Investment Summary

We highlight that 1) 2017 results remain robust; inventory level comes back to be normal; non-Anta brands kept high growth; expenses may continue to rise; product innovation may be key driver for future development. We estimate the expenses to go up in future and revise target price to HKD43.68 based on target PE 26x. (Closing price as at 13 Mar 2018)

Business Overview

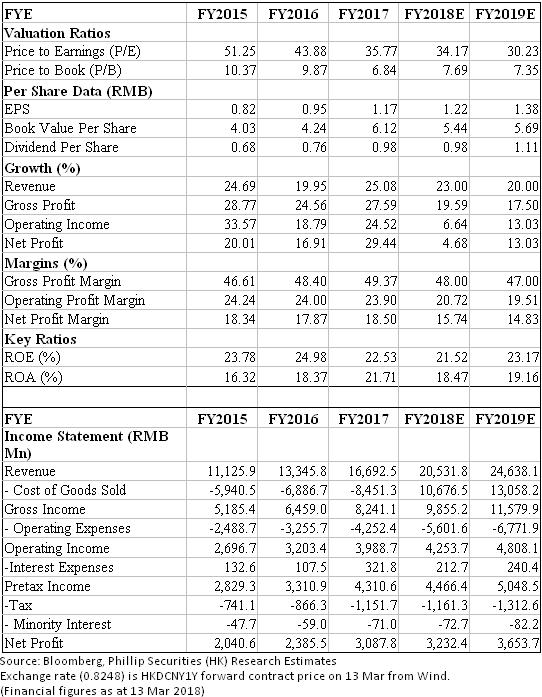

2017 results kept strong. Anta reported 2017 revenue of RMB16.69bn implying YoY growth of 25%, higher than our previous expectation by 4.23%. Gross profit recorded RMB8.24bn growing by 27.59% YoY. Gross profit margin increased by 1% than 2016 GPM. We see that 2H17 GPM is higher than first half (1H17: 50.57%; 2H17: 48.4%), attributable to raw material price hike in second half. The management expects that in future gross profit margin will be stable.

Rising expenses. We see OPM decreasing by 0.1% YoY and expenses rising, which is mainly due to the increase in selling and distribution expenses and administrative expenses as a result of the expansion of retail operations. Administrative fees increased by 31.6% to RMB901mn and its percentage in revenue increased from 5.13% to 5.4%. Staff costs ratio rose by 0.6%, due to increasing R&D expenses in order to enhance innovation power. The management is confident to keep future expenditure around acceptable level. We highlight that expenses may be in rising trajectory given intensifying investment in R&D. Considering good track record, we expect the company to achieve stable profit margin.

Inventory. We see inventory turnover days increased dramatically (75 days in 2017, 61 days in 2016). The management attributed this to festival effect and emphasized that the majority of inventory has been delivered till now.

Brands. Anta brand kept growth, especially Anta Kids which grew dramatically by 40% YoY in 2017. Non-Anta brands developed quickly and FILA contributed over 80% to 17Q4 growth. As at end of 2017, the number of Anta stores reached 9467, while FILA has 1086 stores and Descente 58 stores.

R&D accelerating brand image upgrading. The company will make efforts to enhance brand image and strengthen innovation power. We highlight the importance to increase product quality and brand reputation under the consumption upgrade trend, given stronger consumption demand and power. If the strategy succeeded, we expect ASP to further increase and enlarge the topline.

Valuation

We maintain our target PE 26x and highlight the expense expectation to derive 18E/19E EPS of RMB1.22/1.38, thus we get 2019 target price to be HKD43.68. Risks include: Rising expenses; fierce competition in retail industry; operational inefficiency due to multiple brands. (Exchange rate=0.8248RMB/HKD)

Financials

Click Here for PDF format...