Investment Summary

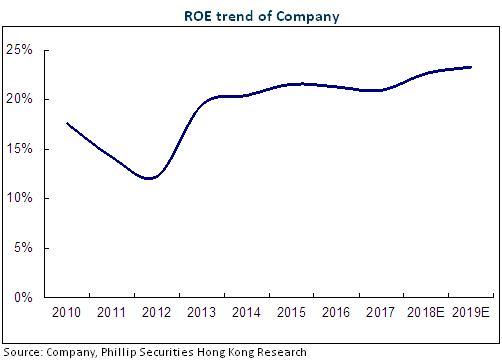

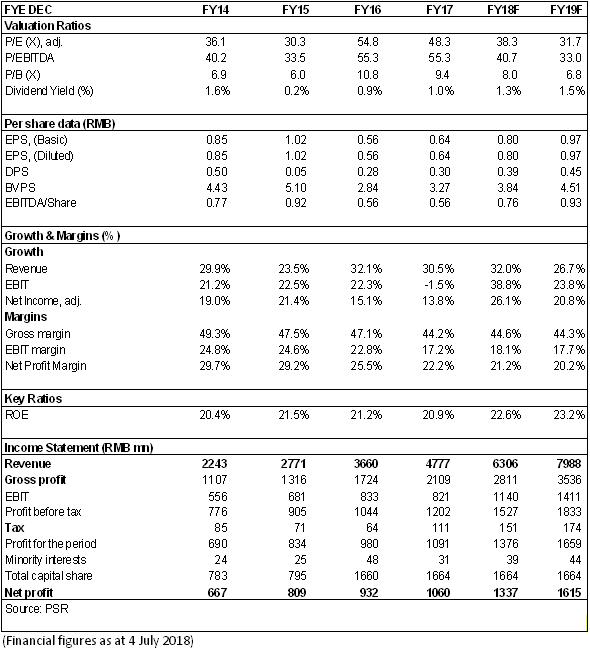

The fluctuation of NEV bus sector affected the Company's 2017 result, But we expect that in 2018, the trend of high growth in China's industrial control industry will continue and the Company's industrial automation services are expected to continue growing rapidly. Meanwhile, the rail transit business will enter a cashing period. As for valuation, we expected diluted EPS of the Company to RMB 0.80 and 0.97 of 2018/2019. And we accordingly gave the target price to RMB32.55, respectively 40.5/33.5x P/E for 2018/2019. "Accumulate" rating. (Closing price as at 4 July 2018)

With a Rapid Growth of Revenue, a Good Situation of Steady Improvement of Net Profits Ongoing

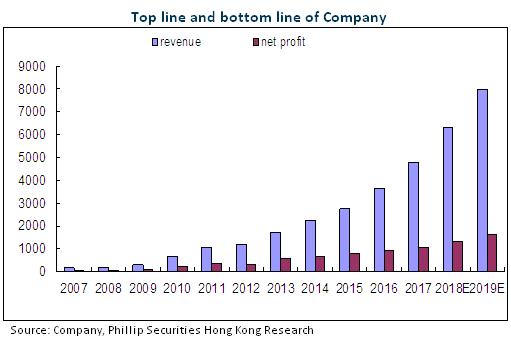

Inovance Technology, with a revenue of RMB4.777 billion in 2017, up 30.5% yoy, with net profits attributable to shareholders up 13.8% yoy to RMB1.06 billion, with EPS RMB0.64 reported, has a result slightly less than our expectation, mainly due to a higher degree of impact on the market of new energy buses by policy adjustment than expectation; the integrated gross margin is 45.12%, down 3 ppts yoy, mainly attributable to such reasons as change in business structure, intensified market competition and rise in prices for part of raw materials. Period cost rate rises 2.3 ppts, mainly due to enhancing the R&D construction for new business.

