Investment Summary

-Acquiring a biotechnology company;

-Proposed spin-off and listing of XNW on Mainland GEM;

-One product was recognized as orphan-drug in US.

Business Overview

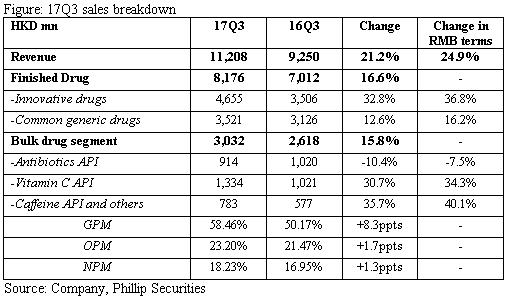

Strong growth expectation. We highlight that the company recorded notable revenue growth in 17Q3 (+24.9% YoY in RMB terms) beyond our expectation. We attribute this to 1) sales hike and rising share of innovative drugs; 2) Caffeine segment reported fast growth and newly-acquired glucose business made more contribution; 3) Vitamin C sales continued to climb. GPM increased by 8.3ppts (17Q3 58.46%, 16Q3 50.17%) due to share of innovative drugs rose which enjoyed higher profit margin. The management expect bottom line to maintain 20%-30% growth in 17E/18E.

Innovative drugs developing quickly. We are positive on bright outlook of innovative drug business. On NBP,both capsules and injection have entered NDRL in 2017 while we still see quite growth potential of NBP injection in future. Oulaining capsule has entered 12 PDRLs while lyophilized powder injection is included in 21 PDRLs. Xuanning, for the treatment of hypertension and angina pectoris, is expected to maintain stable growth as the roll-out of chronic disease management and national tiered medical system. Meanwhile, we highlight that oncology portfolio may serve as a key momentum given Duomeisu and Jinyouli both reported obvious growth in 2017. During first three quarters in 2017, Duomeisu achieved HKD0.36bn sales growing by 44%. It is a drug for treatment of lymphoma, multiple myeloma, ovarian cancer and breast cancer, with less side effects than traditional medicines. Now Duomeisu entered into only three PDRLs. We expect Duomeisu sales to exceed one billion HKD in future with expanding coverage and inclusion into more PDRLs. On Jinyouli, it reported HKD0.26bn (+168% YoY) in 17Q3 and was just selected into new NDRL in 2017. We highlight Jinyouli's potential to achieve high growth in future with further implementation of NDRL.

Acquiring YZY, a biotechnology company. CSPC proactively explores biologic field. Its subsidiary CSPC NBP entered an agreement to acquire 39.56% shares of Wuhan YZY at a consideration of HKD203.57mn. And CSPC will make additional payment up to RMB55mn once milestone events happen. YZY is a biotechnology company engaged in the development of innovative bio-pharmaceutical drugs, including anti-tumor bispecific antibodies. One bispecific antibody in its product pipeline has obtained clinical trial approval, and another bispecific antibody for clinical trial has been submitted in PRC.

Proposed spin-off and listing of XNW on Mainland GEM. XNW is engaged in manufacture and sales of caffeine and vitamin C health supplement and beverage products. CSPC is going to separate XNW (one of indirect subsidiaries) to list on PRC GEM. XNW has already submitted an application to CSRC for proposed A share listing on GEM. After fulfillment of listing, the equity interest of CSPC in XNW will decrease to 75%.

One product was recognized as orphan-drug in US. Orphan-drug is the medicine for treatment of rare disease. In Sep 2017, one product MHL (鹽酸米托蒽醌脂質體) was granted orphan-drug designation by US FDA. This liposome formulation has better efficacy and safety with less side effects. The designation implies that more guidance may be given by US FDA and even part of clinical trials could be waived to speed up product launch. Meanwhile, orphan drugs enjoy exclusive marketing rights for 7 years and tax credits of up to 50% of R&D expenses. The clinical research of MHL is processing in US and we expect the simultaneous application for production approval in China and US by 2020.

