Summary of Investment

-Sanitation business has become the driving force of income growth and structural transformation;

-The funds in hand after fund-raising were abundant, providing strong momentum towards development;

Investment Rating

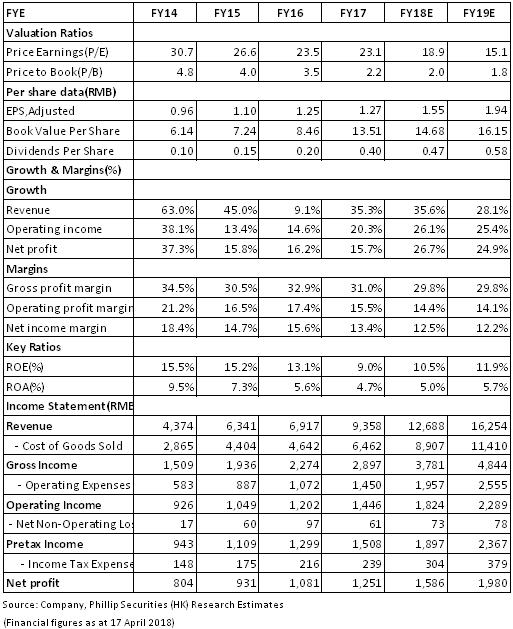

The development prospect of sanitation business of the company and cooperative development under the industry chain are optimistic. The company is now equipped with abundant funds and strengthened operation duration ability after the completion of directional private placement. We estimate, from 2018 to 2019, the net profit of the company will reach RMB1586/1980mn, respectively, EPS of 1.55/1.94, equivalent to a PE of 18.9/15.1. We give a target price of RMB37.2 and the Buy rating. (Closing price as at 17 April 2018)

The Growth of Net Profit is less than that of Revenue

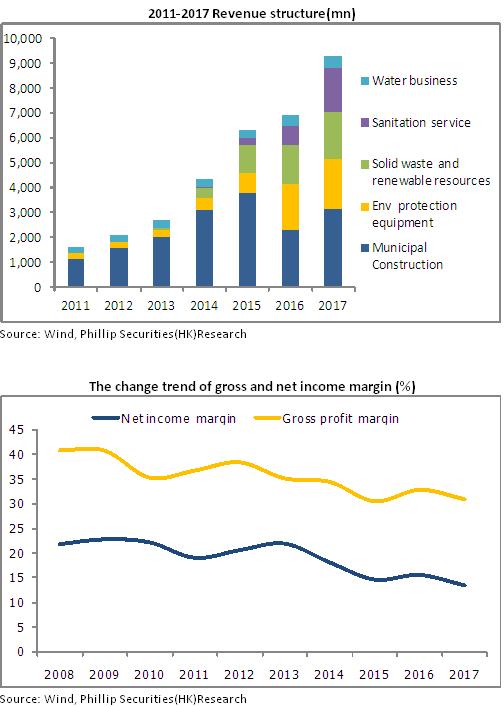

In 2017, the operating revenues of Tus-Sound accounted to RMB9,358 million, representing a year-on-year increase of 35.3%. The net profit attributable to parent company stood at RMB1,251 million, representing a year-on-year increase of 15.7%, and a year-on-year increase of 11.65% after deduction of non-recurring items. Earnings per share were RMB1.27. The figure was RMB1.25 in last year. The performance was below our expectations. Specifically, the municipal construction revenue was RMB3,162 million (+36.6%) and the gross margin was 29.8%; the revenue from environmental protection equipment was RMB1,988 million (+9.4%) and the gross margin was 53.4%; the revenue from sanitation service business was RMB1,788 million (+125.4%) and the gross margin was 17.1%; the revenue from recycling of renewable resources was RMB1,733 million (+21.1%) and the gross margin was 22.2%.

With respect to revenue structure, the revenue from sanitation service business accounted for 19%, the revenue from renewable resources business accounted for 19%, the revenue from environmental protection equipment accounted for 21%, the revenue from solid waste and water services accounted for 6.5% and the revenue from traditional solid water municipal construction business accounted for 34%. The revenue from environmental service business including sanitation services and renewable resources over the period exceeded the construction revenue, representing the further optimization of business structure of the company.

In terms of profitability, the overall gross margin was 30.95%, a year-on-year decrease of 1.93pct and the net profit margin fell by 2.11pct to 13.56% year-on-year. The period cost rate increased by 0.78pct to 15.19% year-on-year, among which the sales expense ratio was 1.66%, a year-on-year decrease of 0.04pct, the administration expense ratio was 8.86%, a year-on-year increase of 0.96pct, and the financial expense ratio was 4.67%, a year-on-year decrease of 0.15pct. In a word, the decrease of gross margin and net profit margin and the fast growth of the period costs resulted in that the growth of net profit is less than that of revenue.

Promote PPP Business, Build New Points of Growth

The performance in solid waste market expansion was significant. The company has entered into the contracts of several household waste incineration power generation PPP projects in Baicheng, Aksu, Fuquan and Jinan, disposal projects of kitchen waste in Changzhi, Jingzhou, Chuxiong and Yishui, as well as biomass cogeneration projects in Heilongjiang and Inner Mongolia, with PPP contracts in hand of more than tens of billions of fund. Q1 in 2018 witnessed a good beginning of the company with 31 projects newly signed, and about RMB15 billion of total investment. The newly added projects are mainly PPP projects in sanitation services and solid waste. The company actively strived to develop PPP business to build new profit growth points, constructing a solid base for the sustained growth of performance.

Bright Prospects for Sanitation Services and Renewable Resources

The sanitation service business in 2017 has presented a booming growth, with a year-on-year increase of 125% of revenue to RMB1,788 million. Its revenue from sanitation service business lies in the forefront of the industry. The number of newly signed operation service contracts of Internet sanitation service was 235 with the annual amount of about RMB1,031 million in total and the total contract value of RMB12.316 billion during the operation of projects. As at the end of 2017, the number of contracts of sanitation services performed by the company was 487, the annual contract value was RMB2.3 billion and the total contract value was RMB31.3 billion during the operation of projects. The company has started to establish the strategic layout of sanitation service business since 2014. Groups of sanitation service industry with the core of Internet sanitation service operation have begun to take shape. Sanitation service business is expected to keep a high momentum in the future, driving the further optimization of overall business structure of the company.

The e-waste annual disassembly capacity has reached 22.59 million units per year in 2017, ranking the first place at home in the scale of disposal of e-waste. The company continues establishing the layout in recycling industrial parks, discarded automobiles, dangerous waste, intensive processing and other fields offline, optimizing and promoting the renewable O2O platform online, and improving the profitability of renewable resource business by integrating industry resources and expanding the industry chain.

Fund-raising Brings about Abundant Funds for Development

In August 2017, the company raised the funds of RMB4,589 million through private placement. The funds were used in integrated platform of sanitation services and service network construction, as well as the reconstruction of sanitation vehicles in Hubei, waste incineration power generation, projects of kitchen waste and supplementary current funds. The fund-raising has brought abundant funds for the business development and project investment, which helps to strengthen capital strength, optimize financial structure and improve the core competitiveness and operation duration ability.

Risk Warnings

The expansion and progress of projects fail to meet expectation;

Risk of intensified market competition;

Industry policy risk;

Financials

Click Here for PDF format...