Investment Summary

The traditional ERP and cloud business are developing well in 2017. As China's future IT spending increases and the SaaS market continues to grow, we expect the businesses to maintain growth in the future. We predict the growth rate of total revenue to be 21.9%/22.2% in 2018/19F. The management also expects that the cloud business will be out of red in 2019, and will replace the traditional ERP as the main business in 2021. With our target price $8.94 derived by the sum of the parts valuation, we believe the stock is slightly overvalued, though its fundamentals are satisfactory. With 2.72% downside, we initiate “Neutral” recommendation. (Closing price at 5 June 2018)

Performance review

The financial performance of the company was remarkable in 2017, and will focus on its development on cloud services. The revenue rose by 23.7% YoY; the net profit increased by 80.8% YoY to RMB 378 million; and the operating cash flow also increased by 34.6% to RMB 824 million. The growth of revenue for cloud services remained strong, with a rise of 66.7% YoY, to RMB 568 million. However, the net loss rose to RMB 113 million, and the company expected to record a net loss until 2019. The R&D cost increased to RMB 345 million, while the proportion to revenue slightly decreased by 0.3%.

Business Overview

Founded in 1993, the company was mainly developing financial software. In 1998, it started to develop Enterprise Resource Planning software (ERP). Since 2012, it started to develop its cloud services, cloudifying its traditional ERP. Currently, the company is developing, manufacturing and selling of enterprise management software products, SaaS cloud products and provision of software-related technical services.

Cloud Services

The main products for cloud services are Kingdee Cloud ERP, Jingdou Cloud, and Guanyi Cloud.

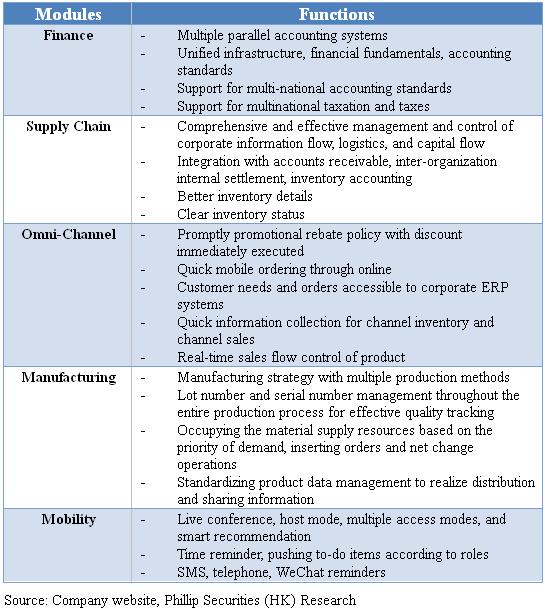

Kingdee Cloud ERP is targeting large and medium-sized companies with substantial growth. It consists of five modules, i.e. Finance, Supply Chain, Omni-Channel, Manufacturing and Mobility. It is expected there will be more modules to be launched, such as Human resource, Customer relationship, and etc. Its main clients are Tencent, Huawai, CocaCola, OfO, and etc.

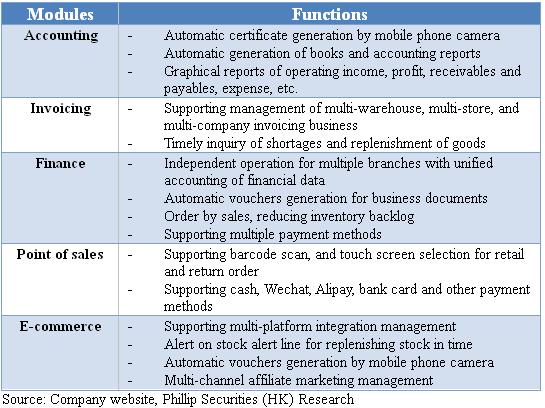

Jingdou Cloud is providing cloud services, such as Accounting, Invoicing, Finance, Point of sales, and E-commerce for Micro Businesses.

Guan Yiyun is mainly for e-commerce customers, providing automated order management, procurement and inventory management, accounting management and statistical reports, as well as B2C mall system, B2B independent mall and BBC platform mall.

