Investment Thesis

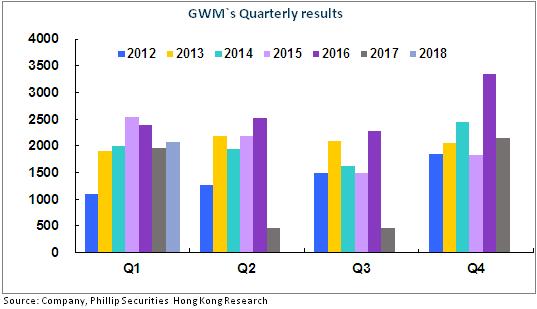

Result of Q1 in 2018 Rebounded Slightly

Initial Success of Cost Reduction & Benefit Growth

Improving Sales Structure and Export Performance

Implementation of Strategy for New Energy Development is Underway

Result of Q1 in 2018 Rebounded Slightly

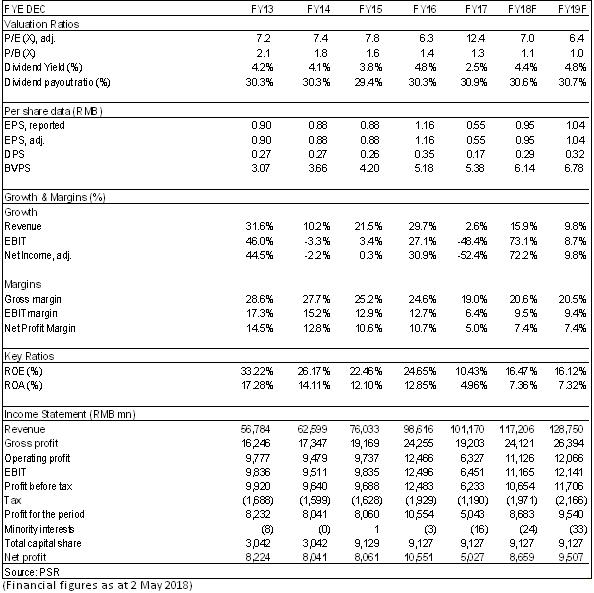

In 2017, Great Wall Motor recorded RMB101.17 billion in revenue, up 2.6% yoy, and a slash of 52.35% in net profit attributable to parent company, at RMB5.03 billion, as well as RMB0.55 of EPS. This slump of the result is mainly caused by heavy promotion of the old products in the first half year, below-scaled sales of new products (which led to the reduced gross profit, down 6 ppts), and the above-expectation advertising effect of new arrivals.

According to the result report of Great Wall Motor in Q1 2018 (China Accounting Standards), the revenue grew by 14.0% yoy to RMB26.57 billion; the net profit attributable to parent company increased by 6.5% yoy to RMB2.08 billion; and the EPS stood at RMB0.23. Compared with EPS of the last year, which stood at RMB0.21, the result exceeded market expectancy slightly.

Initial Success of Cost Reduction & Benefit Growth

The profitability of the company in Q1 has stopped declining, and has continued to increase: the net profit margin reached 7.96%, down 0.5 ppts yoy and up 2.2 ppts qoq; the gross margin hit 20.44%, down 1.3 ppts yoy and up 1.4 ppts qoq. Reasons for this are as follows:

1) Excellent sales performance of the new brand, WEY, and decreased costs of the components have relieved pressure of the gross margin. Although the Q1 gross margin, at 20.44%, plunged by 1.3 ppts, it has increased greatly, from 15%-16% in the middle of the previous year, by 1.4 ppts, when compared with that of Q4 in the previous year.

2) Capitalization of the R&D costs cut the administration expenses by 51% to RMB0.625 billion; advanced CAFC negative points offset the sales expenses, making it grow by 49% to RMB1.17 billion yoy; and interest expenses lifted the financial expenses to RMB0.15 billion, representing 169% growth. The three expenses in total dropped by RMB0.16 billion, slashing the expense rate by approximately 1.4 ppts.

