Investment Summary

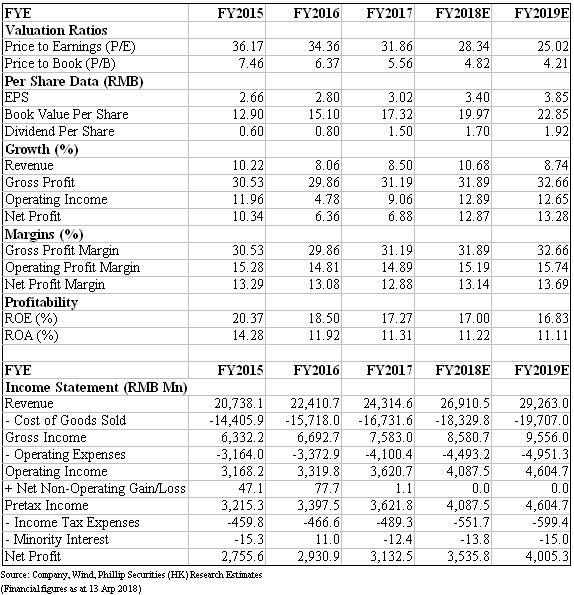

We highlight that: 1) stable growth in distribution business and notable hike in terms of health product segment; 2) rising selling expenses paving way for future growth; 3) composite ownership reform to accelerate development. We fine turn our model to factor into expenses hiking, therefore adjust EPS estimates to be RMB3.4 in 2018E. Given target PE 33x, we derive TP of RMB112. (Closing price at 13 Apr 2018)

Business Overview

Composite Ownership Reform to Accelerate Development

In 2017, Yunnan Baiyao Holdings Limited (YBH) introduced New Huadu and Jiangsu Yuyue (both private firms) as strategic investors, and three entities holds 45%/45%/10% of YBH respectively. Thus YBH and the listing company both transfer into enterprises without one actual controller. After adjustments in 2017, we expect that the reform will further motivate its staff and enhance company competitiveness.

Distribution Segment Achieving Stable Growth

YNSYY reported revenue of RMB14,494mn (+7.5%) in 2017. We expect that this segment will recover gradually in 18H2 after further digesting effects of two-invoice system. The distribution network has covered all county-level hospitals and some hospitals in part of developed towns, with expanding to combining pharma chains, drugstore trusteeship and online drug sales to achieve channel synergies. The company currently has entered into all mainstream e-commerce platforms and explores Wechat business to broaden distribution network.

Manufacturing Segment

This segment reported revenue growth of 9.7% YoY. (1) Medicine department: this part recorded revenue of RMB5,043.5 (+2.56%), weaker than we thought. The company continues to upgrade its distribution network to comply with two-invoice system requirements. On products, it is trying to integrate internal resources to enrich product mix to adapt to current increasing demand for medicinal consumer goods, including developing healthcare products like steam eye-masks. (2) Health product department: it reported revenue of RMB4,361.1mn with YoY growth of 16%. Health products` has covered the whole country market, even county level markets in some developed regions. Meanwhile, the company proactively to facilitate e-commerce growth, given it set up an e-commerce operation center in Hangzhou city and built flagship stores on mainstream platforms.

Efficient Promotion with Rising Selling Fee

Selling expenses rose by 30% YoY mainly due to more expenditure on market maintainance and promotion. The company focuses on new media channels, such as internet, building advertising and public events, to improve brand popularity among young generations. The company takes advantage of popular IP to develop related products, which helps to increase product exposure to the public. In 2017, the company launched two series of products under two popular TV series (`三生三世十裡桃花`, `春風十裡不如你`). It also hosted sport event `雲南白藥愛跑538`, which was also hosted in cities including Changsha, Chongqing, Wuhan, etc. We expect in future selling expenses to be in a climbing trajectory.

Investment Thesis, Valuation & Risk

Our model indicates a target price of RMB112.0. Considering rising selling expenses, we estimate 2018E EPS to be RMB3.4 per share (vs. RMB3.55 previously). We see current PE of TCM sector is around 33.5x-37.6x. With target PE 33x, we give 2018E Target price of RMB112.0. Risks include: Effects from Two-invoice system; Fierce competition in health product industry; Composite ownership reform fail expectation.

Financials

Click Here for PDF format...