Investment Summary

SUNeVision is one of the leading carrier-neutral data center operators in Hong Kong, owned 74.04% by Sun Hung Kai Properties (16.HK). We expect to see there will be a rising demand for data center from the proliferation of Global IP traffic and cloud services, and the group has competitive advantages on both quality and capacity for its data centers. We predict the earnings growth (excluding gain on fair value) to be 16.2%/7.9% in 2018/19F, assuming PE 36x (Average forward PE plus a standard deviation). With 24.9% upside, we initiate “Buy” recommendation. (Closing price at 19 Jun 2018)

Company Background

The group mainly engaged in the provision of data center in Hong Kong. Besides, it also engages in the installation and maintenance of its satellite distribution network, fibre-optic cable, networking and security surveillance systems, and provides professional design-and-build consultancy service for wireless and broadband network projects.

Business Overview

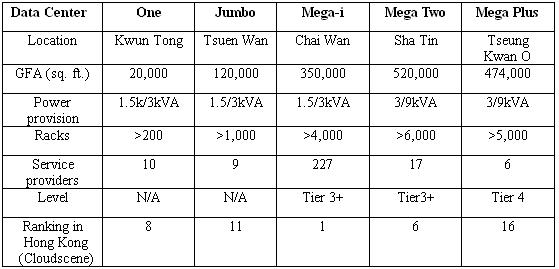

The group is now operating 5 data centers in Kwun Tong, Tsuen Wan, Chai Wan, Sha Tin and Tseung Kwan O. In a total GFA of 1,484,000 sq. ft., it offers more than 16,200 racks with power provision ranging from 1.5 kVA (Standard power zone) to 9 kVA (High power zone). Mega-i and Mega Two have reached to standards for Tier 3+ data center, while Mega Plus even to Tier 4. According to Cloudscene, Mega-i ranked 1st out of 101 data centers in Hong Kong, where the ranking is depending on the number of service providers the data centers have. And, the other data centers for the group were also ranked top 20% in Hong Kong.

Industry Overview

High customer stickiness

The business of data center inherently has very high stickiness to customers. In fear of the operation disruption, the clients usually have a very high the switching cost, so they will prefer to stick with a satisfactory data center operator for a long period. It encourages data center operators to offer discount to customers in the beginning in order to attract potential customers, so the rent for new data center needs a few years to be normalized.

Recurring income

A data center operator is literally a property landlord. By leasing area and providing electricity and maintenance to customers` servers, data center receives rental income from customers. Besides, the lease period is usually ranging 1 to 5 years, or even longer, creating a stable recurring income for the operators. As a result, we believe the historical earnings will be a good reference due to its high earnings quality.

Capital- intensive business

Data center is a capital-intensive business, especially in Hong Kong. The costs of building a data center are mainly from 1) land or properties and 2) equipment, e.g. racks or electronic devices. In Hong Kong, the capital expenditure is usually very high for operators because it is costly to acquire suitable land and property. However, it also creates an entry barrier for them, as new entrants require substantial initial investments.

Limited supply for new top tier data center in short term, yet alleviated in the medium term

In Hong Kong, it is never easy to acquire a suitable land and property for building a top tier data center, yet government has been showing supports in land supply, which will manifest in the medium term. The main source of land and properties for a top tier data center are 1) industrial estate under Hong Kong Science and Technology Parks Corporation (HKSTPC), 2) revitalized industrial building, and 3) land offered in the open market.

Regarding industrial estate, in 2016, HKSTPC claimed they will not rent out any site for a single leasee to build up their own property, because the leasee is usually not encouraged to reach the maximum plot ratios of the site, reducing its space utilization. Thus, HKSTPC planned to build their own property and rent it out. This decision has casted a shadow on the data center industry, as many players are seeking land for their next data center in Tseung Kwan O industrial estate, which is the current data center hub in Hong Kong. The decision will wipe out one of the main sources of land for the data center.

Regarding revitalized industrial building, it is not always suitable for them to convert into a top tier data center, because the electricity supply and the construction of the property could be one of the obstacles for building a top data center. In 2015/16, there were 14 applications on using Industrial Buildings or Industrial Lots for Data Centre Development, yet dropped to 1 in 2016/17, and only 2 as of 2017/11.

