|

|

|

*Advertisement* |

|

|

|

|

|

5 Jun, 2018 (Tuesday) |

TCL MULTIMEDIA(1070)

Analysis:

TCL Multimedia Technology Holdings (1070) announced that it has entered into the Equity Transfer Agreement, pursuant to which it will acquire 100% equity stake in CI Tech. CI Tech is a leading provider of smart commercial information technology products and industry solutions in the PRC. Its business includes provision of one-stop services covering software, content, integral solutions and intelligent products for public sector and commercial customers. Its eHotel, eWall, eShow and other software system solutions are widely adopted in different scenarios, such as hotels, hospitals, schools, shopping malls, airports, cafes, security, cinemas, etc. The acquisition is expected to provide the Group with an additional stream of revenue from software and services and to facilitate the Group to enter into the B2B industry rapidly, which is of promising growth potential. (I do not hold the above stock)

Strategy:

Buy-in Price: $3.90, Target Price: $4.30, Cut Loss Price: $3.70

|

|

HOPERUN SO(300339)

Analysis:

HopeRun Technology Corporation (HRTC) is a solution provider specializing in telematics and device to device communications. Its white label services include mobile technologies/solutions, embedded systems, web technologies, M2M solutions and Telematics applications. The company recently announced that it has signed a business cooperation agreement with Ant Financial and the two parties will cooperate in upgrading the system architecture of the financial industry. We believe that it will help accelerate the company's financial cloud market layout and have huge growth room in the future.

Strategy:

Buy-in Price: RMB13.30, Target Price: RMB16.30, Cut Loss Price: RMB11.50

|

| |

|

Kangmei Pharma (600518.SH) - TCM Decoction Pieces Benefiting From Omni-Chanel

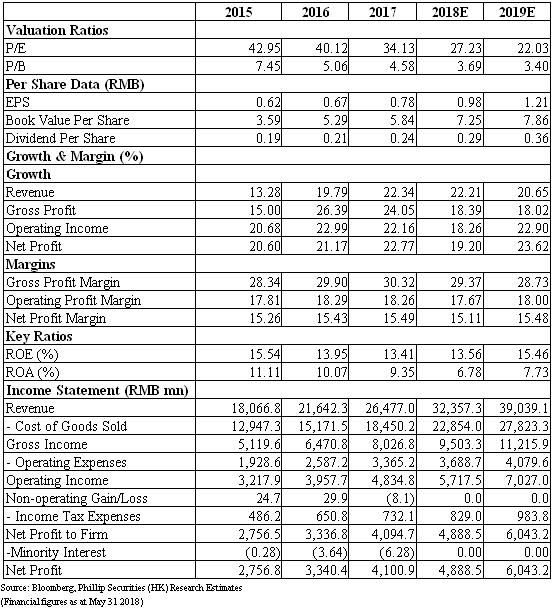

Investment SummaryThe company realized revenue 22%/28% YoY growth in FY17/18Q1, slightly beyond our expectation. We see TCM decoction pieces benefiting from omni-channel advantage, while medicine and medical instrument distribution business grow dramatically. We are positive on Kangmei's integrated healthcare industry chain which is of great synergies and expected to consolidate its leading position. Given 18E/19E EPS estimation of RMB0.98/1.21 and target PE of 31x (roughly par to market consensus 26.69x + 15% premium), we increase target price to RMB30.5. (Closing price at 31 May 2018) Business OverviewFinancial updates. In FY17/18Q1, the company achieved revenue of RMB2.5bn/9.1bn (+22.3%/27.7% YoY) beyond our expectation, and NP attributable to shareholders of RMB4.1bn/1.4bn (+22.8%/33.3% YoY). In terms of profit margin, GPM was up by 0.4pp, more specifically, GPM of TCM decoction pieces up by 1.37pp, self-produced medicine up by 3.32pp and medical instrument up by 5.8pp. By region, East China is still main market taking up 57% in topline and growing by 20% last year, while sales in North China and Southwest China also developed quickly with sales up by 55%/21% YoY. TCM decoction pieces benefiting from omni-channel advantage. In 2017, TCM decoction pieces business generated revenue over RMB6.16bn with over 30.93% YoY growth. We highlight that favorable policies for TCM decoction pieces (maintaining 15% mark-up) will facilitate this industry's continued growth. Kangmei has set up factories in in 11 cities (including Guangdong, Beijing, Jilin, Sichuan, Anhui, etc.) which produce over 1,000 types of TCM products and 20,000 formulas. As a leading company in this industry, Kangmei is going to boost this business leveraging on its strong distribution network, involving medical institutions, pharmacy trusteeship, smart pharmacy, OTC retail, pharma store chain, e-commerce platform, mobile healthcare app, and so on. We see that omni-channel advantage has formed to help digest newly-added capacity, enlarge business scale and take more market shares. Medicine transaction and medical instrument business to speed up. Medicine transaction business generated income of RMB9.6bn rising by 31.44% YoY and medical instrument contributed to RMB1.99bn with 117.88% YoY growth. These two businesses mainly target hospitals and chain pharma stores. Resulting from powerful control over entire TCM value chain (from upstream to downstream), the company's business model helps to increase GPM of these two businesses. The company develops medical instrument business through self-construction and M&A and mainly focuses on consumptive materials and apparatus of orthopedics field. Its agency service has covered 90% Chinese districts, with proxy for Zimmer-Biomet, Smith&Nephew, etc. It will actively enhance integration of medical instrument value chain and strive for more agency rights of competitive products. Bright outlook of healthcare value chain. The company has cultivated an integrated TCM value chain with rich medical resources and great synergies. For upstream, the company effectively manages the supply of Chinese medicine materials (CMM) leveraging on well grasping terminal information. For mid-stream, Kangmei builds `康美e藥穀` as the online transaction platform of CMM and launches CMM price index as well as establishes distribution center in Beijing, Northeast China, Shanghai involving 30 regions. For downstream, its distribution network (involving medical institutions, pharmacy trusteeship, e-commerce platform, etc.) together with managed hospitals (Kangmai Hospital, Meihekou Center Hospital, Kaiyuan City Center Hospital, etc.) and launch of mart pharmacy projects will enrich medical services provided and further supplement its value chain. Investment Thesis, Valuation & RiskOur valuation model gives target price of RMB30.5, based on assumption that revenue growth rate will be 22%/20.65% in 18E/19E. We estimate NP to be RMB4.89bn/6bn in 18E/19E, and EPS of RMB0.98/1.21. Given target PE 31x (roughly par to market consensus 26.69x + 15% premium), our TP is RMB30.5. Downside risks: 1) Management inefficiency; 2) Business growth fail expectation; 3) Policy risks.

Financials

Click Here for PDF format...

| Recommendation on 5-6-2018 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 26.760 | | Suggested purchase price | N/A | | Target Price | $ 30.500 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|