Summary of Investment

- Interim net profit fell by 10% yoy, with short-term pressure on gross margin;

- Strong sales growth in Chinese market, and gradual improvement in European and American markets;

Investment Rating

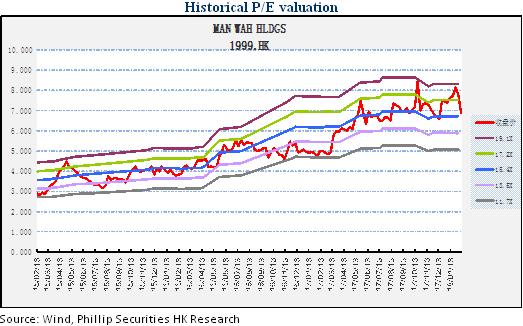

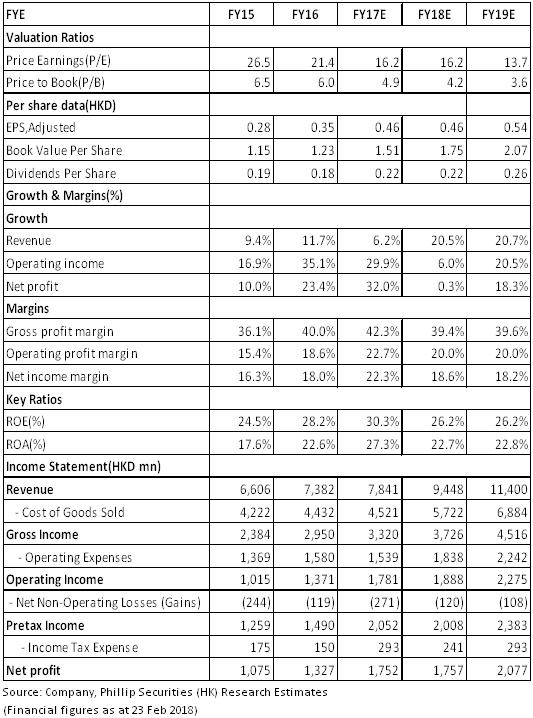

Recently, the Company has acquired two target companies, namely Jiangsu Yulong and Jiangsu Delancey. Upon the completion of the acquisition, the Company will effectively enhance the production capacity and productivity in respect of the business of iron frame and functional sofa in China. We are optimistic about the Company's endogenous growth in the Chinese market. Driven by product price increases, capacity expansion and cost control, the overall gross margin is expected to stabilize and rise. It is estimated that the net profits attributable to the parent company for 2018-2019 will reach HKD1757 million and HKD2077 million, respectively; EPS will be 0.46 and 0.54, respectively, equivalent to PE 16.2 and 13.7, respectively. The rating of "Buy" is given. (Closing price as at 23 Feb 2018)

Interim net profit fell by 10% yoy

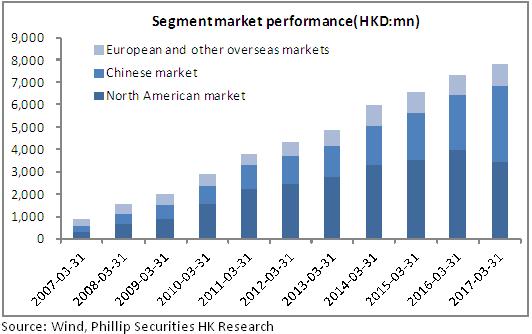

Man Wah Holdings recorded a revenue of HK $4.62 billion in H1 of FY2018, an increase of 28.8% over the same period of last year. Net profit attributable to the listed company was HK $793 million, down by 10.3% yoy. Specifically, the revenue from the sales of sofas and accessory products was HK $3,369 million (+ 13.1%), accounting for 72.8% of the total. The retail business of sofa and related products contributed to revenue of HK $446 million (+ 26.2%), accounting for 9.7% of the total. Revenue of other products recorded RMB420 million (+ 62.1%), accounting for 9.1%. Home Group business recorded a revenue of RMB391 million, accounting for 8.5%.

Gross margin was affected by rising raw material costs

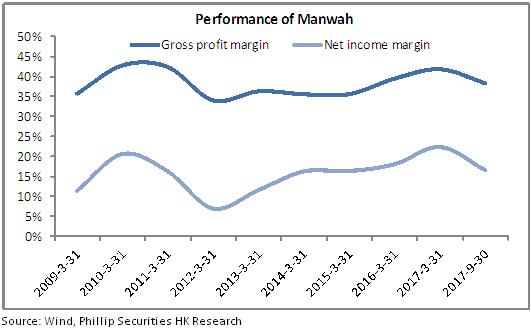

In terms of profitability, the overall gross margin was 38.3%, down by 4.4pct yoy. The decrease in gross margin was partly due to the large increase in the price of raw materials, and, on the other hand, was caused by the merger of the business of the Home Group. The gross margin of the Home Group was approximately 23.6%. Excluding the impact of merger, the gross margin of the Group was approximately 39.7%. In response to the rising cost of raw materials, the Company raised the prices of its products in the market of mainland China by 8%, in which the price of functional sofas rose by about 8% and non-functional sofas and bedding products increased by 5%.

During the period, the expense ratio was 19.83%, up by 1.06pct yoy, of which, the administration expense rate slightly decreased to 4.27% and the selling expense ratio increased by 1.26% to 15.26% yoy. It was mainly due to the merger of Home Group business and rising ocean freight costs. The financial expense ratio rose slightly to 0.2%. In addition, foreign exchange gains and losses during the period dropped from HK $+84 million in the same period of previous year to HK $ -30 million. In summary, the rising cost of raw materials, the rising expense ratio and the exchange losses eventually dragged down the net profit growth.

Strong sales growth in Chinese market

During the period, the wholesale business achieved a substantial growth in Chinese market with an increase of 40.2% yoy to HK $1,285 million with a gross margin basically unchanged. The number of outlets increased from 1,504 in March 2017 to 1,630 with an increase of 8.4%. The average sales volume increased by 16.1% yoy, and the operating efficiency improved significantly. The future growth in the Chinese market, on one hand, comes from the Company's continuous efforts to expand online and offline distribution channels. In the future, the offline outlets will have a broad space for expansion, while online e-commerce platforms still boast good growth potential; on the other hand, the current functional sofa witnessed a period of rapid development, and the Company is expected to further enhance market share through its brands and channels.

Exports in European and American markets gradually improved

Revenue in North America market grew by 2.1% yoy to RMB1,756 million, with gross margin dropping 5.3pct, while revenue in Europe and other markets dropped by 2.6% to RMB329 million, with gross margin decreasing 4.9pct. In the North American market, the Company achieved a monthly improvement in sales growth by enriching product lines, strengthening sales team building and expanding new customers. In addition, the Company has embarked on an expansion project to boost production capacity in the European market, and put wood processing plants into operation recently, which are expected to significantly reduce the cost of raw materials. In our opinion, the collaborative advantages brought by the acquisition of Home Group will help the Company continue to explore the European market and the Chinese market.

Risk Warnings

Market competition is intensified;

Gross margin goes downward;

Sales growth is less than expected;

Financials

Click Here for PDF format...