Hence, we expect the main source for top tier data center will mainly from the land in the open market. The government is going to launch land bidding for two sites specified for data center in Tseung Kwan O in the second half of 2018, around 1,000,000 GFA sq. ft. in total. It is expected to build two top tier data center and will take at least four years to complete. As a result, the supply for new top tier data center is limited in short term, but will alleviate in the medium term.

Industry dynamics

According to Frost & Sullivan, it is expected the revenue from data center market in Asia-Pacific will grow in a CAGR 14.7% from 2015-2022, thanks to the explosive digital needs from the emerging economies such as China, India, and Indonesia. Besides, more and more customers will prefer managed hosting service (server rental with other specified equipment) to colocation service (pure space rental, such as space, cages or racks), because it can reduce their IT infrastructure costs. As a result, it is expected the growth rate of managed hosting service will be higher than colocation service, leading to a larger proportion of managed hosting service in the next few years, while colocation service will still be dominated for few more years.

Long term growth drivers

The demand for data center remains strong

1. The proliferation of Global IP traffic

As the world are entering a digital era, along with prevailing electronic devices, the Global IP traffic has been soaring, and it is expected there will be a 24% CAGR from 2016-2021F, according to Cisco. Asia Pacific is believed to be the second-fastest among the regions, with 26% CAGR from 2016-2021F, just behind Middle East and Africa.

Regarding Consumer IP Traffic, the main demand is from internet video, accounting for 75% in 2017. Meanwhile, the fastest growing segment is online gaming, with a 62% CAGR from 2016-2021F based on the estimate from Cisco.

Since we believe the reliance on internet will be more and more significant in the future, the IP traffic will remains its momentum, boosting the demand for data center.

2. Cloud services are becoming popular

Instead of having a colocation or managed hosting services, there are some cloud services providers e.g. Amazon Web Services (AWS), Microsoft Azure, or Google, offering virtualized computing resources over the internet, such as server, storage or processing. And, the cloud services are becoming popular, especially for SME, because those companies can enjoy a lower cost by adopting their services than hosting their own server. Though the prevalence of cloud services may jeopardize the traditional colocation business, it also creates new demand for data center. We expect those cloud services providers prefer to lease facilities from local operators rather than set up their own data center in Hong Kong due to the skyrocketed land cost.

Abundant capacity for upcoming demand

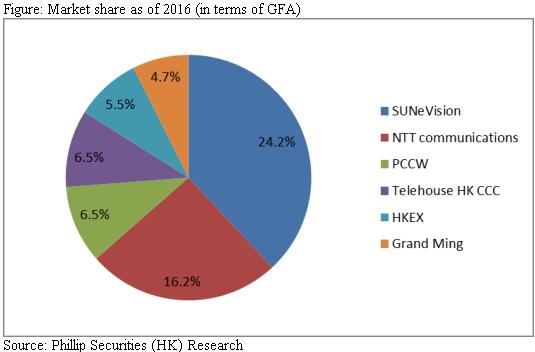

After the completion of Mega Plus and the expansion of Mega Two, the total gross floor area (GFA) doubled from 750,000 to 1,484,000 sq. ft. Moreover, companies has bought a piece of land in Tsuen Wan for HK$ 725 million in 2018 Jan, which could offer at least 201,700 sq. ft. According to a report from an independent third-party in 2016, the market share of the group in terms of GFA before the expansion is 13.9%, ranked 2nd, behind NTT communications, whereas the market share rises to 24.2% after the expansion, becoming the first in the industry. With abundant capacity, we believe the group will be able to enjoy the upcoming demand in the next few years.

Competitive advantages against peers

1. Carrier-neutral data center with numerous service providers

The group is one of the carrier-neutral data center operators in Hong Kong. The advantage of being a carrier-neutral data center is that it will not be tied to any one service provider (telecommunications, ISP, or other), thus providing diversity and flexibility for customers. Not only are the customers able to enjoy an attractive offer from service providers thanks to the competition, but they also enjoy better flexibility on choosing service providers, because they do not need to move their equipments to an new data center.

