Investment Thesis

Minth's 2017 result slightly lower than our previous forecast, but the increasing trend of the topline is still to continued. We maintain the opinion that Minth's existing businesses indicate a robust growth momentum, while great potential boom lies before the new ones, on the base of more input on R&D etc. We gave target price of HK$ 45.55 and Buy rating. (Closing price as at 27 March 2018)

Result slightly lower than expected

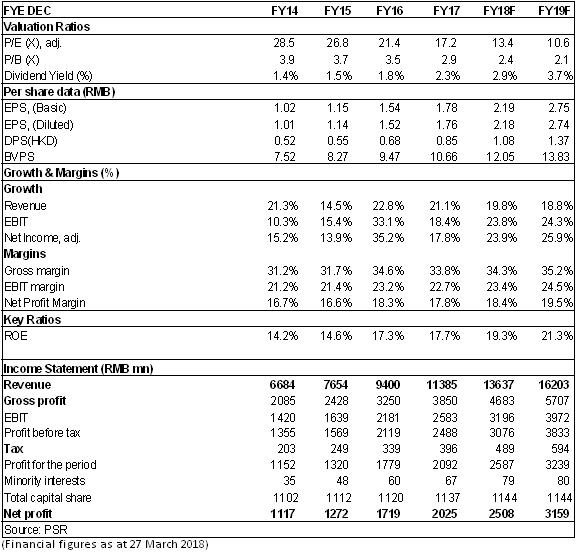

For the year 2017, Minth Group's turnover reached RMB11.384 billion, with an increase of 21.1% year-on-year; the gross profit was RMB3.849 billion, with an increase of 18.4% year-on-year; net profit attributable to owners of the company was RMB2.025 billion, meaning year-on-year growth of 17.8%. Earnings were lower than market expectations, slightly lower than our previous forecast of RMB2.13 billion. Basic earnings per share were RMB1.782. The proposed final dividend was HKD0.85 per share.

Driven by European customers, overseas growth is slightly higher than domestic growth

In terms of specific markets, domestic sales amounted to approximately RMB7.102 billion, with an increase of approximately 20.1% from 2016, mainly due to the increase in production and sales volume of Japanese, German and American cars in the Chinese market. Overseas turnover amounted to approximately RMB4.382 billion, with an increase of approximately 22.7% from 2016, mainly due to business growth in overseas markets, especially in Europe, benefiting from orders from BMW, Audi, Daimler and other customers. The European market share has increased rapidly from 8.8% to 12.7% in previous years.

Rising cost of raw materials and some other factors show an impact on the gross profit

The gross margin reached 33.8%, which was about 0.8 ppts lower than that of 34.6% in 2016. This was mainly due to the depreciation of old products and the increase of raw material costs. At the same time, some overseas factories were still at the climbing stage, and the gross margin remained to be improved. To this end, the company strives to maintain stable overall gross margins by implementing lean production, optimizing production layout, and adjusting product structure.

Labor cost investment and capital expenditure increased

During the period, the company's sales expense ratio and administration expense ratio increased slightly by 0.2 ppts and 0.5 ppts, reaching 4.2% and 7.5%, respectively. The administration expenses increased by a big margin, namely 29% over the same period of last year, mainly due to the company raising employee salaries in order to maintain competitiveness and sustainable development, causing labor costs to rise. Capital expenditure of the period increased by 76%, amounting to RMB2.1 billion, which was mainly used for the construction of factories in Jiaxing, Huai`an, and Mexico, and increased investment in automated production lines, flexible production lines, intelligent logistics, and information management systems.

Share of high-end brands increased, and product layout continues to expand

In terms of customer development, Minth has expanded its market share for high-end brands and entered the Mercedes-Maybach business system for the first time. Meanwhile, in addition to Great Wall, it has also attracted customers such as GAC, Geely, and Changan.

In regard to product development, the company has made achievements in the 3 development dimensions of intellectualization, weight reduction and electrification. In intellectualization, the company achieved the R&D and promotion of ACC equipped new products; in weight reduction, while continuing to expand the aluminum product business, it has expanded the layout of traditional products on new energy vehicles and obtained the new business of aluminum battery pack for Nissan and Renault's related electric vehicle models, as well as the new business of opening and closing of grilles for electric vehicles. At the same time, relying on the platform of Min`An Auto, the company is seeking and developing strategic products for the core components of electric vehicles.

Ambitious goal

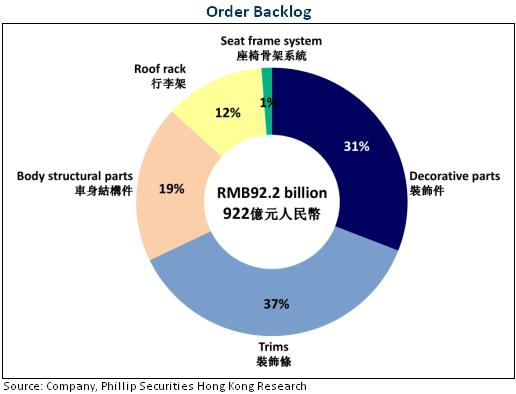

At present, the company's total orders in hand amount to RMB9.22 billion , which means a growth of 16% compared to the end of 2016, and 8.1 times the total revenue in 2017, indicating a foreseeable good result for the future. The company set a total revenue target of RMB50 billion for 2025 (CAGR=20%), showing the management's confidence in the future global competitiveness strategy to maintain the company's sustainable development through upgrading product technology, improving global production layout and enhancing global business operation capability.

Valuation

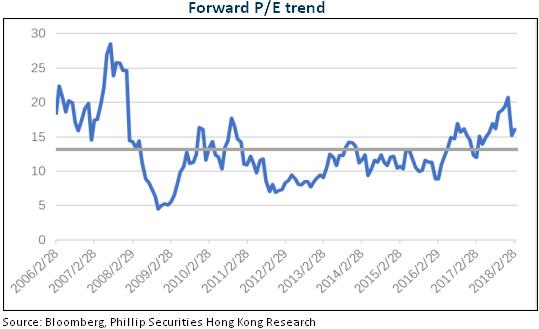

The Company has a solid financial condition, with only 31% asset- liability ratio and 3.8 billion cash in hand. Besides, its operating net cash flow has increased year by year and achieved 1.88billion for 2017. It is believed that the 40% dividend payout ratio will maintain. We believe that it is reasonable to give the company a valuation of 16.6x/13x P/E in 2018/2019, equivalent to target price of HK$ 45.55 and Buy rating.

Financials

Click Here for PDF format...