Investment Summary

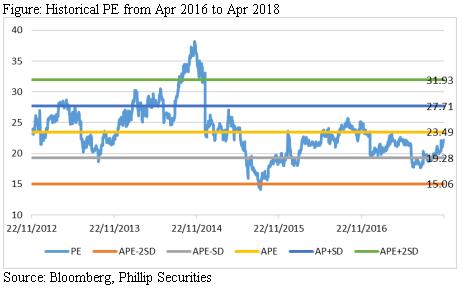

CMS reported strong 2017 results with decreasing expense ratios. Going forward, we highlight that current core products will grow stably in addition that expected progresses in pipeline may become possible explosive catalyst for stock price. We fine turn financial data to derive 18E/19E EPS of RMB0.77/0.86, and with target PE 23.45x (par to 2-year historical average plus 1x SD) we increase TP to HKD21.97, BUY recommendation. (Closing price as at 4 Apr 2018)

Robust 2017 Results

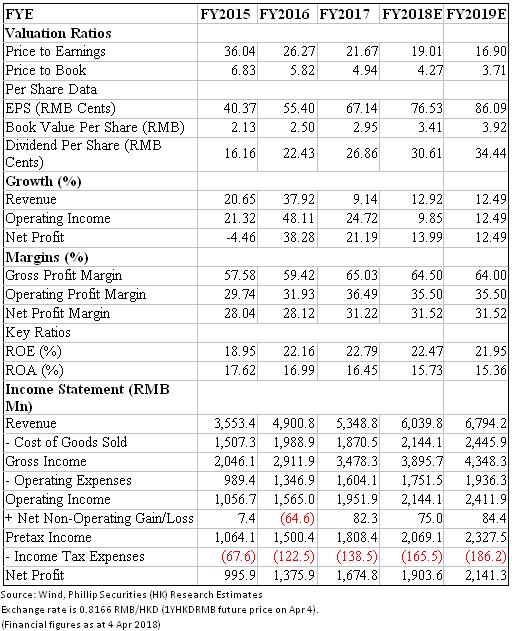

The company reported revenue of RMB5348.8mn (+9.1% YoY), mainly attributable to sales hike in 2017 (excluding Two-invoice System effect, topline RMB5578.6mn, +21.2% YoY). GPM rose from 59.4% to 65%, however, excluding TIS effect there is 1% decrease in GPM, given ASP down by 1.9pp. We see efficient cost control measures, given EBITDA margin increased by 0.7pp, with percentage of selling/administrative expenses in revenue dropping by 0.8pp, as well as stable NPM. We see climbing inventory days and A/R days, mainly due to TIS effect (lower COGS) according to the management, which drew down turnover and added turnover days. Meanwhile, ROE rose by 0.9pp to 24.6% with stable payout ratio 40%.

Products Updates

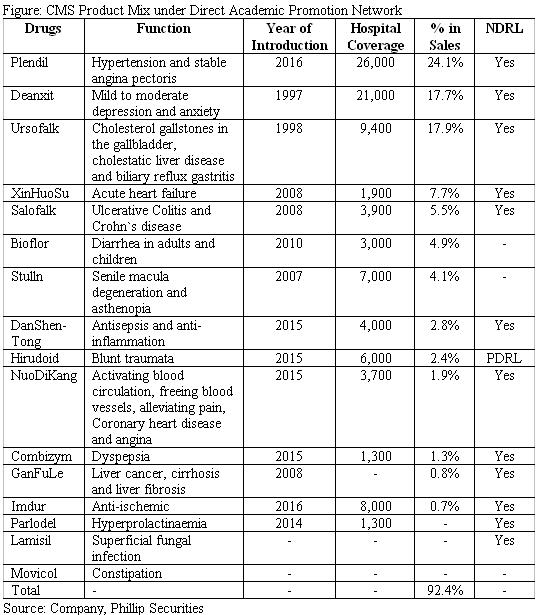

Plendil, included in NDRL, is for the treatment of hypertension and stable angina pectoris. On comparable basis, Plendil sales recorded ~8% YoY growth covering 26,000 hospitals and medical institutions (2016: 20,000). Since CMS took over Plendil asset, the company changed the down revenue trend when it belonged to AstraZeneca. Given much bigger market size of current comparable drugs, we highlight the great potential of Plendil to grow in future.

Xinhuosu, Class I biological agent used to treat acute heart failure, is the only rhBNP currently in China market. It entered NDRL through negotiation in Jul 2017, thus its ASP dropped by 40% while sales volume surged. Management indicated that Xinhuosu was estimated to grow by 36% YoY excluding the price cut effect. Resulting from price cut with TIS effect, the product reported negative growth in 2017 (-23.4% YoY). We highlight there will be a tradeoff between price cut and sales volume hike. We expect notable and positive growth in 2018E.

Deanxit, introduced in 1997 and ranked NO.1 in market share of antidepressant drugs in China, reported sluggish sales growth (+3.4%) in 2017. Given the company will strengthen promotion and management, we expect high-digital to low-teen growth for Deanxit in 2018E.

TCM products (Danshentong, Nuodikang, Ganfule) grew slowly or negatively in 2017. The management attributed this to policies and lack of medial evidences for promotion. After adjustments for compliance requirements, CMS is going to boost TCM products sales through further localizing its distribution network.

Others. Main products (including Ursofalk, Salofalk, Bioflor, Stulln, etc.) reported notable YoY growth higher than 20%. New products introduced during recent years, also grew dramatically, though insignificant sales volume currently. We expect them to contribute more to revenue in future.

Pipeline Progresses

There are three main series in pipeline. 1) CMS024: it is for treatment of liver cancer, national Class I new drug. Currently, the research company is conducting phase III extended clinical-trial and it is in the patient recruitment stage. The listed firm will pay loyalty fee (13% of sales) to the research firm without bearing R&D risks. 2) Traumakine: for ARDS with huge market potential, developed by Faron, a Finland firm. The listed firm owns its rights in China. The patient data for phase I/II will be unblinded in Apr 2018. If the result is positive, we expect it to be commercialized in two years. 3) Destiny Pharma portfolio: Product XF-73, a kind of nasal gel with numerous potential target patients, has accomplished phase I/IIa clinical-trial in Europe and US; other two products (XF-70 & DFD-207) are in pre-clinical stage and to be developed to treat skin infections and ocular microbial infections.

Investment Thesis, Valuation & Risk

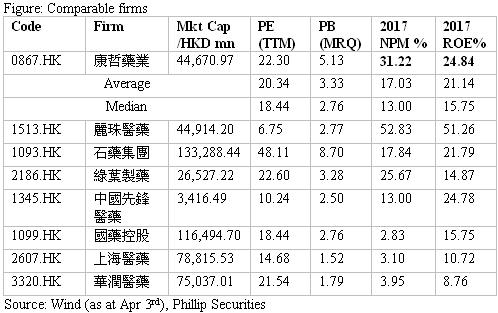

Our valuation model gives target price of HK$21.97. We highlight future growth momentum coming from increasing penetration of current hospital coverage and possible explosive contributor from pipeline. Comparing with HK listed peers, the company enjoys advanced ROE and NPM, thus we appreciate its stock valuation. Excluding possible pipeline contribution, we assume efficient expenses control and predict 18E/19E EPS to be RMB0.77/0.86, based on current product mix potential. Given target PE 23.45x (par to 2-y historical average plus 1* SD), we given target price of HKD21.97, BUY recommendation. (Exchange rate= 0.8166 RMB/HKD)

Risks include: R&D fail expectations; Policy risks; Foreign currency risk; Fierce competition.

Financials

Click Here for PDF format...