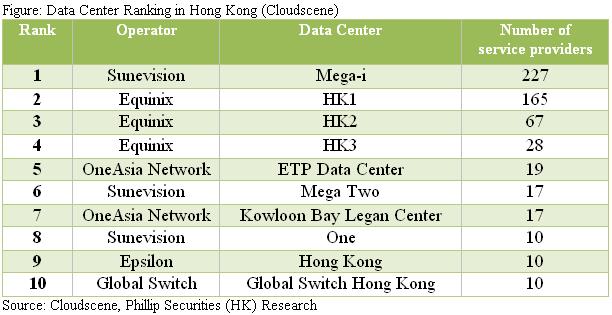

According to Cloudscene, the number of service providers in Mega-i is 227, the most in Hong Kong, and the runner-up is HK1 operated by Equinix, with only 165 providers. The abundant service providers in Mega-i will create significant competitive edge, differentiating their data center from others, because we believe the customers will depend on the aforementioned factor to select its operators.

1. Sustainable competitive edge

We expect the competitive edge is going to sustain, since it is costly for carriers to enter a data center (they needs to install fibers, connecting their infrastructure to the data center they would like to enter). Thus, service providers will be prudent for entering a data center in fear of the business not able to cover its construction cost. Under those circumstances, big data centers are able to persuade service providers by ensuring them enough businesses, eventually inviting more and more customers as well as service providers to enter. It creates a virtuous circle for protecting their lead.

Making good use of the strong connectivity in Mega-i, the group has connected Mega Two and Mega Plus with Mega-i by high-performance dedicated fibers. After the connection with Mega-i, many major international and local carriers will be available on Mega Two and Plus. The three MEGA facilities are strategically located to meet different business requirements and. We believe Mega Campus can expand the competitive advantage to group's other data centers, creating a solider leading position in the industry.

Support from parent company

Currently, Only Mega Two, located in the Sun Hung Kai Logistics Centre, is leased from its parent company Sun Hung Kai Properties (16.HK). Thanks to its parent company, a giant player for property market in Hong Kong, the group is able to reach out many high-quality properties. And, it is more likely for them to renew its lease term in the future. Therefore, we expect to see more sites for data centers are leased from parent company in the future, just like Mega Two.

Earnings forecast

Revenue

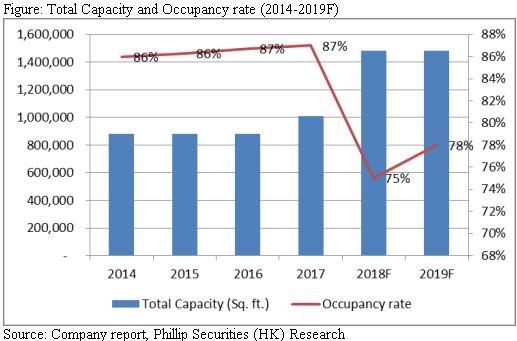

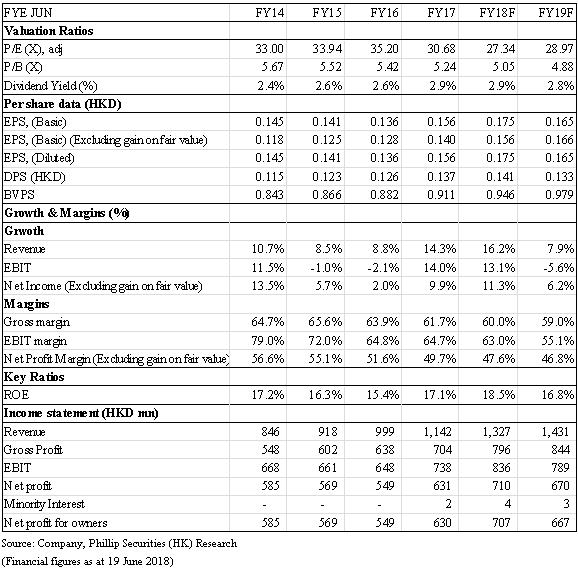

We project the Occupancy rate will drop to 75% in 2018F and rebound to 78% a year later, because of the additional capacity from Mega Plus. Attracting new customers to Mega Plus by offering discounts, we believe the average rent per sq. ft. in 2018F will decrease by 5%, but will be normalized in 2019F, with 2% rise. And, we expect the revenue growth to be 16.2%/7.9% in 2018/19F.