Cloud ERP preferable to traditional ERP for SME

Less initial expenditure

For traditional ERP, the customers required to pay a one-off licensed fee for the software, database, servers, as well as maintenance fee every year. However, the business model for cloud ERP is user subscription. The customers only pay a service fee every year for the software, reducing the initial expenditure substantially. Thus, the cloud ERP is preferable to traditional ERP for SME.

Lower maintenance cost

Whenever there are version switching or special requests, on-site consultant is needed for traditional ERP, leading to a higher cost. But, it can be done online for cloud ERP, which costs less for SME.

Robust growth in cloud services still in place

Strong growth in SaaS market

According to the estimation by IDC, the SaaS market in China will reach USD $4.89 billion, a CAGR over 40% from 2017-2021. Since users only need to pay for the service fee, but not for the software, database, and servers, it can reduce the initial expenditure substantially. Besides, it do not require on-site consultant for maintenance and update, reducing average cost by 60-70% in five years. Therefore, we expect the cloud ERP will be the mainstream in the future, boosting the growth in cloud services.

Strong product advantages

Developing cloud products in 2012, the company was early enough than its competitor “Yonyou” in the SaaS market, thereby a stronger competitve advantages for its cloud products. According to “China Semi-annual Public Cloud Services Tracker” released by IDC in 2017, Kingdee ranked 1st in the overall SaaS market in the first half of 2017 with 7% market share, and continued to lead in SaaS ERP with a market share of 18.25%. In addition, the number of paying users rose rapidly, with a high renewal rate 70-90%. Meanwhile, having well-known customers such as Anta, OfO, Huawei, and China Merchants Group, it shows the cloud products are highly accepted by customers.

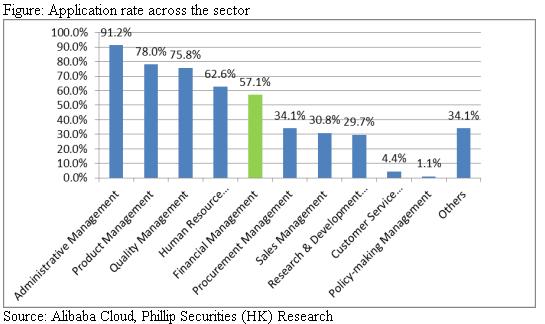

Unsaturated SaaS Market

According to “China SaaS Users research report in 2017” released by Alibaba Cloud, among the respondent companies, the SaaS application rate for financial management, procurement management, sales management, etc. was still below 60%, implying some SaaS subsectors still have a lot of room to grow. Based on IDC, the market share of company's Finance SaaS products was 46% in 20171H, ranked 1st. As the company started its businesses by developing finance management software, we believe the company will remain its leading position in this submarket, fueling the growth of cloud services.

Customers mix for Kingdee Cloud ERP

Due to the overlap of cloud ERP and traditional ERP in regard to some functions, there is concern that the cloud ERP may take away the traditional ERP existing customers. However, based on the company information, 74% of the existing customers for Kingdee Cloud ERP are new, where 58% are new customers who are non-previous ERP users. Besides, only 26% are previous Kingdee customers for traditional ERP, showing that the demand for cloud ERP is not simply an upgrade from traditional ERP users. Many customers join because of the cost reduction by cloudification, demonstrating that cloud ERP helps attract new customers.

Cloud services is expected to get out of the red

The cloud business usually requires huge customer acquisition cost in the initial stage of development, so the loss will increase with income in the beginning. However, when the business reaches a certain market size and customers are addictive to their products, they can gradually make profits. At present, under the high product renewal rate and market share ahead, we believe that the loss in the cloud business will soon narrow. At the same time, the management of the company stated that it is also confident that the loss will be around RMB 50 million to RMB 1 million in 2018 and get out of red in 2019.

Traditional ERP

The ERP software products of the company are Kingdee EAS, Kingdee K/3 wise and Kingdee KIS.

