Summary of Investment

- Result of 2017 met expectations;

- Further Optimization of Business Structure;

- Continuous Extension and Expansion to Improve the Business Layout Throughout the Country;

Investment Advice

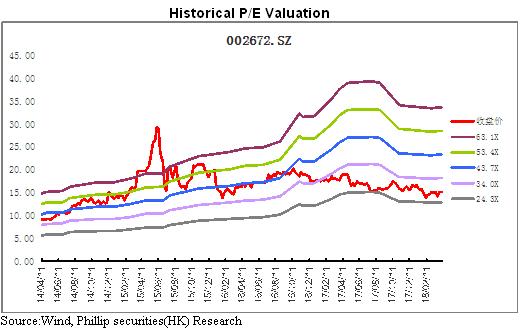

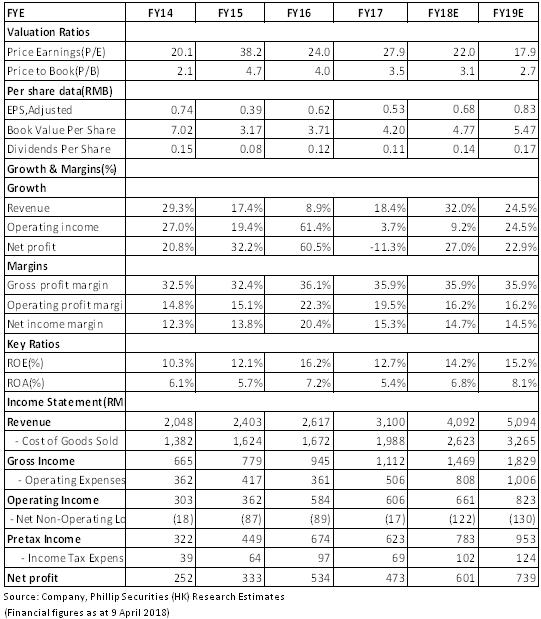

It is expected that the company's net profit of 2018 and 2019 will be 601 million and 739 million respectively; EPS will be as high as 0.68/0.83; and the price earnings ratio will reach 22.0/17.9 respectively, giving a target price of 19.38, with a "Buy" rating. (Closing price as at 9 April 2018)

Result of 2017 met expectations

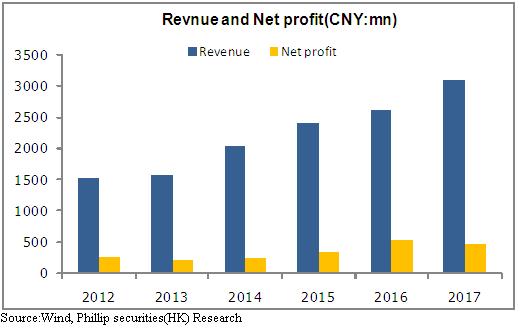

In 2017, Dongjiang Environmental recorded a revenue of RMB3.09 billion, with a year-on-year increase of 18.44%. The net profit attributable to the parent company was RMB473 million, a year-on-year decrease of 11.32%. And the net profit attributable to parent company excluding non-recurring items was RMB463 million, a year-on-year increase of 22.23%. EPS was RMB0.55, compared with RMB0.62 in the same period of last year. The result growth was in line with our previous expectations.

In terms of profitability, the overall gross margin was 35.88%, a year-on-year decrease of 0.24pct and the net profit margin fell by 4.2pct to 17.85% year-on-year, mainly due to the high base caused by the non-recurring items in the previous year, and the net profit excluding non-recurring items rose by 0.46pct. Period expense ratio was 18.79%, which was basically the same as that of the same period of the previous year. Thereinto, the administration expense ratio increased by 0.42pct while the financial expense ratio decreased by 0.49pct.

The net operating cash flow was RMB671 million, which was basically equal to that of RMB690 million of the previous year. The company has access to diversified financing channels, able to further reduce capital costs and optimize the capital structure by issuing ABS, green bonds, non-public issuance of stocks, establishment of industrial funds and other financing projects.

Deepened Reform of Main Business of Hazardous Waste to Further Optimize Business Structure

The company's business transformation achieved remarkable results. In the revenue structure, the treatment and disposal business of industrial waste contributed RMB1.167 billion, increased by 38.44% year-on-year; the gross margin decreased by 2.24pct to 47.74% year-on-year. The business revenue from industrial waste resource utilization was RMB1.182 billion, with a year-on-year increase of 49.33%; gross margin decreased by 5.64pct to 27.28% year-on-year, which was mainly hampered by the increase in the cost of upstream raw materials. That the growth rates of both revenues were higher than those of the overall revenue was mainly attributed to the release of capacity and the increase in demand for hazardous waste markets.

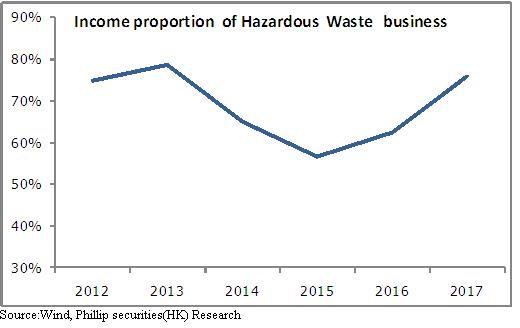

The proportion of hazardous waste revenue continuously increased. Contribution to revenue increased significantly by 13.4% from 62.4% of the previous year to 75.8%. The company's business structure was further optimized. In addition, the revenue from environmental engineering and service business was RMB280 million, an increase of 14.01% year-on-year. The gross margin was 25.72% (+1.71%). The amount of contracts was approximately RMB400 million, including a number of hazardous waste EPC projects. The new business model works, contributing to benefits step by step.

Intensify the Market Expansion and Improve the Business Layout over the Country

As at the end of 2017, the company is able to dispose of industrial hazardous waste of 1.6 million tons/year, occupying the most important industrial hazardous waste market in the regions of the Pearl River Delta, the Yangtze River Delta, and the central and western regions. It has signed a number of hazardous waste disposal projects within the year and will be able to dispose of hazardous waste of more 510,000 tons than before. During the period, the construction and commissioning of Hubei Tianyin, Zhuhai Yongxingsheng as well as Dongguan Hengjian Projects were finished; and technical renovation and extension of qualification to Jiangmen Dongjiang, Yongxingsheng and other projects were also completed. Jiangxi, Hengshui, Weifang, Xiantao, Quanzhou and other projects were carried forward one after another. If the project construction progresses smoothly, it is expected that many projects will be finished in 2018, thereby leading to a significant increase in hazardous waste capacity and overall result.

Further Intensify the Market Expansion and Improve the Business Layout over the Country. The company further strengthened the foundation for the development in the Pearl River Delta by acquisition of stock shares of Foshan Fulong Environmental Protection Project and Dongguan Fengye Environmental Protection Project; improved the business coverage of Beijing, Tianjin and Hebei by acquisition of Caofeidian Project in Tangshan, Hebei Province; and formed a strategic point radiating the southwest region by signing a strategic cooperation agreement with Sichuan Province Mianyang Municipal Government. Through acquisitions and mergers nationwide, business layout has been further consolidated and improved, which is conducive to its leading position in the hazardous waste industry and the further expansion of the scale of hazardous waste business as well as the sustainable growth of future result.

Risk Warnings

Market competition is intensified;

Price of raw materials is rising;

The project progress fails to meet expectations;

Financials

Click Here for PDF format...