Gross profit margin

Due to additional rental expenses for new data center, the gross profit margin has been deteriorated since 2015, we expect the trend will continue, with 60%/59% in 2018/19F.

Net profit margin

Due to the drop in gross profit margin, we predict the net profit margin excluding gain on fair value 47.6%/46.8% in 2018/19F.

Valuation

A “Paradigm shift” since the beginning of 2017?

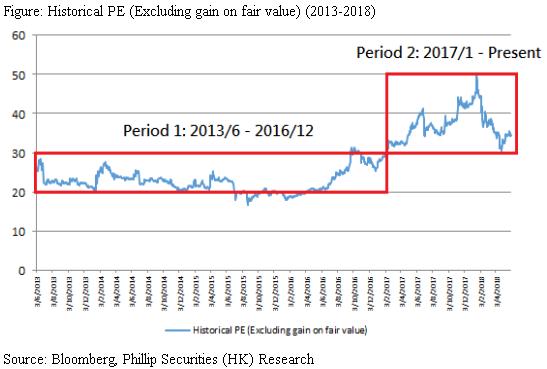

Before 2017 (Period 1), the historical PE (Excluding gain on fair value) was between 20x to 30x, yet the range shifted upward since then (Period 2), ranging from 30x to 50x. What makes the historical PE range upward shift? Was it a temporary phenomenon due to the market sentiment since 2017? We tend to believe it is a paradigm shift instead of a temporary phenomenon, because of two reasons; 1) a debt-oriented development model since the mid of 2016 and 2) transfer of listing from GEM to Main Board.

1. A debt-oriented development model since the mid of 2016

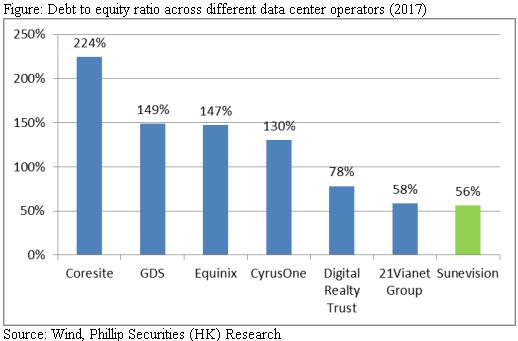

Before 2016, the group usually funded their new projects by retained earnings. However, it changed in the mid of 2016, where group started borrowing loan to fund its projects, with 56% debt to equity ratio as of the end of 2017. In fact, many data center operators in US or China funded their projects by debt, as the cash flow of a data center is usually stable, making their financial condition less vulnerable to the debt burden. We believe a moderate financial leverage will be able to add value by increasing the return on equity and creating tax shield for the group, justifying the new valuation range.

2. Transfer of listing from GEM to Main Board

Transferring from GEM to Main Board can attract new institutional investors, who are prohibited to stocks on GEM. In addition to new investors, the group is now eligible for more institutional analysts to cover, as analysts tend not to cover stocks in GEM. With more analysts to cover, we believe the market will realize the investment value of the company, helping it stay in the new valuation range.

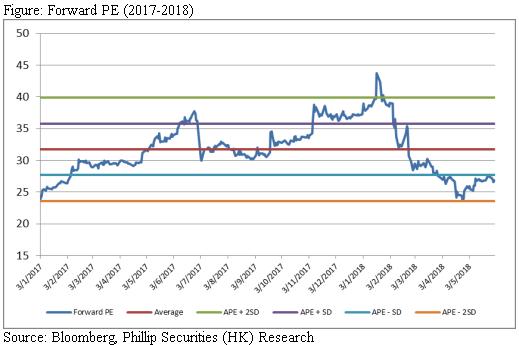

Owing to the rising demand on data center from the proliferation of Global IP traffic and cloud services as well as its competitive advantages against peers, we give a target price of HK $5.97, assuming 2019F PE 36x (Average forward PE plus a standard deviation). With 24.9% upside, we initiate “Buy” recommendation.

Risk

1. Slower than expected demand on data center

2. Significant increase in land supply for data centers within a short period

3. The entry of cloud service giant players to data center industry in Hong Kong

Financials

Click Here for PDF format...