Investment Summary

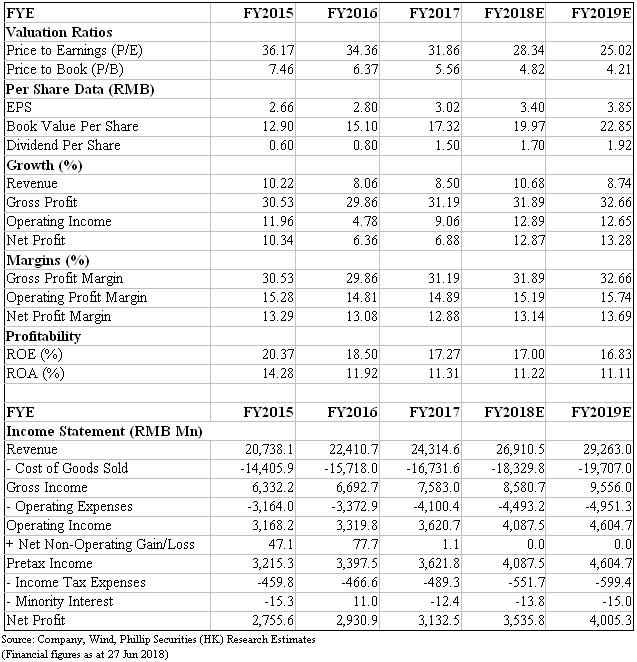

We highlight that recent market volatility brings accumulating opportunity. We restate that company fundamentals remain strong given improving salesman efficiency and solid 18Q1 results (revenue up by 7.26% YoY, NP up by 11.18% YoY and CFO up by 137.75%). We also suggest to pay attention to company's further exploration in hospital field. We maintain 18E EPS target of RMB3.4, and given 33x target PE, we give target price RMB112. (Closing price at 27 Jun 2018)

Business Overview

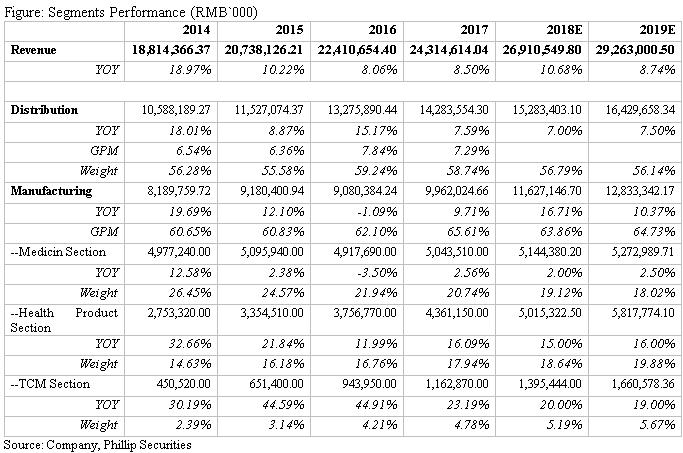

Larger gets larger. The report on drug circulation industry in 2017 issued by the Ministry of Commerce of China showed that the growth rate of pharmaceutical wholesale enterprises was slowing down, given Top 100 pharmaceutical wholesale enterprises report sales up by 8.4% YoY (dropped by 5.6 ppts compared to 2016 growth). The company reported wholesale business revenue of RMB14.5bn, ranking sixteenth among the Top 100, is a regional circulation enterprises. In future, the regional leaders are likely to accelerate expansion through more cross region M&A to increase industry concentration.

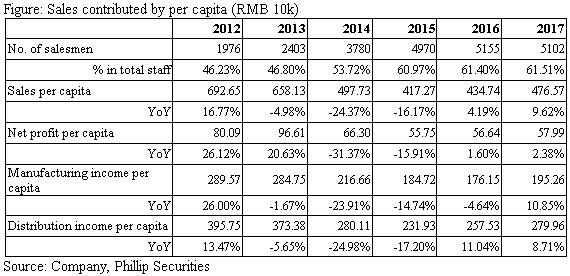

Salesman efficiency may continue to improve after the composite ownership reform. Salesman efficiency decreased during 2010 to 2016. In 2017, Yunnan Baiyao Holdings Limited (YBH) introduced New Huadu and Jiangsu Yuyue as strategic investors to diversify holding structure. We already see improving salesman efficiency in 2017, given revenue per capita was up by 9.62% YoY (2016 +4.19%) and net profit per capita up by 2.38% YoY (2016 +1.6%). We expect the company continue to improve operation efficiency.

Potential progresses of hospital business. Investor meeting summary on its website shows that the company may benefit from provincial government's favorable policies, as the government aims to build Yunnan as a healthcare center featured healthy lifestyle. The company, as a regional pharmaceutical leader, may try to cooperate with tertiary institutions and explore orthopaedics field leveraging on Baiyao's brand advantage.

Investment Thesis, Valuation & Risk

Our model indicates a target price of RMB112.0. We estimate 2018E EPS to be RMB3.4 per share and with target PE 33x, we give 2018E Target price of RMB112.0. Risks include: Rising selling fees; Effects from Two-invoice system; Fierce competition in health product industry; Composite ownership reform fail expectation.

Financials

Click Here for PDF format...