Kingdee EAS's target customers are large-scale enterprises and assist customers in making business decisions and daily operations management. Enterprise decision-making functions provides strategic target management, strategic performance management, comprehensive budget management and decision support; daily operation management covers value chain, like R&D, procurement, production, inventory, sales, distribution, and other value-added activities, and provides financial, human resources, collaborative office, etc. Business innovation platform helps companies quickly respond to customer needs and enhances business efficiency.

Kingdee K/3 wise target customers are medium-sized enterprises, and provide financial management systems to corporate financial accounting and management personnel to achieve overall financial consolidation, comprehensive budgeting, capital management, and financial reporting, and help transform financial management of the enterprises from accounting to management Decision-making changes. Each module of the financial management system can be used independently and can be seamlessly integrated with the business system. There are eight major module subsystems: financial management, supply chain management, manufacturing management, sales and distribution management, office automation, customer relationship management, human resources management, and business intelligence.

The target customers of Kingdee KIS are mainly small and micro enterprises. It builds a customer-centered capability for customers to manage their business efficiently, and have a clear grasp of core assets such as inventory and capital. Kingdee KIS is divided into different products, such as: Finance Series, Business Series, Professional Series and Kingdee KIS flagship series. Enterprises can only purchase their own needs and services, greatly reducing expenditures.

Traditional ERP business will maintain steady growth

Optimistic in economy of China, driving future IT spending

The correlation between ERP software sales volume and economy is very high. The reason is that when the economic downturn occurs, the company tends to reduce unnecessary expenditures such as IT as much as possible, thus reducing the demand for ERP software. During the period 2012-2015, due to the uncertain economy of China, the company continued to record negative growth in its traditional ERP business. It did not regain positive growth until 2016. At present, most companies are optimistic about the economy of China and are therefore willing to invest more in IT spending. According to consulting firm Gartner, China's software spending in 2018 will increase by approximately 12.5% to RMB 70 billion, and will reach RMB 80 billion in 2019. If the economy of China is going well, we believe it will continue to drive future IT spending, so that traditional ERP software can maintain stable growth.

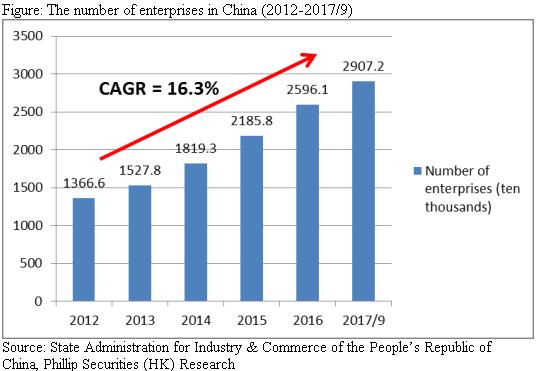

The number of domestic companies continues to grow, stimulating demand for ERP software

Since the main income for traditional ERP software is one-time, it is very important to attract new enterprise customers to increase the revenue of traditional ERP software. In recent years, the number of Chinese companies has continued to grow, recording a CAGR of 16.3%, and has brought many potential customers to the traditional ERP business. We believe that the number of Chinese companies will continue to grow in the future, and the traditional ERP software business will maintain steady growth.

Earnings forecast

Revenue

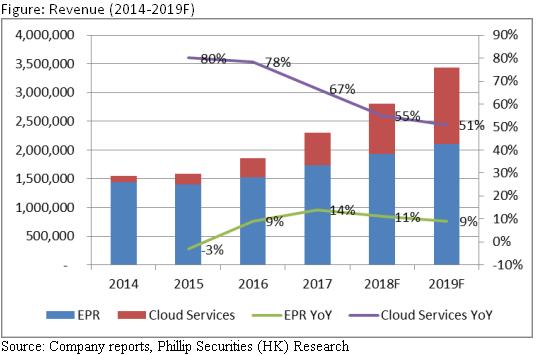

The company will focus on the development of cloud business in the future. We expect the revenue growth of cloud business in 2018/19 to be 55%/51% to RMB 880 million/1.33 billion, due to 1) Strong growth in SaaS market, 2) Strong product advantages, and 3) Unsaturated SaaS market. If the cloud business maintains its momentum, it is expected to exceed the traditional ERP business for the first time in 2021.

