Investment Summary

We believe that Geely will continue to be benefited from the dividends generated by successful strategies. The Company shows advantages in epitaxial leapfrog development and export market. Several times of increases in the management's holdings also demonstrate its considerable confidence.In terms of valuation, we increase the profit forecast, adjusting our target price to HK$36, equivalent to 18/13 P/E ratio in 2018/2019, and we shall give the rating of Buy. (Closing price as at 16 May 2018)

Growth of sales volume in April remains strong

The total sales volume of Geely in April increased by 49% yoy and 6% mom to 128,817 units, which is far higher than 9.6% of the industry average. The sales volume and export volume in the Chinese market increased by 47% and 187%, respectively. In the first 4 months of 2018, the total sales volume rose by 41% yoy to 515,000 units, completing 33% of the annual sales volume target (1,580,000 units).

Gross profit is expected to increase along with the increases of models with a monthly sales volume of over 10,000

There are four models of Geely with a monthly sales volume of over 10,000 in 2017, two of which reported a sales volume of over 20,000. Since the beginning of 2018, the main models remain attractive and the newly launched models are gaining popularity step by step. It is expected that the number of models with a monthly sales volume of over 10,000 will increase to 5 or 6, and the number of models with a sales volume of over 20,000 will increase to 3. The monthly sales volume of Imperial is about 22,000 units and that of Bo Yue is about 24,000 units with both GS and GL reporting robust increases. The sales volume of Vision X3 has experienced a rapid growth since its launch with a monthly sales volume of over 10,000. The only disadvantage is the decrease of sales volume of high-end sedan Bo Rui. It is expected that the ASP of Geely will remain stable and increasing due to the contribution of new models in the increase of sales volume, and hopefully, the gross profit will further increase along with the increase of popular models.

Net profits in 2017 achieved double growth

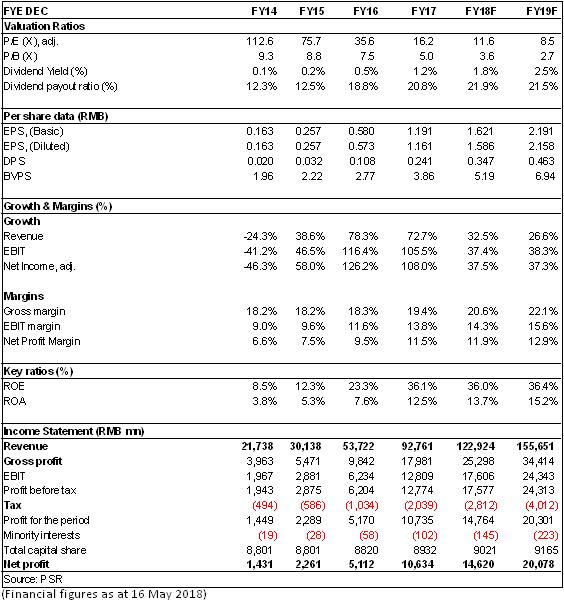

The financial results of the Company in 2017 outperform the market consensus and our expectation. The net profits were RMB10.6 billion, achieving double growth (+108%) for the second year. The diluted earnings per share was RMB1.16, the dividend paid was HK$0.29 and the dividend rate was 20%. The total revenue increased by 73% to RMB92.96 billion and the total sales volume increased by 63% yoy to 1,247,116 units.

The net profit growth is higher than revenue growth, reflecting that the Company's profitability has seen improvement. While the revenue growth is higher than sales volume growth, demonstrating that the average price of single vehicle of the Company has increased. The gross profit grew by 1.1 ppts to 19.4%, the net profit margin increased by 2 percentage points to 11.5% and the price of single vehicle increased by 7% to RMB73,500. The three expense ratios reduced by 0.3, 1.6 and 0.9 ppts, respectively, indicating the influence of scale benefits. The Company early redeemed the senior notes of USD0.3 billion at the rate of 5.25% and issued the bonds of USD0.3 billion at the rate of 3.625%, which is expected to save the interest expenses of more than 60 million.

The Company remains the strong efforts to launch new models

The Company will remain the strong efforts to launch new models and considerable new models will be unveiled in 2018/2019. Facelift versions of the existing models will be launched successively. Besides, Geely will launch more than 8 new models in 2018, including LYNK&CO 02 and 03, two models of new energy vehicle, 2 models of sedan, 2 models of SUV and a model of MPV. And in 2019, the Company will continue to launch no less than 5-6 brand-new models, enriching its product portfolio. By the end of 2017, the number of dealers of the Company has reached 962, 82 of which are LYNK&CO. The network of dealers of LYNK&CO will be enlarged to about 200-300 in 2018. The second plant of engine of the Company will be put into operation by the end of the year. A joint venture plant of transmission set up with Aisin will ensure the supply and the productivity of LYNK&CO will be released gradually, helping to fulfill the potential of sales volume in the future.

Investment Thesis

In terms of valuation, we increase the profit forecast, adjusting our target price to HK$36, equivalent to 18/13 P/E ratio in 2018/2019, and we shall give the rating of Buy. (Closing price as at 16 May 2018)

Financials

Click Here for PDF format...