In the first quarter of 2018, the Company's revenue has risen by 24.7% yoy to RMB975 million, with net interests attributable to shareholders up 13.9% to RMB196.5 million, EPS RMB0.12 reported. In respect of gross margin, the Company, through constantly strengthening R&D of core technology, continues to launch new products with high gross margin rate as well as in-depth solutions to the industry, so as to keep a steady integrated gross margin for products from the Company and make the decrease of gross margin slow down by 1 ppts to 45.54%.

Strong recovery of industrial control services

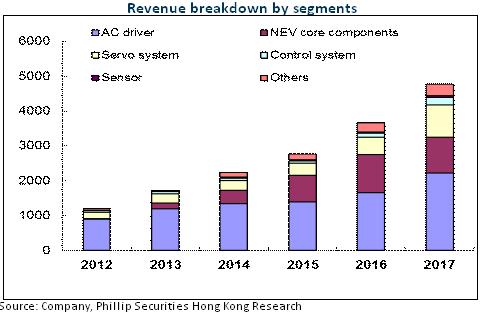

From product structure, the Company has different progress in each business:

Based on data from www.gongkong.com, in 2017, the size of China's industrial automation market increased by 16.5% yoy, in which frequency converter products increased by about 13% yoy, PLC&HMI products by more than 20% yoy, and motion control products by more than 25% yoy. Benefiting from a structural recovery of China's equipment manufacturing and project-based market, the Company's industrial automation services, depending on excellent solutions and brand influence, achieved a market performance of high quality in 2017, with revenues from frequency converter category/servo category/control technology category rising 34%/86%/96% yoy respectively in 2017, their gross margin rates rising -2.7/-0.6/0.95 ppts yoy respectively.

In 2017, global robot industry presented a situation of high-speed development, with a constant expansion of industrial scale and market space, and in Chinese market, industrial robots have sales of 136,000 units, with a yoy growth of 60%. The Company's industrial robot products have achieved bulk sales in mobile phone manufacturing and other industries. In addition, Industrial Robots, Nanjing Inovance (industrial vision), and Shanghai LAIEN (high-precision guide screws) had RMB83 million revenue recorded in total, up 1.84 times yoy.

We expect that in 2018, the trend of high growth in China's industrial control industry will continue. Meanwhile, we argue that the potential of application market for China's industrial robots is gradually entering a stage of rapid release, with the yoy growth rate of industrial robot market able to reach 40%, and the Company's industrial automation services are expected to continue growing rapidly. In 2017, new orders for the Company's intelligent equipment & robots reached RMB4.56 billion, up 43.4% yoy. In the first quarter of 2018, new orders of the Company had an amount of RMB1.158 billion, up 29.7% yoy.

New energy and rail transit services setting out again

The Company's new energy & rail transit services had a revenue in 2017 down 6% yoy, with gross margin descending 8 ppts, mainly due to a subsidy policy adjustment to new energy buses. In 2017, the market of new energy buses in China declined sharply by 14%. Suffering from sales down 7.4% of Yutong Bus, a major customer, the Company's revenue from new energy buses emerge on a decline therefore, but the Company's new energy logistics van services start bulk sales, which offset part of negative effect. We estimate that, with an end of the transitional period of subsidy policy, new energy bus services in Inovance will step out of bottom, while new energy logistics van services will see a burst development.

For the reasons of the construction period and revenue recognition for subway project, in 2017, the Company's rail transit services had a revenue only recognized as RMB100 million, down 56% yoy. At present, the Company has more than 1.3 billion orders for rail transit in hand, and with the delivery of projects and revenue recognition, it is estimated that the Company will have its revenue from rail transit reach about RMB530 million, RMB630 million and RMB700 million respectively in the following three years, which will strongly boost the growth of its result.

Valuation

As analyzed above, we expected diluted EPS of the Company to RMB 0.80 and 0.97 of 2018/2019. And we accordingly gave the target price to RMB32.55, respectively 40.5/33.5x P/E for 2018/2019. "Accumulate" rating.

Financials

Click Here for PDF format...