Investment Summary

-Regarding the recent trade disputes between China and USA, we expect that the Chinese government will pay more attention to the contribution of domestic demand to overall economic growth. With the increase in per capita income, it will help to boost the fast-moving consumer goods market growth, including the necessities market. As the market leader in paper towels and sanitary napkins industries in China, Hengan is expected to benefit from the trend.

-Facing intensified market competition and rising cost of raw materials (i.e. wood pulp), Hengan responded by launching new high-margin products, and implementing the “small sales team” operation model (also known as “Hengan's Amoeba model”) in late April last year. The improvements of the financial figures like top line and expenses savings have been showed in the second half of last year. The improvements are expected to reflect in the whole year of 2018, to offset part of the impact from rising pulp cost on gross profit margin.

-Through the Amoeba model, the management team can also better understand the market situation, and observes that in addition to sanitary napkins and diapers products, there will be demands for other products. The management team has already repositioned the sanitary napkin business as premium personal hygiene business, and plans to launch new product categories such as cotton pads within this year. It also plans to strengthen the competitiveness of the e-commerce platform. We expect that these measures will help the growth of top line and controlling of expenses.

-Hengan has just announced the acquisition of the Finnpulp Oy, marking the expansion of its business to upstream pulp industry. The market has different views towards this action. We believe that the acquisition of upstream business will help Hengan to strengthen the mid- to long-term cost advantage and reduce the impact of pulp price volatility to gross profit margin. With an estimated total northern bleached softwood sulphate kraft pulp(NBSKP) production of 1.2 million tons, and eventually maximum holding of 49% of the share capital of Finnpulp, Hengan is expected to have approximately 600,000 tons of guaranteed supply from Finnpulp by 2021, which can fully fulfill previous yearly demand of 300,000 tons.

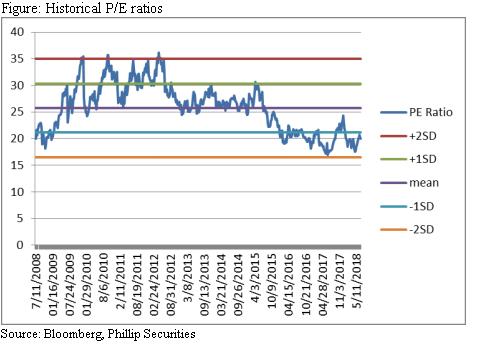

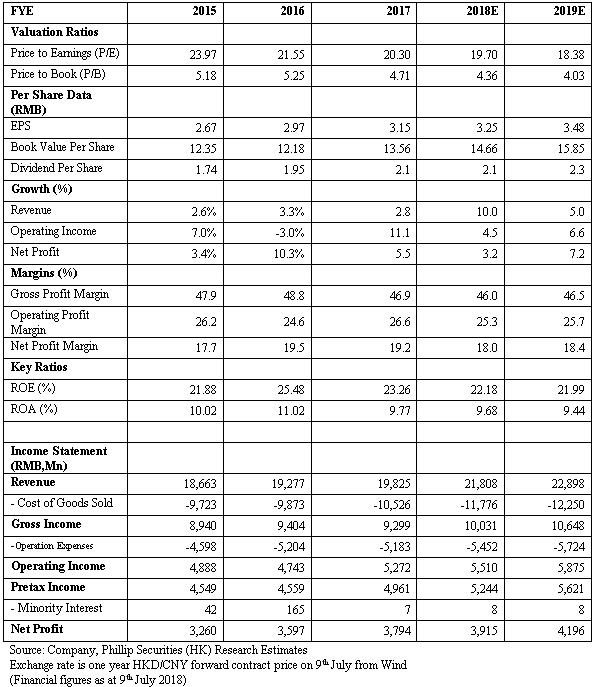

-In the past three years, Hengan's dividend payout ratio was over 60%. The management team intends to maintain the dividend policy. We give Accumulate rating, a forecast price-earnings ratio of 21.1, and thus a target price of HKD80.5. (Closing price as at 9 July 2018)