Thanks to the improvement of the economy of China and the rising number of companies, we expect the company's traditional ERP business will grow steadily. It is expected that the revenue growth in 2018/19 will be 11%/9% to RMB 1.93 billion/2.1 billion. Lest the rapid development of cloud-based services may replace traditional ERP to some extent, because SME tends to adopt the cloud services on cost considerations, we have made a conservative forecast for traditional ERP business growth.

Gross profit margin

The company adjusted its sales channel in 2012, increased its distribution investment, and converted Kingdee K/3 from direct to indirect sales in 2013, which increased gross profit margin. Until 2014, the gross profit margins have stabilized, and we do not expect major changes in 2018/19 and remain at 81.5%.

Sales, administrative and research and development expenses

The company's sales, administrative, and R&D expenses have been relatively stable with revenue in the past. In 2017, they were 53.7%, 13.9%, and 15%, respectively. As the company is making great efforts to develop cloud services, the sales expense rate has been high. In addition, the sum of the three expenses from 2014 to 2017 is 78.2%, 76.8%, 84% and 82.5%. We expect the R&D expense ratio to slightly decline in 2018/19, 53.5%/53% and 15%/14.5%, respectively, to reflect the assumption that the clould business starts to be profitable in 2019. The administrative expense ratio decreased slightly at 2018/19, which was 13.6%/13%.

Net profit

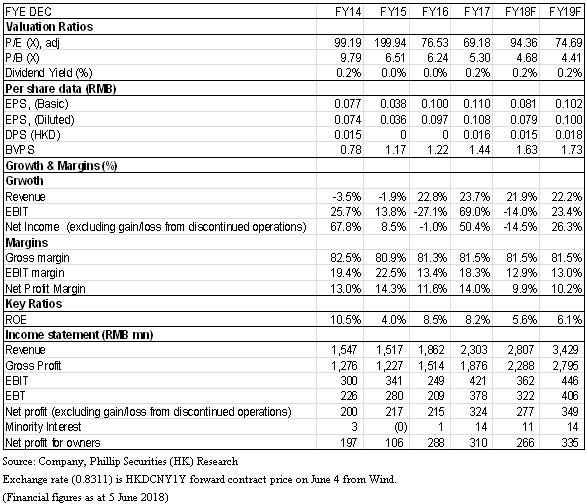

After the drop of net profit in 2015, it regained its growth momentum. The 2016/17 revenue growth was 172.5%/7.6%, reaching RMB 290 million/310 million. However, we forecast that the net profit will record a decline in 14.3% in 2018, due to the non-recurring gains of the revaluation of investment property of RMB 96 million in 2017, which made the net profit of that year overstated. In addition, we expect the net profit will record a 26.3% growth in 2019 based on the assumption that the cloud business will record net profit for the first time in 2019.

Valuation

We adopted sum of the parts valuation by dividing the business into three parts: 1) Traditional ERP business (P/E), 2) Cloud business (P/S), and 3) Investment real estate business (book valuation). We forecast the earnings per share of the traditional ERP business in 2018 to be RMB 0.096 with target PE ratio 28x (similar to the adjusted historical average in 2008-2012); the revenue of cloud services per share in 2018 would be RMB 0.268 with target PS ratio 13x; for the investment real estate business, the book valuation is used, and the valuation per share is RMB 0.52. Finally, a net cash is RMB 0.58 per share at the end of 2017 (taking the completion of convertible bond into account), plus available-for-sale financial assets per share RMB 0.14. A target price of HK$8.94 was obtained and we initiate “Neutral” recommendation. (HKD/RMB: 0.8311)

* As the market does not have a single company conducting traditional ERP business as a reference, we have chosen to use the historical PE ratio from 2008 to 2012 (we have adjusted the income from investment in real estate business), because traditional ERP was the main business at that time.

Risk

1. Slower-than-expected growth in SaaS market

2. The economy of China slows down

3. Cloud ERP may take away the existing customers of traditional ERP, particularly SME

Financials

Click Here for PDF format...