|

|

|

*Advertisement* |

|

|

|

|

|

4 Apr, 2018 (Wednesday) |

|

|

CEB GREENTECH(1257)

Analysis:

Based on the business layout, the company founded three management centers, including clean energy, solid waste and environmental restoration. While consolidating existing main business, the company actively enhances natural gas, soil, soil remediation to brew a new growth point. Based on the fundamentals of good quality and the boom of the biomass and hazardous waste industry, we expect the net profits attributable to the parent company in 2018-2019 will reach HKD1345 / 1680 million, and the EPS will be HKD0.65/0.81, equivalent to the PE of HKD12.0 / 9.6, respectively. The target price of HKD 9.36 and an Buy rating is given.

Strategy:

Buy-in Price: $7.83, Target Price: $9.36, Cut Loss Price: $7.20

|

| |

|

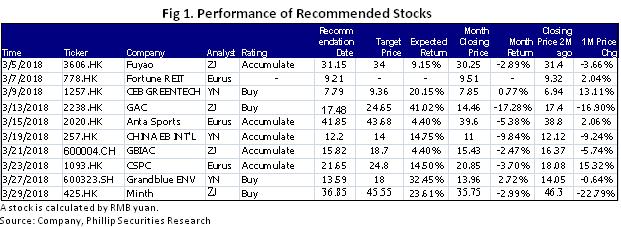

Report Review of March 2018

Sectors: Air & Automobiles (ZhangJing) Environmental protection & New energy(Wangyannan) Healthcare & Consumer (Eurus Zhou) Automobile & Air (ZhangJing)Minth's 2017 result slightly lower than our previous forecast, but the increasing trend of the topline is still to continued. We maintain the opinion that Minth's existing businesses indicate a robust growth momentum, while great potential boom lies before the new ones, on the base of more input on R&D etc. We lift target price and rating. GAC's 2017 Result is in line with our expectation. With a good beginning and a brilliance new car plan in 2018, we believe that the excellent growth will last for GAC in this year, and so we reaffirm target price and rating. Environmental protection (Wang Yannan)This month I released 3 equity reports, including CEB GREENTECH(1257.HK) , CHINA EB INT`L (257.HK)and Grandblue ENV (600323.SH). We tend to highly recommend CEB GREENTECH (1257.HK). Based on the business layout, the company founded three management centers, including clean energy, solid waste and environmental restoration. While consolidating existing main business, the company actively enhances natural gas, soil, soil remediation to brew a new growth point. Based on the fundamentals of good quality and the boom of the biomass and hazardous waste industry, we expect the net profits attributable to the parent company in 2018-2019 will reach HKD1345 / 1680 million, and the EPS will be HKD0.65/0.81, equivalent to the PE of HKD12.0 / 9.6, respectively. The target price of HKD 9.36 and an Buy rating is given. Healthcare & Consumer (Eurus Zhou)This month I released 3 equity reports, including Fortune REIT (778.HK), Anta Sports (2020.HK) and CSPC (1093.HK). We tend to highly recommend CSPC (1093.HK) and Anta Sports (2020.HK). On CSPC, we highlight that 1) 2017 results maintain strong growth; 2) NBP and oncology portfolio grew rapidly; 3) gross profit margin climbing while operating expenses surging (R&D, selling). CSPC has become the leading pharmaceutical firm among HK listed peers, given its great growth potential with high visibility. Moreover, we recommend Anta Sports given its strong growth potential of non-Anta brands and expected external expansion. The management expects that in future gross profit margin will be stable and expenses will be controllable. Though inventory days at year end was much higher than 2016 level, the management emphasized it has returned to be normal now. We expect rising R&D expenses to accelerate brand image upgrading thus boost further development of Anta Sports.

Click Here for PDF format...

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|