Investment Summary

BYD's 2017 and 2018Q1 result declined by 19.5% and 83% yoy due to the change of NEV subsidy policy. We expect 2018 H1 to be a low point for BYD's automotive business. Still, with new energy vehicles and traditional fuel-engined vehicles exerting their power in H2, the Company's net profit is expected to bottom out in H2 We give BYD Accumulate rating. (Closing price as at 10 May 2018)

Summary of Result

BYD has released its 2017 annual report and 2018 first quarter report

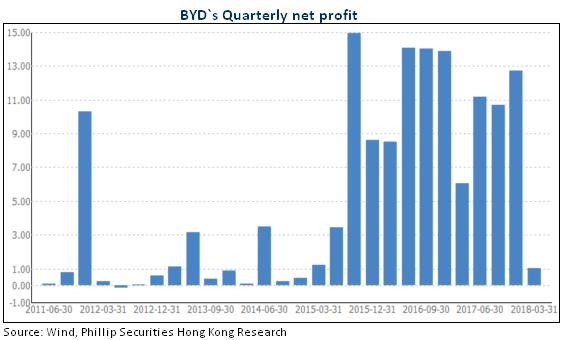

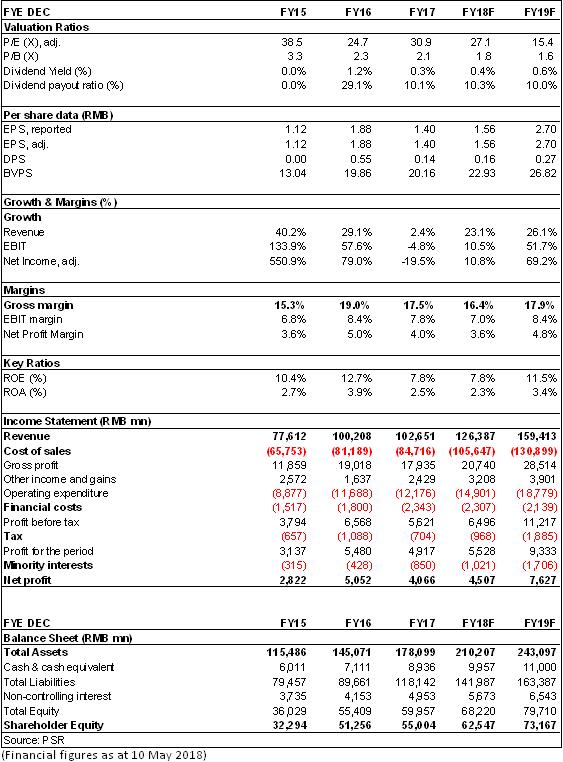

In 2017, the Company recorded revenue of about RMB105.9 billion, an increase of 2.4% yoy; net profit attributable to parent company stood at RMB4.07 billion, a yoy decrease of 19.5%, which fell in the lower end of previous result forecast interval, equivalent to EPS of RMB1.4. The final dividend per share stood at RMB0.141 with dividend payout ratio of about 10%.

The company recorded revenue of RMB34.74 billion in the first quarter of 2018, a yoy increase of 17.5%; net profit attributable to parent company stood at RMB100 million, a yoy decrease of 83%, whereas it recorded net profit of RMB606 million in the same period last year.

The Margin Level Is not Ideal as the Subsidy Declines

By different departments, in 2017, the strong growth of mobile phone business has made up for the decline of the automotive business: annually, three major business segments, namely automotive and related products business, mobile phone parts and assembly business, rechargeable batteries and PV business revenues accounted for 53%, 39%, and 8% of total revenue, respectively. The ratio of profit before tax was 14.8%, 40.4%, and 44.7%, respectively, up 0.7 ppts, up 21 ppts and down 22 ppts, respectively. Overall gross margin of the year fell by about 1.4 ppts to 19%.

