|

|

|

*Advertisement* |

|

|

|

|

|

10 Jul, 2018 (Tuesday) |

TOWNGAS CHINA(1083)

Analysis:

Towngas China (1083) is principally engaged in gas connection, sales and distribution of piped gas and related products. As at end of 2017, the Group operated 108 projects in city gas as well as vehicle gas refilling stations and midstream projects, selling gas to over 11.77 million customers covered by a gas pipeline network stretching out over 40,000 kilometres. The Group is pursuing the development of integrated energy service operations, distributed energy business in particular. Its wholly-owned integrated energy project investment platform, Towngas China Energy Investment (Shenzhen) Limited, was inaugurated in January 2017. Its goal is to drive the building of natural gas distributed energy stations. (I do not hold the above stock)

Strategy:

Buy-in Price: $7.60, Target Price: $8.30, Cut Loss Price: $7.20

|

|

SH PHARMA(2607)

Analysis:

Market valuation of pharmaceutical distribution business now is reaching a record-low after previous fluctuations. In first half leading distributors finished adjustment of inventory allocation business to comply with TIS, which is expected to start rebounding and regarded as a considerable target to buy now. SPH is a national pharmaceutical market leader. Its manufacturing business is expected to keep quick growth and maintain good profit margin given intensifying introduction of innovative drugs. For distribution segment, the company is progressing integration with Cardinal which will show effective synergies. Besides, SPH e-commerce platform proactively seeks cooperation with more hospitals and explores prescription outflow business, leveraging on its regionally biggest retail pharmacy network and wide hospital coverage.

Strategy:

Buy-in Price: $20.50, Target Price: $25.50, Cut Loss Price: $19.00

|

| |

|

CSPC Pharmaceutical (1093.HK) - Robust sales of innovative drugs

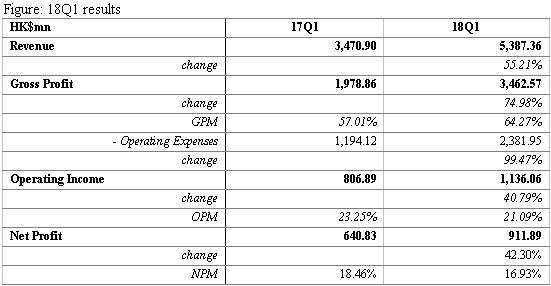

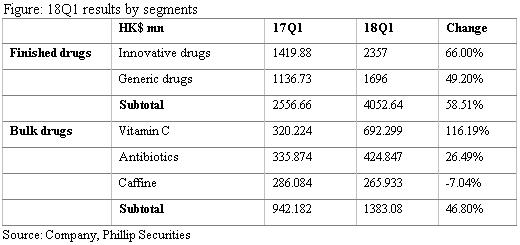

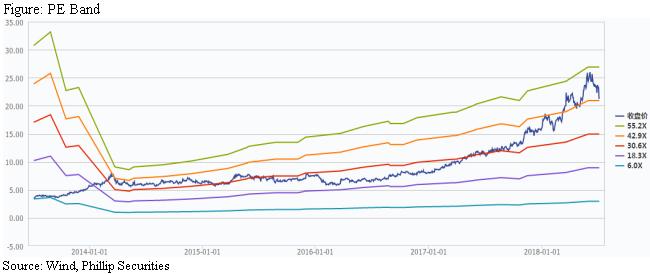

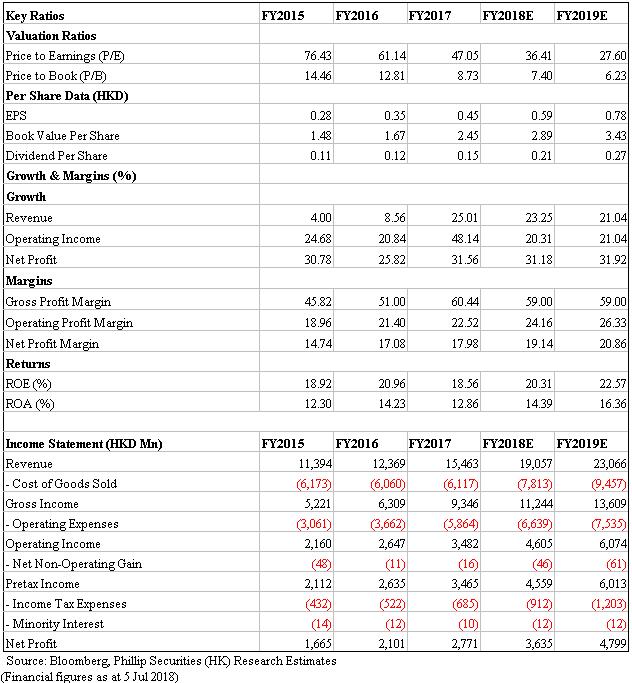

Investment SummaryDuring the last month, the stock price has dropped by ~17%, after which we see Accumulate opportunity. The management maintains annual NP growth guidance of 20-30% intact for future 5 years. We highlight that CSPC as a leading firm among HK listing peers has solid fundamentals and maintain 18E/19E EPS estimation of HKD0.59/0.78 and target price HKD24.8, implying forward PE 36.8x. (Closing price at 5 Jul 2018) Business OverviewSolid 18Q1 results. The company reported 18Q1 topline growth of 55% (HKD5.39bn) and lower operating income growth of 41%. This is due to rising selling expenses and increasing R&D investment, which led operating margin dropped by 2ppts. While net profit maintains proportionated growth of 42%. We expect the company to achieve good results in first half. Finished drugs beat our expectations, given notable YoY growth of 58.5%. Innovative drugs (60% in segment income) recorded 66% growth while common generic drugs reported 49% growth. In future, the company will continue to enlarge sales team of innovative drugs, explore blank markets and strengthen academic promotion. On generic drugs, the company targets continuously stable growth through introducing TCM products and pediatric drugs, to build branded generic drugs.Bulk drugs. VC continues to benefit from relatively high price since last year, given Q1 sales was up by 112% which simultaneously contributed to profitability. Antibiotics reported moderate growth of 24% resulting from recovering price. However caffeine generated less profit attributable to rising costs. Focusing on biotech targets. The company can externally expand through acquiring biotech targets to enrich product mix. Back to the beginning of 2018, CSPC announced acquisition of ~40% interest of a biotech firm. In future, it is expected to seek target firms with relatively mature pipeline of biologic drug products. Valuation Thesis & RisksOur model derive TP of HKD24.8: Given recently intensifying short-term volatility, we highlight Accumulate opportunity for medium-term investment. Robust Q1 results enhance our confidence towards 2018 performance, but concerns of rising selling costs and R&D expenses lead to unchanged 18E/19E EPS estimation of HKD0.59/0.78 and target price of HKD24.8, with target PE 42x. Risks include: rising selling and R&D expenditure; M&A or R&D fail expectations; policy risks.

Financials

Click Here for PDF format...

| Recommendation on 10-7-2018 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 21.400 | | Suggested purchase price | N/A | | Target Price | $ 24.800 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|