Business Overview

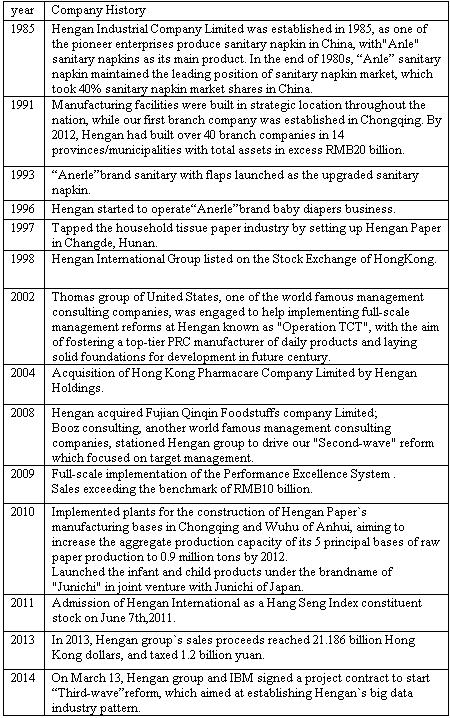

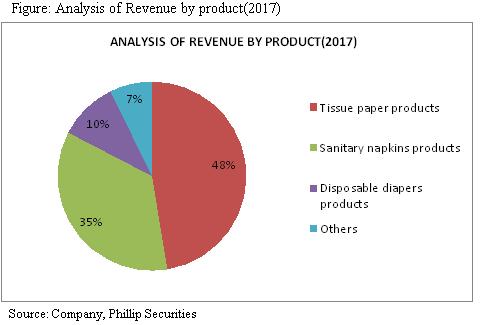

Established in 1985, Hengan is one of China's earliest manufacturers of sanitary napkin products. After years of development, Hengan's business can be roughly divided into four parts. The top three are personal hygiene products, including tissue paper, sanitary napkins and disposable diapers, which account for 47.4%, 35.2% and 10.1% respectively of the total revenue for 2017.

According to the management team, in terms of market share in mainland China in 2017, paper towels business accounted for around 20% , whereas sanitary napkins accounted for 27% to 28%. Hengan is the market leader for both industries. The market share of disposable diapers business accounted for single digit, which is mainly due to the dispersed market nature including foreign brands, but it is still the top leader among its mainland peers.

On March 13 2014, Hengan group and IBM signed a project contract to start “Third-wave”reform, which aimed at establishing Hengan's big data industry pattern.

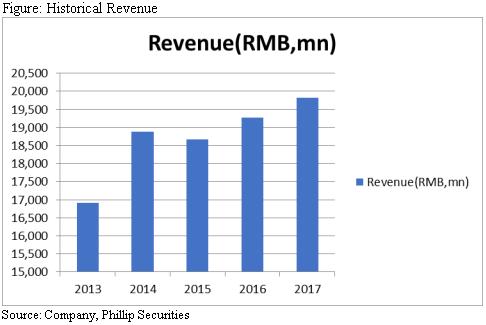

In recent years, Hengan's revenue growths were only single digits. Last year's growth was only 2.8%. The management team has given this year's guidance as double-digit growth. The main driving factor is that the growth of paper towel business is accelerating. Considering the growth trend from the beginning of 2018, it has confidence to achieve the target.

The tissue paper business only increased by 3.6% last year, but it increased by more than 7% in the second half of the year, reflecting the results of amoeba reform, and the improvement of the overall sales channel.

We expect that the benefits from Amoeba model will be fully reflected in 2018, and the small team compliance rate is expected to increase from approximately 20% in 2017 to over 50% for this year. The benefits will be reflected as a result of accelerating growth of top line and reduction of operation expenses. Last year, less than 20% of Amoeba's units reached the sales target and this year we expect the ratio will increase to more than 50%.

Besides, taking into account of the absorption of the releasing demand from industry consolidation, and the improvement of e-commerce channel, we believe that the double-digit growth target can be achieved. Tissue paper business will grow the fastest compared to other two main businesses.

We also expect that the main driver will be the sales volume growth. The overall selling price is expected to remain stable due to the launching of high-margin products. However, we also consider the intense competition in the industry, we expect that there will only be a low double-digit growth.

In terms of operating profit, there will still be new product promotion and branding investment this year. Therefore, it is believed that there is an opportunity to offset the improvement in the expense ratio brought by Amoeba reform. But if revenue can achieve double-digit growth, we believe that overall operation cost can be bought into control.

The price of raw wood pulp continues to be high, acquisition of upstream business help to combat

Due to the the increase in wood pulp prices, the gross profit margin of tissue paper business dropped by 5 percentage points to 32.9% in last year. This also dragged the overall gross profit margin down 1.9 percentage points to 46.9%. We estimate that wood pulp prices will continue to rise this year. This will add pressure to the overall gross profit margin. The improvement bought from the launching of high GP-margin products may be fully offset. So we expect the GPM will drop a little bit compared to last year.

Hengan issued an announcement on April 23, announcing the acquisition of Finnpulp Oy. The initial investment consideration is 11,666,666 euros (equivalent to approximately RMB 90,461,700), which accounted for 36.46% of the enlarged issued share capital. Hengan has the right to eventually increase the shareholding to 40 to 49% in 2019-2021.

Finnpulp is currently engaged in planning and aiming to build a large-scale bioproduct mill in Kuopio, Finland. The target of the planned pulp mill is to produce approximately 1.2 million tons of NBSKP and other biological products each year. The project is expected to start this year and be completed in 2021.

We believe that the acquisition can provide Hengan with a stable supply of pulp at a stable cost. If Hengan eventually increase the shareholding to 49%, we expect to supply about 600,000 tons of wood pulp to Hengan by 2021.

According to the information given by the management team, Hengan's historical demand for NBSKP is only 300,000 tons per year, future demand is expected to increase further. It also stated that the next step will be to take the role as a sales agent for Finnpulp's NBSKP production in Asia.

