Investment Summary

Air China's fourth-quarter results were lower than expected, resulting in a slight increase of 6.4% in net profit for the year. The main reasons are the fuel cost and the increase in impairment losses. The Chinese government is studying and formulating a new civil aviation pricing policy. First-tier cities will soon implement marketized fares for air routes and most large-scale air routes, which will be conducive to the restoration of the industry economy. Air China is expected to benefit deeply.

Last Year's Operating Results Fell Short of Expectations

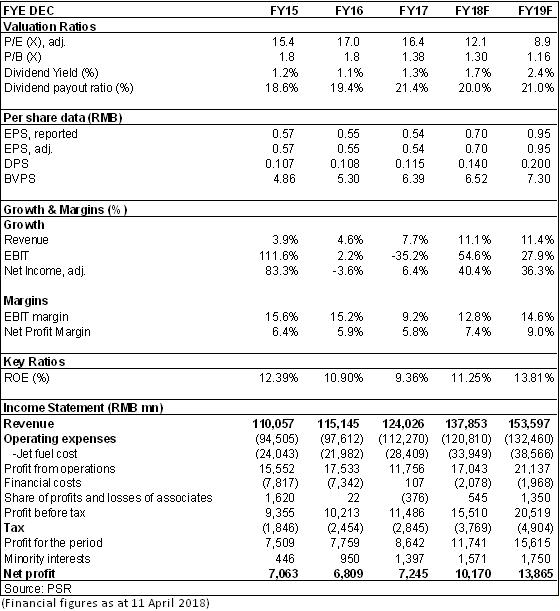

In 2017, Air China's annual turnover was RMB124.03 billion, an increase of 7.71% year on year, net profit of RMB7.244 billion, an increase of 6.39% year on year, and the earnings per share of 53.79 points. The final dividend was 11.497 points. The dividend rate was 21%. The main reason behind the lower earnings and market expectations was that the company's fourth-quarter net profit was worse than expected.

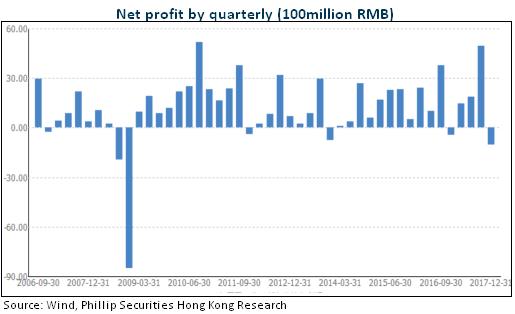

Fourth-quarter loss of about 1 billion

In the fourth quarter, the company recorded a loss of RMB1.04 billion, an increase of 154% over the same period of previous year. The single-quarter loss was only less than the third and fourth quarters of the 2008 airline limit. We believe the major reasons consist of the following aspects:

1) Gross margin in the fourth quarter was significantly narrowed by more than 6 percentage points to 17.4% due to rising fuel costs and maintenance costs. 2) Asset impairment losses in the fourth quarter were RMB570 million, an increase of RMB310 million over the same period. The asset disposal loss recorded was approximately RMB170 million. 3) Non-operating net income recorded a loss of RMB360 million, which was a profit of RMB200 million in the same period of previous years. 4) In the fourth quarter, the appreciation of the RMB exchange rate slowed down, and the exchange gains narrowed significantly.

Exchange gains improved significantly to boost performance

In 2017, the total cost for the period was RMB10.54 billion, a year-on-year decrease of RMB6.581 billion, of which sales expenses were RMB6.131 billion, an increase of 9% year on year, mainly due to the increase in labor costs and computer reservation fees. The administration expenses were RMB4.373 billion, an increase of 8.5% over the same period of last year, mainly due to the increase in labor costs.

Financial expenses amounted to RMB53 million, a year-on-year decrease of RMB7.441 billion or 99.3%, mainly due to a net foreign exchange gain of RMB2.94 billion, which represented a year-on-year growth of RMB7.172 billion, mainly due to the increase in the RMB depreciation during the period. The interest expense (excluding the capitalized portion) was RMB3.055 billion, a year-on-year decrease of RMB180 million.

The net loss of investment income in 2017 was RMB308 million compared with a profit of RMB22 million in the same period of last year, which was mainly due to an increase in losses of Cathay Pacific. This year's equity method confirmed that Cathay Pacific's investment losses were RMB986 million, and the loss increased by RMB327 million year on year.

The fare increase plan has been reported

Air China's RPK increased by 6.9% in 2017, and the ASK growth rate was 6.3%; the passenger load rate increased by 0.5pct. Due to factors such as the airport punctuality rate in 2017, domestic airline ticket prices increased slightly. However, due to the large investment in the air lines to the United States and Australia, and international airline ticket prices weighed on, dragging down the overall unit passenger-kilometer revenue by 2% year on year to RMB0.53.

The Chinese government is studying and formulating a new civil aviation pricing policy. First-tier cities will soon implement marketized fares for air routes and most large-scale air routes. Airline companies have submitted flight plans that need to be adjusted as required. The aviation moment reform aiming at improving the punctuality rate of flights will limit the delivery of air transport capacity, increase the demand for flight connection capacity, and favor the first-line shipping companies with well-developed hub airports. We expect that the aviation industry boom in 2018 will be based on this restoration.

The company plans to attract customers by improving the transit quality of the Beijing hub. This year, it plans to open two or more international express lines, similar to the international express lines from Beijing to Frankfurt and strengthen the rapid transfer capacity before the pivot point. As of the end of 2017, the company's fleet size reached 655 aircraft, a net increase of 32 aircraft compared to the end of 2016, with an average age of 6.53 years. In 2018, the company plans to increase the number of aircraft by 32, with Boeing 737 and Airbus A320/321 as its main models.

Valuation & Investment thesis

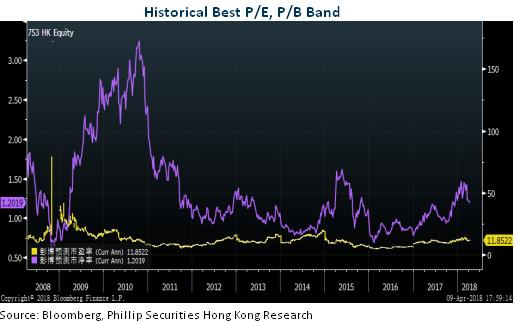

According to the latest result, we revised our estimate 2018/2019 net profit of AC to be 10.17/13.865 billion RMB. The target price is adjusted to HKD11.9, estimates 13.6x/10x P/E and 1.36/1.3x P/B in 2018/2019. “Accumulate” rating is given. (Closing price as at 11 April 2018)

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Highspeed railway diversion

Financials

Click Here for PDF format...