Investment Summary

SPH announced FY17&18Q1 results, beat our expectation. We see that momentum of manufacturing maintain strong and growth of retail business steps up. We highlight that BE test will increase sales volume and ASP in future, thus we adjusted EPS estimation to be RMB1.48/1.69 in 18E/19E. Assuming target PE 14.25x (roughly par to 2-y historical PE), we get target price of HKD25.5. (Exchange rate= 0.823 RMB/HKD) (Closing price at 7 May 2018)

Business Overview

Robust FY17& 1Q18 results. In FY17/18Q1, the company realized revenue of RMB130.8bn/36.69 (+8.35%/9.83% YoY), NP attributable to shareholders of RMB3.52bn/1.02bn (+10.14%/2.07% YoY) and NP excluding non-recurring items of RMB2.65bn/996mn (+2.73%/6.08% YoY).

Manufacturing kept rapid growth. This segment achieved revenue of RMB14.99bn (+20.71% YoY) with GPM rising by 3.3pp to 53.86%. 28 products reported over RMB100mn sales and 60 core products reported sales of RMB7.98bn (+14.42% YoY) and GPM 71.28% (+2.65pp). In 18Q1, the company realized sales of RMB4.96bn (+30.82% YoY) and we expect growth momentum will maintain in 18E19E.

Retail business stepped up. In 2017, the company realized revenue of RMB5.64bn (+9.44% YoY) with GPM of 16.36% (+0.84pp). In 18Q1, retail business continues high growth given segment revenue rose by 12.78% YoY to RMB1.44bn with GPM of 15.95%. As up to end 2017, SPH operated 1892 chain pharma stores (1247 of which were self-owned) and continued to expansion hospital coverage. Based on its e-commerce platform (上药云健康) to explore e-prescription business, SPH sighed strategic cooperation agreement with Tencent, which facilitates a integrated system involving acquirement of prescription, drug delivery and value-added services. During 2017, the company disposed over 2mn e-prescription and cooperated with 214 hospitals. Meanwhile, it continues to enhance DTP network and now operates over 70 DTP pharma stores in China after acquiring Cardinal China. We highlight that retail business will continue high growth given SPH's rich drug resources and strong channel advantage.

Distribution segment in line with expectation. Influenced by two-invoice system, the distribution segment slowed down in short term. It reported revenue of RMB115.86bn/31.42bn (+6.93%/6.66% YoY) and GPM of 6.12%/6.48%. SPH is the largest pharmaceutical importer and distributor in China with 223 imported products. To maintain profitability of distribution business, the company makes efforts to improve product structure, control expenses and explore hospital supply chain business (managing 226 hospital pharmacies). In long run, we highlight TIS will increase industry concentration and improve efficiency. And we expect distribution business to rebound in 18H2.

BE test provides future driver. China government published policies (《關於改革完善仿製藥供應保障及使用政策的意見》) to facilitate the replacement of original imported drug with generic drug. It indicates that qualified generic drugs should be included into public purchase lists and be paid just as original drugs. This means that part of market share of original drugs will be taken by generic drugs, and players who pass BE test earlier are likely to grasp more market share. Meanwhile, ASP will increase given the generic drugs will be sold at price of original drugs, which is usually higher than related generic drugs now. So we see potential hike both in volume and ASP after passing BE test. SPH now has 70 products in BE test and invested 20.8% of R&D expenditure in BE test (R&D expense rose by 20.79% YoY, 5.27% in manufacturing sales).

Valuation and Risks

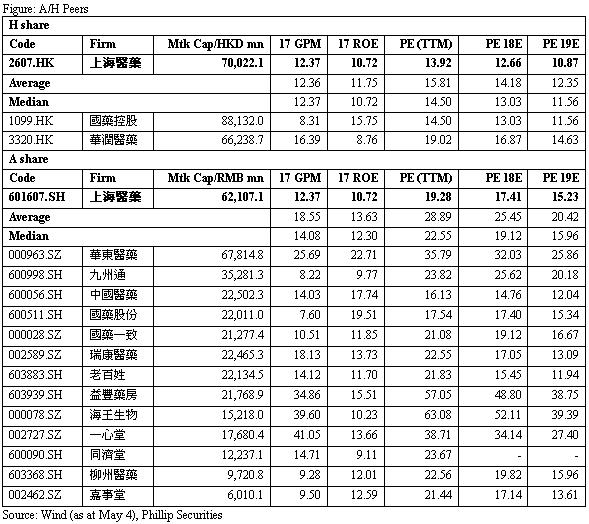

Our model gives target price of HKD25.5. A share peers valuation now is around PE 22.5-28.9x, while PE 14-19x for H share peers. We assume 2018 target PE to be 14.25x (roughly par to 2-y historical average) and estimate 18E/19E EPS to be RMB1.48/1.69 to get target price of HKD25.5. Risks include: 1) Two-invoice system's effect on inventory allotment business; 2) Integration of Cardinal fails expectation; 3) BE test progresses not well; 4) Policy risk. (Exchange rate= 0.823 RMB/HKD)

Financials

Click Here for PDF format...