Summary of Investment

- Steady operations and stable improvement in operational efficiency;

- Sound cash flow and attractive valuation;

Investment Rating

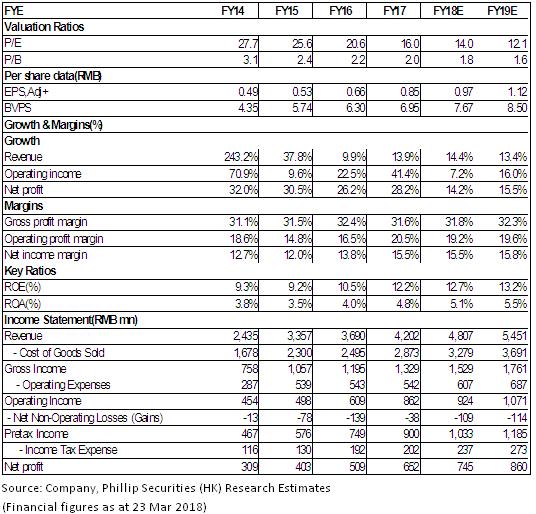

We are optimistic about the sound growth potential in the Company's future performance. It is forecast that net profits of the Company in 2018 and 2019 will reach RMB745 million and RMB860 million, respectively, earnings per share (EPS) will be RMB0.97 and RMB1.12, respectively, the current valuation level is attractive, and the target price will be RMB18.0, with a “Buy” rating. (Closing price as at 23 Mar 2018)

Steady Growth throughout the Year, in Line with Expectations

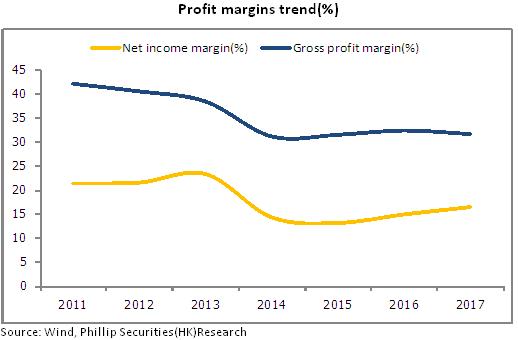

In 2017, Grandblue Environment recorded a revenue of RMB4.202 billion, up by 13.87% y-o-y, net profit attributable to the parent company was RMB652 million, up by 28.25% y-o-y, and net profit attributable to the parent company excluding non-recurring items was RMB594 million, up by 20.64% y-o-y. EPS excluding non-recurring items was RMB0.78. The figure was RMB0.66 over the same period of last year. Performance was in line with expectations and growth was stable on the whole.

With respect to profitability, gross margin fell by 0.76pct to 31.63% and net profit margin rose by 1.52pct to 16.59%, the latter of which was mainly due to the increase of non-recurring profit and loss arising from the increase of government grants. The period cost rate fell by 1.8%, of which sales expense decreased by 0.27pct to 1.66%, administration expenses decreased by 0.19pct to 6.99%, and financial expense decreased by 1.34pct to 4.26%.

Cash flow recovery was of relatively good condition, and net operating cash flow rose by 28% y-o-y to RMB1.509 billion. Book capital increased to RMB1.294 billion and the asset-liability ratio was 56.79%, down by 1.47pct y-o-y, and the financial leverage was on an obvious decline in the last three years. The Company forecasts an annual capital expenditure of RMB2.7 billion in 2018, and the sound financial structure shall support its business expansion.

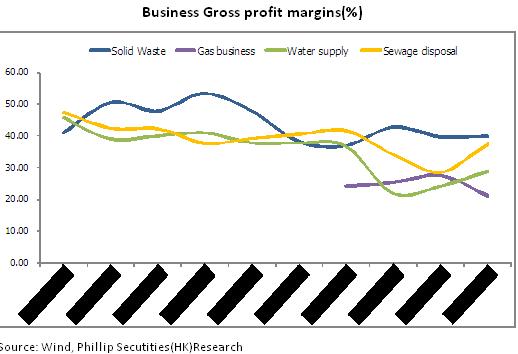

Substantial Increase of Gross Margin in Water Business

With respect to revenue structure, water supply business contributed RMB1.108 billion to revenues, up by 4.33% y-o-y; revenue of sewage treatment was RMB188 million, up by 17.85% y-o-y; revenue of solid waste treatment was RMB1.428 billion, up by 7.01% y-o-y. Water supply and sewage treatment business saw a significant rise in gross margin, mainly due to cost reduction in electricity fee and repair charge and the decrease of water loss rate, rising by 4.8% and 8.8% to 28.85% and 37.27%, respectively. Gross margin of the solid waste treatment business basically remained unchanged, slightly up by 0.19pct y-o-y to 40.05%.

The gas service reaped a revenue of RMB1.479 billion, up by 21.57% y-o-y. The main reason behind the relatively rapid growth was that the shift to natural gas as required by environmental policies drove the increase of sales volume by 27.8% y-o-y and the sales volume of liquefied gas rose by 22.89% y-o-y, whereas gross margin fell by 6.57pct y-o-y to 21.05%. This was mainly due to the y-o-y decrease in price difference between purchase and sale of natural gas and liquefied gas, and cost offset by tax rebate, etc. In December 2017, the Company acquired the remaining 30% equities in Nanhai Gas with RMB437 million. In 2017, Nanhai Gas reported a revenue of RMB1.479 billion and net profit of RMB138 million, and the consolidation in 2018 shall improve profitability and overall performance.

Steady Progress of Projects and Operational Efficiency Improvement Assisted by Renovation & Expansion

The Company is proactively committed to the upgrading & reconstruction and renovation & expansion of all projects in a bid to improve operational efficiency. At present, the water supply production capacity is 1.36 million tons/day, sewage treatment is 583,000 tons/day, of which the Second Water Plant Phase IV expansion project (250,000 tons/day) and the sewage treatment plant upgrading & reconstruction project (20,000 tons/day) are expected to be put into operation in mid-2018. In addition, efforts are made to accelerate ongoing projects such as Foshan City Solid Waste Treatment Industrial Park Phase III project (1,500 tons/day), C&G Jinjiang upgrading & reconstruction project (500 tons/day), C&G Anxi renovation & expansion project (750 tons/day), C&G Langfang renovation & expansion project (500 tons/day), and the supporting gas project for the gas company's “Shelv” Phase II, which is expected to secure steady growth in future earnings.

The Company has made new achievements in business expansion. First, it firmly implements the strategy of “mega solid waste”. The Company has obtained the environmental impact assessment (EIA) approval for the Foshan green industrial waste project in collaboration with REMONDIS of Germany, which is expected to dispose 93,000 tons of hazardous waste each year. Second, it becomes the controlling shareholder of Tuowang Bio. The Company has obtained four BOT or PPP projects for harmless treatment of dead livestock and concession operation of cyclic resource utilization. Third, it increases capital in Blue Bay Company and invests in the watershed management project of the Lishui River, so as to march towards the watershed management sector. In general, the expansion of new business shall create new growth for future performance.

Risk Warnings

Risk may arise from environmental policies;

Project expansion falling short of expectations;

Drop of gas price and intensifying market competition.

Financials

Click Here for PDF format...