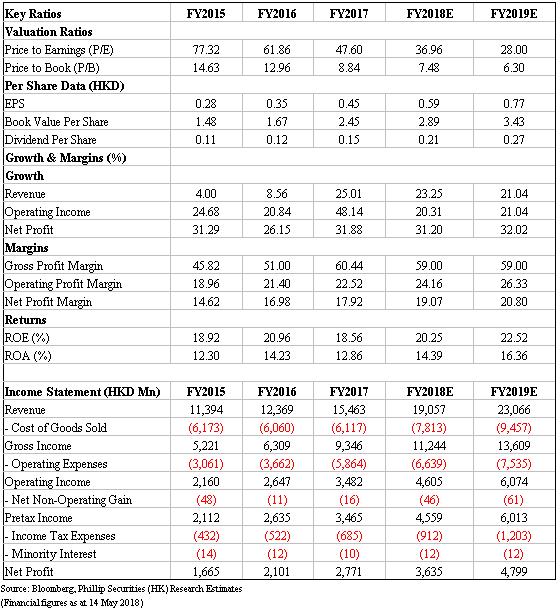

Investment Summary

Since April, the company has acquired two clinical trail approvals, one drug registration approval and passed consistency evaluation of Azithromycin tablets. We expect further progresses of pipeline and continuously rapid growth of innovative drugs. We maintain target price of HKD24.8, implying 18E PE 42x, with EPS estimation of HKD0.59/0.77 in 18E/19E. (Closing price at 14 May 2018)

Business Overview

Two products gained clinical trail permissions. 1) Q101-Pegylated Recombinant Human Interferon-α2a for Injection: it is used alone or in combination with other drugs for the treatment of adults with chronic hepatitis B; and used in combination with ribavirin for the treatment of adults with chronic hepatitis C with no previous treatment. 2) Vinorelbine Tartrate Liposome Injection: Vinorelbine features high anti-cancer activity. It can be used alone or in combination with other drugs clinically for the treatment of non-small cell lung cancer, breast cancer, ovarian cancer and malignant lymphoma. The product can significantly suppress the growth of various solid tumours in a dose-dependent manner, with efficacy increased by at least four times.

Azithromycin tablets has been granted consistency evaluation approval by CFDA, which means CSPC is the first one passing the consistency evaluation for this type of drug in China. Azithromycin is used for the treatment of various bacterial infections, including bronchitis, pneumonia, skin and soft tissues infections, otitis media, sinusitis, pharyngitis and tonsillitis. Azithromycin tablet is one of the key anti-infective drugs of the Group, having the largest market share of the same type of drug in domestic market. Passing consistency evaluation implies its availability as a clinical alternative for the originator drug and potential sales volume hike.

2018 growth momentum will come from: 1) NBP injection is expected to grow as being included into NDRL, due to its further expansion to county-level hospitals; 2) Strong growth of oncology portfolio. The company continues to enlarge the sales team (720 salesmen in 2017 while 1200 salesmen in 2018E). We expect oncology portfolio to report high growth given its expanding sales team and network. 3) Albumin-bound paclitaxel gained registration approval in Feb. According to CSPC management, this product will be sold at only 60% of original drug and may contribute to over HKD1bn income in 2019E. Given CSPC's intensifying channel advantage and favorable price, albumin-bound paclitaxel is competitive to win considerable market share.

Valuation Thesis & Risks

Our model derive TP of HKD24.8: with EPS estimation of HKD0.59/0.77 in 18E/19E, we maintain our target price of HKD24.8, implying 2018 PE of 42x. Risks include: rising selling and R&D expenditure; M&A or R&D fail expectations; policy risks.

Financials

Click Here for PDF format...