Investment Summary

The annual throughput exceeds 65 million passengers

The net profit in the first three quarters increased steadily

After putting into operation, T2 Terminal keeps releasing its capacity and reflects its commercial values

Baiyun Airport accelerates its building of an international hub

Investment Thesis

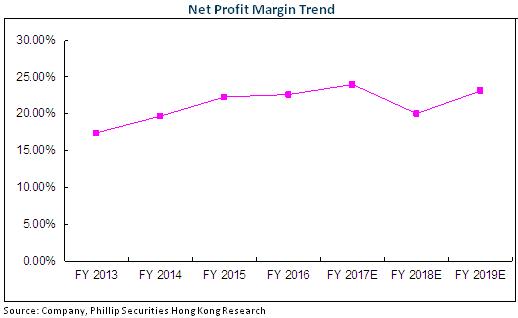

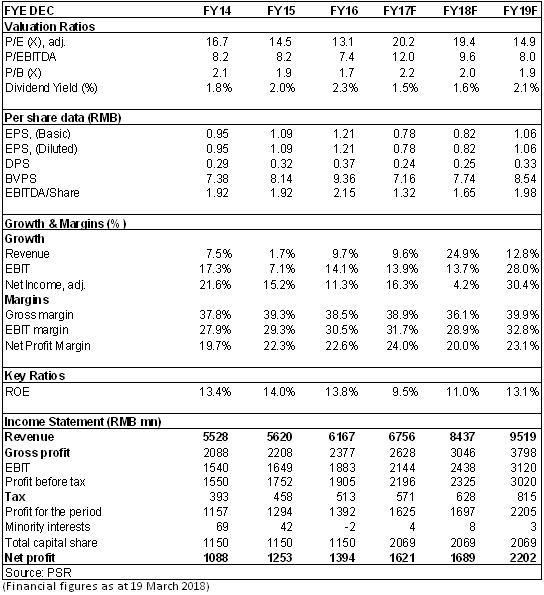

Given that the company expanded its capital after dividend distribution and share donation, and that the convertible bond redemption had an influence on the dilution of EPS, we forecast its EBITDA/share in 2017/2018 to be RMB 1.32 and 1.65 yuan, our target price of RMB 18.7 yuan, respectively 11.3/9.4x of our expected EBITDA/Share. We give it an "Accumulating" rating. (Closing price as at 19 March 2018)

The annual throughput exceeds 65 million passengers

Baiyun Airport is the third largest airline hub in China, with one terminal and three runways. Its source of passengers is mainly the Pearl River Delta region. In 2017, the company had throughput of 65.78 million passengers, an increase of 10.2% compared with that of the previous year, ranking No. 13 globally. As of the end of 2017, Baiyun Airport's route network has covered more than 210 navigation points around the world, among which nearly 90 international and regional destinations are accessible to over 40 countries and regions; more than 75 airlines operate at Baiyun Airport.

The net profit in the first three quarters increased steadily

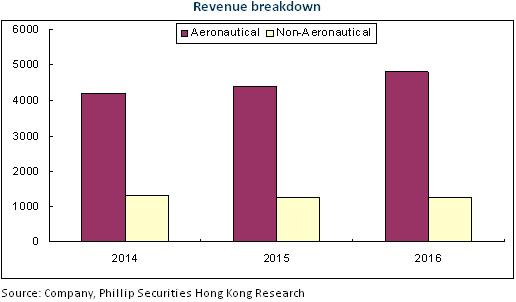

Benefiting from the increased number of peak hours, the volume of business of Baiyun Airport increased steadily in the first three quarters, with 346,000 aircraft movements, 48.64 million throughputs of passengers, 1.29 million tons throughput of cargo and mails, an increase of 7%, 10% and 8%, respectively. Its growth of production data is in the leading position among the three largest airports in China. As CSA, a main base airline, has built the Canton Route and arranged its international flight courses actively in recent years, Baiyun Airport has continuously increased the percentage of its international flight courses, and constantly refined its flight course structure.

In the first three quarters in 2017, the company reported a revenue of RMB4.92 billion, a YoY increase of 8.5%; net profit attributable to parent company stood at RMB1.18 billion, a YoY increase of 11.33%, equivalent to an EPS of RMB0.57. More than one year after the new management performed their responsibilities, the company has kept improving its operating efficiency, decreased the sales expenses and administration expenses by 16% and 13% yoy, respectively, and reduced the administration expense ratio by 1.3 ppts to 5.8% yoy.

After putting into operation, T2 Terminal keeps releasing its capacity and reflects its commercial values

The expansion project of Baiyun Airport started in August 2012. This project covers many supporting facilities, including the third runway and its taxing system, T2 Terminal, station site and air traffic control, and oil supply, etc. Among other things, the third runway has been put into operation since February 2015. T2 Terminal will be constructed and put into use in 2018. At that time, Baiyun Airport will be able to meet the needs of 620,000 aircraft movements, 80 million throughput of passengers, and 2.5 million tons thorough of cargo and mails per year, and further break through the bottleneck of capacity.

On the other hand, the commercial parts of T2 Terminal and the transportation center in Phase I cover an area of 44,000 square meters, among which 36,000 square meters are offered to attract investment. At present, the invitations for bids of the duty-free entry and exit, commercial retail and advertising have been successively completed. It is expected that not less than RMB1.3 billion income will be obtained in 2018, which is completely able to cover the depreciation expenditure (RMB414 million) after T2 is put into operation, and will hopefully contribute to a net profit of approximately RMB0.6 billion.

Baiyun Airport accelerates its building of an international hub

Facing the Oceania, Southeast Asia and Africa, Baiyun Airport is equipped with obvious regional advantages. In the development and reform planning of the civil aviation industry released by the State Council and the Civil Aviation Administration of China, Baiyun Airport is defined as one of the three largest airport hubs in China. The requirement of building Baiyun Airport into an international airport hub is emphasized in the planning and documents of the Guangzhou Airport Economic Zone Management Committee, Guangzhou Municipality and Guangdong Province. In the first three quarters, the percentage of international passengers of Baiyun Airport has arrived at 24%, and the percentage of transfer passengers of Baiyun Airport has stood at nearly 13%. From a medium- and long-term perspective, Baiyun Airport plans to accelerate the three phases of the expansion projects of the fourth and fifth runways, the fourth eastern and western airside concourses, T3 Terminal, and APM system building, and accelerate the construction of freight facilities. The expansion projects will further meet the increasing demands of air transportation in the Pearl River Delta and south China, and accelerate the building of Baiyun Airport into an international airport hub.

Financials

Click Here for PDF format...