Improving Sales Structure and Export Performance

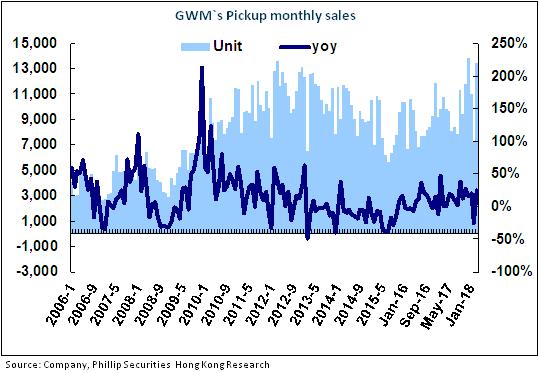

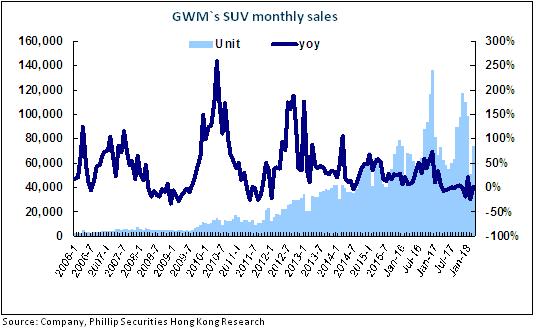

In Q1, Great Wall Motor reported sales of 2,567 thousand vehicles, up 0.97% yoy, suggesting the upgrading sales structure. Among them, sales of HAVAL dropped by 18.56% to 180 thousand; sales of WEY, the high-end brand, reached 430 thousand; and the monthly sales of VV5 and VV7 arrived at approximately 7 thousand, respectively. New fuel vehicles of 2018 include two types that entered the market in March, namely, H4 (HAVEL series) and VV6 (WEY series). Moreover, the export sales recorded excellent performance in Q1, increased by 51% to 10 thousand.

Implementation of Strategy for New Energy Development is Underway

Since the company lags quite behind in adopting strategies to develop new energy automobile, it is now picking up pace in this regard. Apart from the transfer right for new energy points gained by becoming a shareholder of YOGOMO, the company has also acquired exclusive selling right for part of the lithium concentrate by buying a share of Pilbara (Australia) with RMB0.146 billion, and attached more importance to new energy automobile in accordance with the cooperation agreements with BMW. The first electric version of its new energy automobile, C30EV, entered the market in last May, and recorded sales of 2,718 last year; while the first type of hybrid electric vehicle , P8 (WEY series) will make its debut in the automobile exhibition in Beijing in April, and the electric sedan will also be unveiled in the second half of 2018.

In terms of technology, the company plans to conduct research and development of the frames, EV, HEV and PHEV, at the same time and work on the development of FCV. In the future, it will invest RMB30 billion in research and development of the new energy vehicle, smart car and vital components. By doing so, the R&D expense will be transformed into capital, which will lessen the operation pressure in the short term.

Investment Thesis

We believe that Great Wall Motor has embarked on its right path to the transformation and upgrading and is improving its profitability. Therefore, we expect that the company will be excelled in its performance in 2018 and will accelerate its development after implementation of the new energy strategy in 2019.

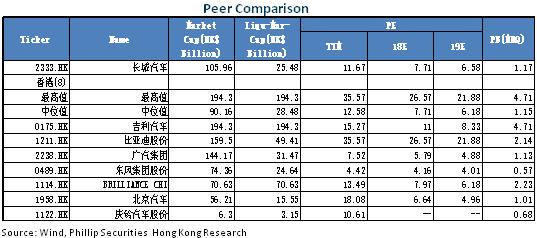

In terms of valuation, we adjust our target price to HK$9.6, equivalent to 8.2/7.5 P/E ratio in 2018/2019. We maintain the rating of “Accumulate”. (Closing price as at 2 May 2018)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle project is poorer than expectations

Financials

Click Here for PDF format...