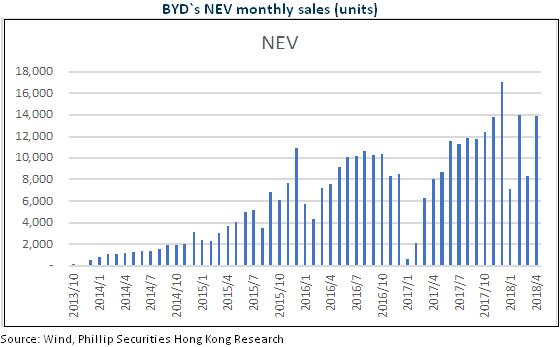

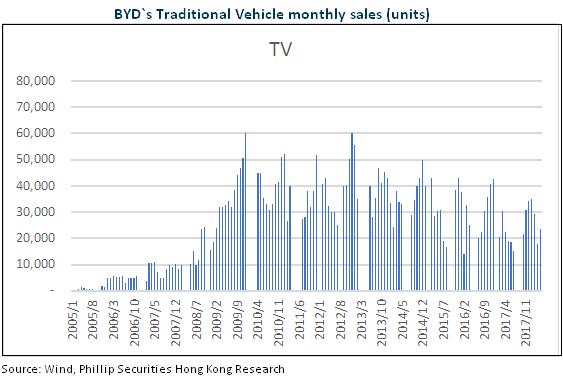

Affected by the change of subsidy policy in 2017, BYD's new energy vehicles recorded more than 110,000 units sold, an increase of 15% yoy, which was slower than the industry average. The new energy vehicle recorded revenue of about RMB38.55 billion, a growth of 13% yoy, whose proportion of total revenue increased to 37.55%. But in the traditional fuel-engined vehicle segment, sales fell by about 25% yoy due to the life cycle of older models and late launch of new models.

As a result of subsidy decline in 2018Q1, although the Company's new energy vehicles recorded robust sales growth, its profitability was obviously under pressure. Its mobile phone shell business margins also showed a small decline because of the slowdown in its main customer's orders. The company's overall gross margin fell sharply by 3.9 ppts.

Large Increase in Financial Expenses Encroaches on Profit

In terms of period cost, the Company's sales expenses increased by 0.6 ppts in 2017, the administration expenses reduced by 0.2 ppts, both of which basically remained stable. Because the new energy vehicle's accounts receivable turnover period lengthened, the Company's capital pressure has increased. Financial expense rate increased by 1 ppts or RMB540 million to RMB2.34 billion.

In 2018Q1, the three expense ratios reduced by 0.3 ppts, and increased by 0.2 ppts, and increased by 1.5 ppts, respectively. Among them, due to exchange rate losses and sharp increase in interest expenses, financial costs increased by 114% to RMB810 million yoy.

2018H1 Will Be a Low Point for its Automotive Business

The Company expects net profit attributable to parent company to fell 83%- 71% in 2018 H1 yoy, to RMB300 million-RMB500 million, which suggests the net profit of the second quarter will be within RMB200 million- RMB400 million, a yoy decline 55%-82%. The main reason is that the Company's new energy vehicle subsidy in the second quarter is still in a buffer period. However, with the implementation of the new subsidy standards from June 11, the subsidies on the Company's pure EV passenger car of long range, high energy density, and low energy consumption will be greatly increased. Its models will have a maximum of 30% more subsidy yoy.

As for new models, the Company has launched the Qin EV450, e5 450, Song EV400 and other face-lift models, all of which have been equipped with ternary batteries, resulting in a significant increase in range. In 2018, the Company will also introduce a new generation of Tang, Qin, compact pure electric SUV Yuan and PHEV version of Song Max. Former Audi Head of Design, Wolfgang Egger, specially designed the Dragonface for the Company, whose market response is quite enthusiastic. Song Max's monthly sales have surpassed 10,000 units, featuring sufficient orders currently. In the future the Company will also launch a new fuel-engined version of Tang and Qin, we think which will propel BYD's traditional fuel-engined vehicle business back to growth road.

Investment Thesis

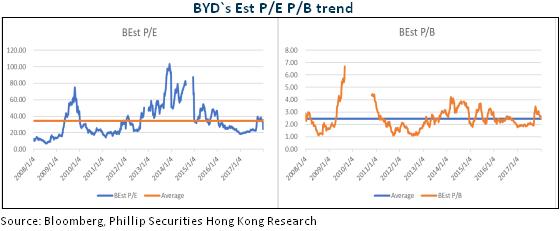

As the latest estimates, we adjusted the expected EPS of 2018 to RMB1.56, and add our 2019 expected EPS to RMB 2.7. Thus, we revise the target price to HKD60, which corresponded to 31/18x P/E and 2.1/1.8x P/B ratio for 2018/2019. We give the rating of “Accumulate”. (Closing price as at 10 May 2018)

Risk

Sales of new energy vehicles is not as good as expected

Cloud Rail business risk

Slow-down of Hand-set components business

Financials

Click Here for PDF format...