Valuation Thesis & Risks

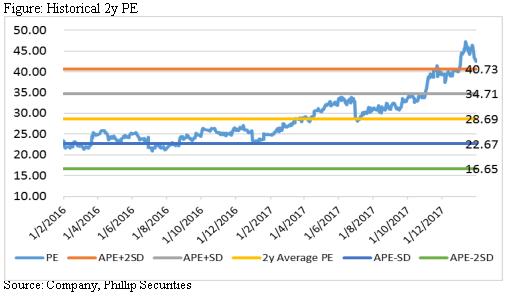

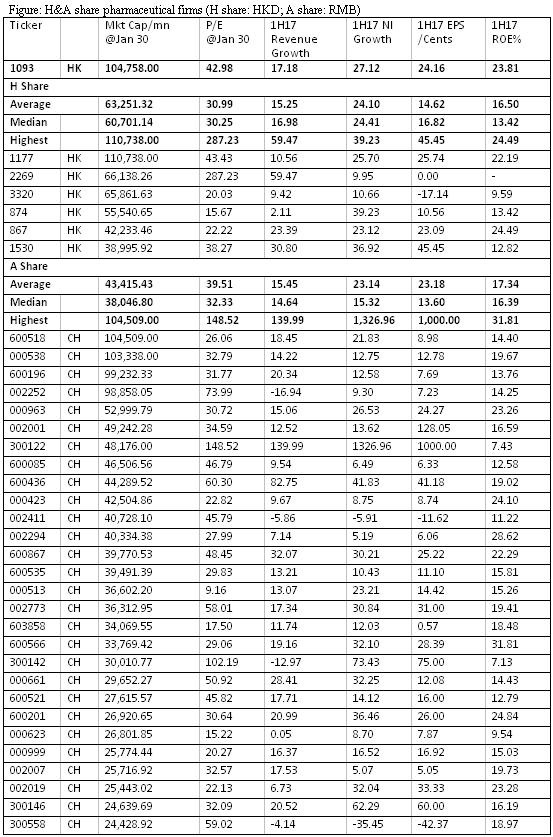

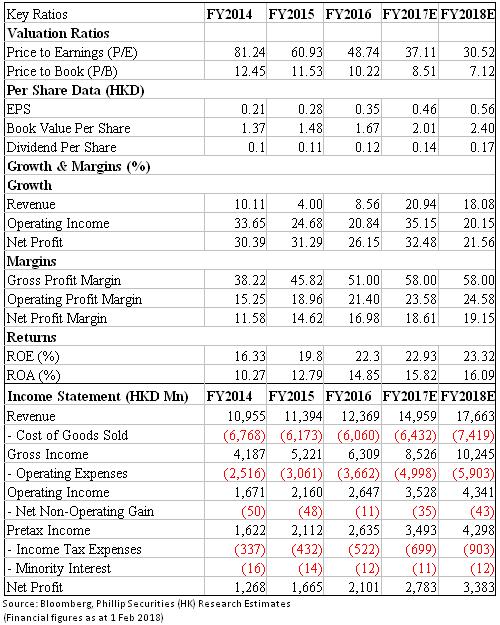

We conservatively predict the topline growth to be 21%/18% in 17E/18E. Assuming relatively stable profit margin, we estimate 17E EPS to be HKD0.46 and 18E HKD0.56. We select 36 pharmaceutical firms listed in HK and Mainland with market cap over HKD30bn, and get industry average PE to be 31x in HK and 39x in Mainland market (excluding outliers). Thus we see average PE range for pharmaceutical firms should be 31x-39x currently. We also highlight that CSPC has higher ROE than HK and Mainland peers (CSPC 23.8%, HK peers 16.5%, Mainland peers 17.34%). We conservatively assume PE 34.7x (par to 2-y historical average PE + 1*SD) and derive 2018E TP 19.4HKD. Risks: 1) Sales growth and R&D fail expectation; 2) Spin-off effect; 3) Policy risks.

Financials

Click Here for PDF format...