In addition to pulp products, Finnpulp will also have 10% to 20% biological products, which can replace coal mines as raw materials for power generation. Therefore, in terms of overall profit and operating efficiency, Finnpulp is believed to perform better than its ordinary peers. If we refer to the performance of its peer Mesta, the operating profit for 2017 and 2016 remained above 16%.

Sanitary napkins repositioned as feminist personal care business, launching cotton pads and facial care mask products

The high-GPM sanitary napkin business is the best performer among Hengan major business segments in recent years. Its revenue increased by 6.1% last year. It also eased the pressure of rising costs through product mix upgrading. The GPM was reminded flat at 72.2% y.o.y. We expect that this year's sanitary napkin business revenue will maintain a steady growth, and GPM is expected to be maintained through the launching of high-GPM products.

The penetration rate of sanitary napkins in China market is already at a relatively high level. If Hengan's business is limited to sanitary napkins in the future, it will be difficult to achieve higher growth. Therefore, Hengan has repositioned this business as a feminist personal care business.

From the perspective point of different markets in China, cities below 3rd tier are Hengan's relatively focused markets. In the future, as consumption upgrades will bring advantages, accompanying with Hengan's plan of launching of new brands and packaging. Its market share in 1st and 2nd tiers cities is expected to increase.

Hengan completed the acquisition of Wang-Zheng Berhad last year which is with developed distribution network in Southeast Asia market. According to management team, Hengan will launch cotton pad products to mainland market within this year marking the expansion of business to ladies` beauty products. It also plan to launch tampons, followed by facial care masks for the next step.

Wang-Zheng is currently the OEM supplier of cosmetic cotton pads for Watsons and Mannings in Singapore. The planned new products are aimed at female customers, which are the same as the original sanitary napkins. The related registration and study of distribution channels for cotton pads in China market are currently in progress.

Disposable diapers business expected to rebound this year, the proportion of special products in e-commerce platform planned to boost

The revenue from diapers business dropped by 7% y.o.y last year. The keen market competition coupled with the increase in prices of raw materials and petrochemicals, and the unadjusted e-commerce price strategy, all helped to drive the GMP down 3.9 percentage points to 46.9%.

Since the second half of last year, Hengan has taken adjustment measures, including pricing adjustment of e-commerce products, and launching high-end and optimized products. The GMP during the period slightly improved comparing to the first half of the year.

The benefits of the strategic investment in e-commerce and maternity stores began to emerge. Diapers sales in both channels recorded significant growth. Sales from e-commerce channels reached a y.o.y growth of 70% and accounted for over 25% of the overall diapers sales in 2017.

According to the management team, the recovery trend of revenue for diapers has continued for Q1. New products with thinly design and strong water absorption are planned to launch within this year.

At present, high-end diaper market in China grow at a higher rate comparing to lower-end diapers, which implies that parents with growing purchasing power have high demand for the quality of products and low sensitivity to price. Hengan plan to continue to upgrade its products targeting high-end market but not mass market.

We expect that with the rapid growth of e-commerce platform sales, it will provide support for the overall sales of diapers in 2018. The revenue is expected to be stabilized and return to growth path.

Last year, Hengan's overall e-commerce turnover reached 2.02 billion yuan, rising by more than 80% y.o.y. Its contribution to the overall sales increased by 4 percentage points to 10%. Hengan's strategies include keep the same product prices online to be consistent with the offline ones, sometimes even more expensive; launch exclusive products for online channels.

According to the management team, the exclusive tissue paper products account for around 40 to 50% of overall tissue paper products on the ecommerce channels. The mainly difference is the packaging. For diapers, the exclusive ones account for 30%, and sanitary napkins are about 30%. For the latter, most of the products are the same as the offline channels, but the prices are more expensive.

Hengan started strategic cooperation with the major e-commerce operators like Tmall and JD.com. It is expected to further strengthen the cooperation in product development, marketing and supply chain. The company's ultimate target is to boost the contribution of e-commerce business to the overall revenue.

We expect the loss from e-commerce business to be narrow further and revenue will continue to grow at a high rate this year. The contribution of e-commerce business is expected to increase to about 15%.

Investment Thesis, Valuation & Risk

Our valuation model suggests a target price of HK$80.5: We expect that with the help to fast growing tissue paper business, Hengan's revenue will have a 10% increase this year. However, GPM this year is expected to decline slightly from last year due to the rising wood pulp price. But with the help of Amoeba model, the improvements are expected to reflect throughout the year. The operation expense to revenue ratio is expected to improve further.

We give Accumulate rating. Our forecast P/E is 21.1 times and the target price is HKD 80.5 . The risks that need to be watched include top-line growth rate missing from expectation, wood pulp prices fluctuating sharply, industry competition increasing significantly, and Ameba units missing sales target. (Closing price as at 9 July 2018)

Financials

Click Here for PDF format...