Investment Summary

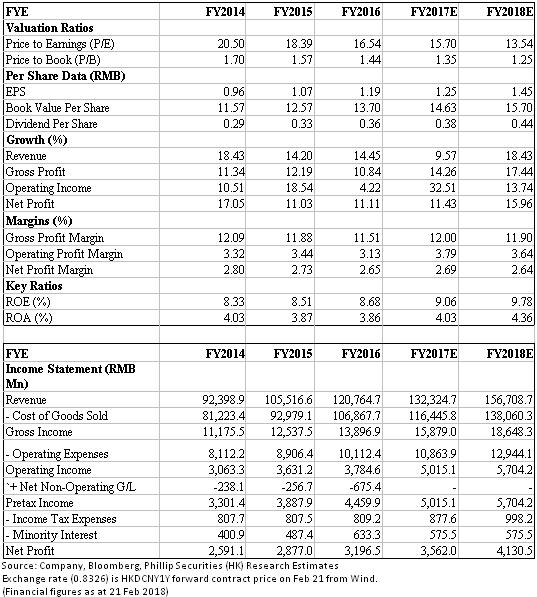

What's new: Finished H share placing and gained HKD3.1bn; Completed the acquisition of Cardinal China and accelerated integration involving DTP business; E-commerce platform is seeking for new investors. Investment recommendation: Considering potential effect of two-invoice system in 1H18 and share dilution, we adjusted numbers to derive 17E/18E EPS RMB1.25/1.45. Conservatively assuming target PE 14.2x (par to 2y historical level), we get target stock price HKD24.8, maintain BUY. (Closing price at 21 Feb 2018)

Business Overview

H share placement generated HKD3.1bn. Shanghai Pharma (SPH) announced the completion of H share placement on Jan 26 and the aggregate net proceeds totaled HKD3.1bn. The proceeds will be used to fund manufacturing and distribution businesses and supplement working capital. 153mn new H shares were sold to not less than six but no more than ten placees at HKD20.43 per share. New shares accounted for 20% of issued H shares or 5.7% of issued shares. After the placement, H shares totally make up 32.34% of total issued shares while A shares portion decreased to 67.66% (before placement H 28.48%, A 71.52%).

Finishing acquiring Cardinal China. SPH announced the completion of acquiring Cardinal China with consideration of USD557mn (c.HKD4.4bn). Core management team of Cardinal China (including President Lin Wenshi) will stay in office and launch 2018 operation plan. Now SPH has finished procedures for closing of transaction and set up a department to promote integration. The acquisition helps to extend SPH distribution network to cover 24 provinces and cities, speeding up its network expansion which aims to cover 28 provinces and cities in 2020E. Also SPH will become one of the largest agents and distributors of imported pharmaceuticals, owning the most categories of imported drug products.

Expected further integration of DTP business. We highlight momentums of DTP business model, including foreseeable outflow of hospital prescriptions, increasing consumption of drugs for cancer and chronic deseases, and residents` stronger consuming power due to intensifying coverage of medical insurance. DTP business is expected to serve as a new driver of distribution enterprises in future, given market value of DTP business will grow at CAGR 39.7%, from RMB10.5bn in 2016 to RMB40bn in 2020E, according to IMS. Comprehensive upstream (drugs) and downstream (hospitals) resources form moat of SPH, which helps to better control cost and absorb prescription outflows. After integration of Cardinal DTP business, SPH will operate over 70 DTP chain pharmacies covering majority of developed regions in PRC.

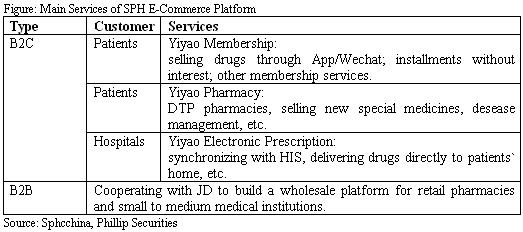

E-commerce platform to attract new investors. SPH invested to set up its e-commerce platform (上藥雲健康) with other investors including JD, IDG, SBCVC, etc. The platform focuses on electronic prescription and develops B2C & B2B businesses. It operates over 32 DTP chain pharmacies under Yiyao Pharmacy brand, covering 13 provinces and 27 cities. We expect the service coverage will continue to expand with further integration of SPH and Cardinal. SPH official website disclosures that the company is proactively searching for new strategic investors and introducing fund to promote further application of the e-commerce platform.

Valuation and Risks

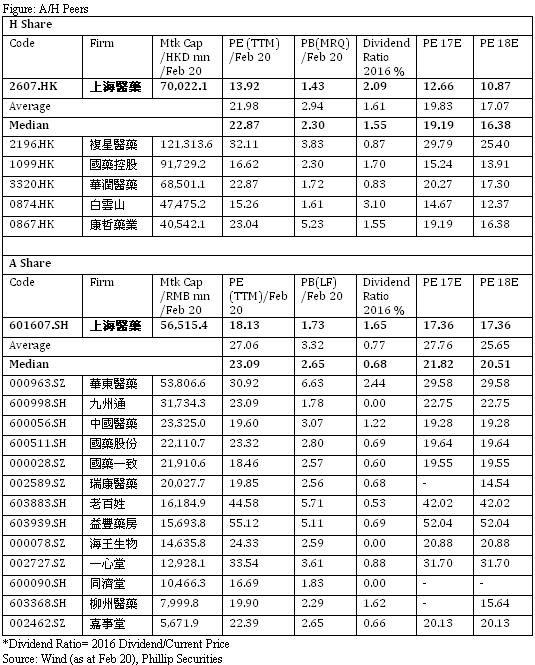

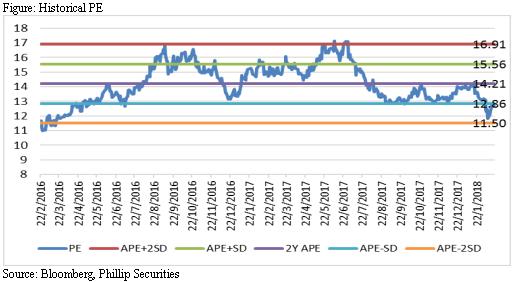

We fine-tuned EPS estimation to factor into potential effect of two-invoice system in 1H18 and share dilution, implying 17E/18E EPS RMB1.25/1.45. We see price still attractive compared to H share peers, given SPH current PE 13.9x (vs. HK peers PE median 22.87x) and 18E PE 10.87x (vs. HK peers 18E PE 16.38x). Meanwhile, with 30% payout ratio, SPH reported higher dividend ratio than peers (SPH 2.09% vs Peers 1.55%). The same is true in A share market. We conservatively assume target PE of 14.2x (roughly par to 2y historical PE) to derive target price HKD24.8 (Exchange rate 0.8326). Risks include: 1) Two-invoice system's effect on inventory allotment business; 2) E-commerce business fail expectation; 3) Policy risk; 4) Dilution effect.

Financials

Click Here for PDF format...