Investment Summary

- Exchange Loss Causes the Results of 2017Q3 to Decrease by 1.5%

- Core Profit Increase is Great, and Q3's Net Profit Actually Rises by 20%

- Enhancing the Market Share and Better Sales Structure

- Overseas Business is Entering the Right Path, Global Expansion is being Continually Advanced

Investment Thesis

Stable position in the industry, the continuous optimization of product mix, and high dividend rate provide a greater margin of safety for the Company's share price. The sound development of overseas business will bring high resilience of earnings, which is promising.

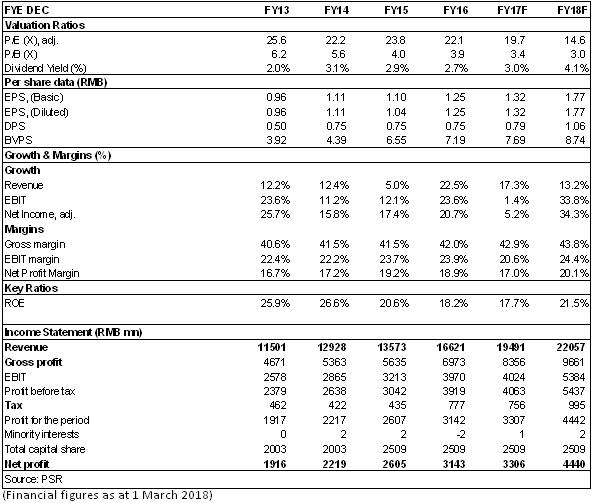

We maintain the "Accumulate" rating,with target price to be HK$ 34, equivalent to 16x P/E for 2018. (Closing price as at 1 March 2018)

Exchange Loss Causes the Results of the First Three Quarters of 2017 to Decrease by 1.5%

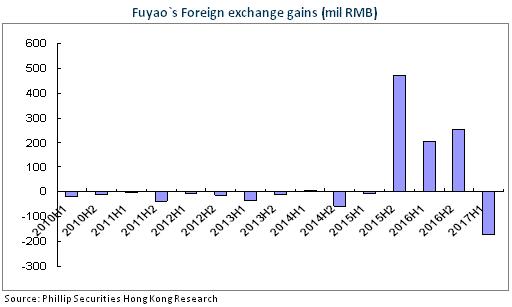

The revenue of Fuyao Glass in the first three quarters of 2017 increased by 15.6% yoy to RMB13.4 billion; the net profit attributable to the parent company was RMB2.14 billion, slightly down by 1.5% yoy; the basic EPS was RMB0.85, from RMB0.87 of the same period of the previous year. Mainly as a result of the exchange losses due to the appreciation of RMB, the exchange loss in the first three quarters was RMB0.3 billion (RMB0.13 billion in the third quarter), while the exchange profit in the same period of the previous year was RMB0.21 billion.

Core Profit Increase is Great, and Q3's Net Profit Actually Rises by 20%

If the impact of exchange was excluded, the net profit in the first three quarters would increase by 17.8% yoy, and the main business would tend to continually greatly increase. On a closer look at quarters, EPS in the first three quarters reached RMB0.28, RMB0.27 and RMB0.30, respectively from last year's RMB0.23, RMB0.35 and RMB0.29, respectively. Under the disadvantageous condition of dramatic RMB appreciation in Q3, the Company's single-quarter result still kept growing slightly. If the impact of exchange was excluded, the actual profit of Q3 increased greatly by more than 20% yoy.

Enhancing the Market Share and Showing a Steady Improvement in Sales Structure

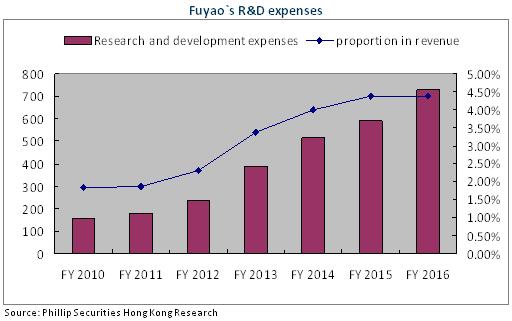

The Company's sales volume increases at a speed higher than that of the automobile industry in the downstream (China+5%, America -1.9%), indicating that the market share of products of the Company is growing. In recent years, the Company has been expanding the production scale by upgrading the production line, and enhancing the raw material utilization rate by enriching product categories of high added value and featuring a strong cost control ability. Fuyao Glass's gross margin basically remains stable and its overall gross margin is 42.8%, despite that the price of raw material, i.e., soda ash had been on the increase in the first three quarters. Specifically, the gross margin of Q3 increased 0.6 ppts to 42.5% qoq. We think that this is mainly associated with the proportional growth of the products of high added value of the Company and the gradual improvement of the profitability of the American factory.

Overseas Business is Entering the Right Path, Global Expansion is being Continually Advanced

Fuyao Glass's automobile glass factory in Ohio, America has started to make profit: It reported a profit of USD2,195 thousand from June to September, and it is predicted that only a slight loss was accumulatively generated in 2017, and a profit will be contributed in 2018. The profit of the float glass factory, Mt.Zion, America in the first three quarters was USD7.50 million, and it is predicted that the year's profit will be more than USD10 million. The Company's overseas layout will finally be paid back.

The net cash flow from operating activities of the first three quarters increased by 14.55% to RMB3.1 billion yoy. Specifically, that of Q3 was RMB1.4 billion, an increase of 13% yoy and a surge of 110% qoq. This indirectly indicates that the Company's overseas business has started to be paid back positively, and the American factory's profitability is rapidly restoring.

Fuyao Glass's market shares in the domestic supporting automobile glass market and the global automobile glass market are 65% and 20%, respectively. There is huge room for improvement in the overseas market. After the completion and commissioning of Phase I (3 million sets) of the factory in Ohio, America at the end of 2016, the supplementary Phase II of 2.5 million sets has also been completely installed and is predicted to be gradually put into production in February. The American factory's total productivity is expected to reach 5.5 million sets. At the same time, the Company's global productivity expansion is still being progressed; it plans to invest in an automobile glass project of 4 million sets in Suzhou City, Jiangsu Province; float glass factories in Benxi City, Liaoning Province, Germany and Russia are also in the planning. We predict that Fuyao Glass's leading position will be further consolidated, as its domestic and overseas industrial layout is being constantly improved.

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

Financials

Click Here for PDF format...