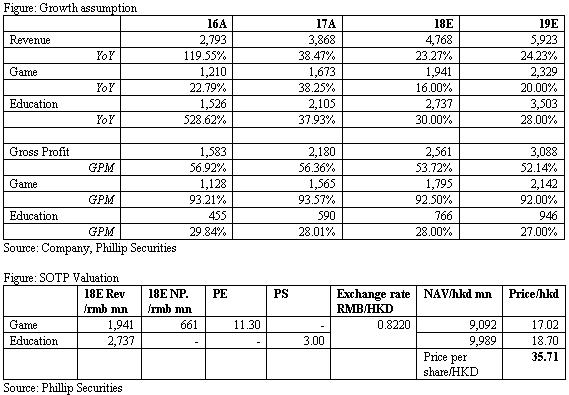

Investment Summary

Recently, Netdragon acquires an international education website EDMODO. We highlight that education business steps up with lowering loss and wining domestic and overseas tenders. We expect mobile games to contribute to stable growth of game segment. Based on our growth assumption and industry valuation, we give education segment target PS 3x, game business target PE 11.3x, thus derive TP of HKD35.71. (Closing price at 18 May 2018)

Business Overview

Acquiring international education online platform. The company announced the acquisition of EDMODO with a consideration of USD137.5mn. EDMODO is a global education online platform to K-12 schools targeting teachers, students, administrators and parents. The EDMODO network enables teachers to share resources, distribute quizzes and assignments, and connect with students, colleagues, and parents. Its registered users amounted to 90mn with 6mn DAU covering 192 countries. EDMODO now starts monetization through advertising, given advertisement revenue reached USD1mn in 2017. We are positive on the synergies among Netdragon's current products (education software and hardware) and EDOMODO's large user base, which is believed to form great monetization potential in future.

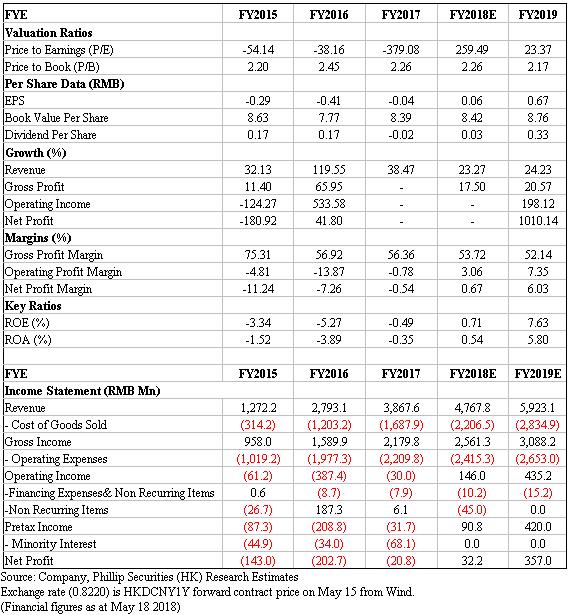

Education business to step up with loss narrowing. Education business generated revenue of RMB210mn with 37.9% YoY growth. In terms of international business, Promethean reported revenue of RMB1.78bn up by 32% YoY and EBITDA RMB53mn (2016: -50.6mn), with increasing market share in US, Europe, Middle East and Africa. In domestic market, its business develops quickly given revenue up by 82.2% YoY to RMB330mn in 2017. The installation amount of flagship product 101 PPT now reaches over 1.2mn.

Wining domestic and overseas tenders. For international market, we expect the company to win more government purchase orders. After Russian contract (worthy of USD30mn) last year, Netdragon won its Phase II order to provide interactive learning technologies with contract amount of USD60mn in Mar 2018, which is expected to be recognized in 18H2. Currently, the company is actively preparing for tenders in Turkey and Malaysia. We estimate that GPM of projects in developing countries may be slightly lower, but popular large screen display with higher GPM will help to maintain Promethean's overall GPM around 30%. For domestic market, Netdragon realized sales of RMB279mn in 2017 and Q4 revenue grew dramatically to RMB99.8mn. We expect the company to enhance promotion in domestic market and proactively to explore cooperation with Chines schools and government.

Mobile games contribute to high growth. Benefiting from mobile games` quick growth, game business generates revenue of RMB1.67bn up by 48.2% in 2017. We highlight the good performance of flagship IPs: 1) Eudemons achieved record high with revenue up by 48.2% YoY to RMB1.37bn. Eudemons PC version continued to deliver eight months of gross billings over RMB100mn, while pocket version also reached a record high in Sep 2017, ranking as `top ten most outstanding app by billings` on Tencent Open Platform. Besides, Eudemons Online Mobile, which is cooperated with Kingsoft, attained much popularity since it has been launched in Oct 2017 and contributed to a gross billing of over RMB100mn in first month, ranking as one of the `top five most outstanding app by billings` on Tencent Open Platform for four months. 2) Heroes Evolved, another flagship IP, sustained strong momentum given 17H2 income doubled, with rapid user ramp-up. In future, the company will insist core IP strategy to maximize IP value and launch more mobile games in 2018. It is worth mentioning that a new version of School of Dragons (a MMORPG based on DreamWorks Animation's How to Train Your Dragon franchise) will launch in 18H2 for the propaganda of HTTYD new movie. We expect game business maintain stable growth during 18E/19E.

Investment Thesis & Valuation

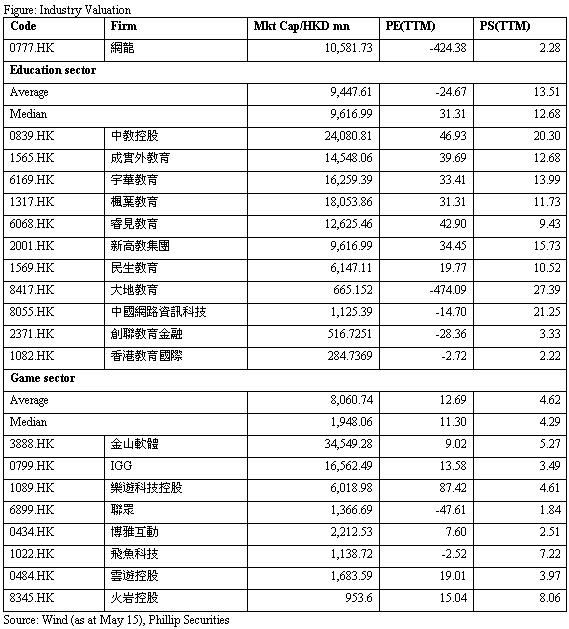

We appreciate the great potential of education business and estimate game segment to grow steady. Based on our topline growth assumption, 11.3x target PE for game business and 3x target PE for education business, we increase TP to HKD35.71 considering exchange influence. (Exchange rate=0.8220) (Closing price at 18 May 2018)

Risks

Fail to attain international government purchase orders;

Domestic education business fail expectation;

Game business fail expectation;

Fierce competition.

Financials

Click Here for PDF format...