|

|

|

*Advertisement* |

|

|

|

|

|

9 Aug, 2018 (Thursday) |

|

|

CAFE DE CORAL H(341)

Analysis:

The Group is principally engaged in the operation of quick service restaurants and institutional catering, fast casual and casual dining chains, as well as food processing and distribution business. For the year ended 31 March 2018, the revenue of the Group was 8.43 billion HKD, with 6.7% growth YoY, whereas the net profit dropped by 8.8%, due mainly to the increasing investment in workforce. In addition to the brand “Cafe de Coral”, The Spaghetti House, Shanghai Lao Lao, Mixian Sense, Super Super Congee & Noodles were also the brands of the Group. Currently, the Group had a network of 366 stores in Hong Kong. Total receipts of fast food shops increased by 5.7% in value and 1.3% in volume in the second quarter of 2018, indicating the fast food market in Hong Kong are growing steadily. Besides businesses in Hong Kong, the Group are eager to develop its businesses in China, and will focus on the Guangdong-Hong Kong-Macao Greater Bay Area, especially Guangzhou and Shenzhen. Currently, the Group had 97 stores in China.

Strategy:

Buy-in Price: $19.30, Target Price: $21.80, Cut Loss Price: $ 18.80

|

| |

|

Yihai International (1579.HK) - Fast expansion of Haidilao underpins future momentum

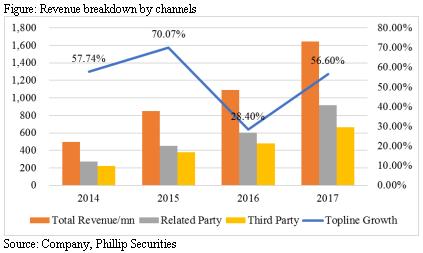

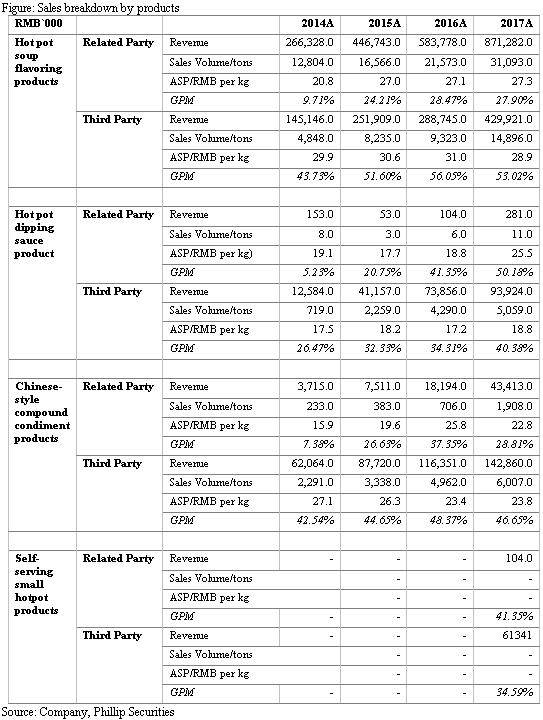

Investment SummaryYihai is a leading and fast-growing compound condiment manufacturer in PRC. This May, its biggest related party Haidilao has submitted hearing materials to HKEX, which showed that Haidilao restaurants would continue to expand at a high speed. As Haidilao's exclusive provider of hot pot soup flavoring products, Yihai is expected to benefit from the quick expansion of Haidilao restaurants. We thus increase Yinhai's EPS forecast to be RMB0.358 in FY18E, assuming 40x PE, and give target price of HKD16.47. (Exchange rate=0.87RMB/HKD) (Closing price at 6 Aug 2018) Business OverviewHaidilao underpins future sales hike. In 2017, revenue from related party Haidilao reached RMB915mn (+51% YoY). Haidilao, owning 273 hot pot restaurants in PRC with daily sales per shop amounting to RMB140k and SSSG keeping 14% in recent 3 years, has submitted listing documents to HKEX in May. It indicates that the number of newly-opened stores will total to 180~220 in 2018E. We thus highlight the great potential for Yihai's sales hike, given it is the exclusive provider of hot pot soup flavoring products to Haidilao.

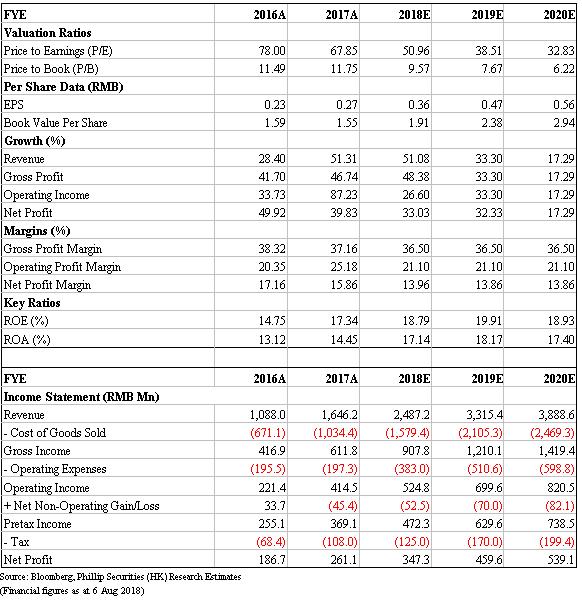

New drivers to topline. The company launched 3 new hot pot soup flavoring products, 5 new Chinese-style compound condiment products and 5 self-serving small hotpot products. Through optimizing and refreshing existing products together with launching new products, Yihai not only upgrades its product mix but also mitigate the problem of insufficient products during low season. We especially highlight that new product, self-serving small hotpot products (自熱小火鍋產品), which realized over RMB60mn sales in 2017 with overall GPM of 35%. Its SSHP under `Haidilao` brand enjoys good reputation among customers and is one of the top 10 in the online shopping platform Taobao. We also highlight the fierce competition risk in this field, given low entry barrier and Haidilao's relatively high ASP. Considering consumers of this fast food are relatively sensitive to selling price, we recognize short-term supplement risk from competitors. But in long run, we highlight Yihai may enjoy greater sustainable growth momentum in this field, given Haidilao's brand advantage and high quality control measure as the industry leader. Third party channels. As up to 2017 end, Yihai's distributors have covered 31 Chinese provinces and cities, HK, Macau and 23 overseas regions. This is mainly attributable to its adjustment of distribution channels in 2016 and continuous effective controls of customer-end. We estimate the sales to distributor reached RMB600mn in 2017 with 35% YoY growth. Meanwhile the e-commerce channel continued rapid development with currently five online flagship shops and income of RMB105.9mn in 2017 (+265.2% YoY). Robust 17 results. In 2017, Yihai recorded revenue of RMB165mn (+51.3% YoY) and net profit of RMB261mn (+39.9% YoY). GPM dropped from 38.3% in FY16 to 37.2% in FY17 mainly due to rising material costs. Valuation & RisksWe assume the exchange rate to be 0.87RMB/HKD, target PE 40x, FY18 EPS RMB0.358, thus we get TP of HKD16.47(Closing price at 6 Aug 2018). Risks include: Rising COGS; Fierce competition; Haidilao expansion fails expectations; Food safety problem.

Financials

Click Here for PDF format...

| Recommendation on 9-8-2018 | | Recommendation | Neutral | | Price on Recommendation Date | $ 15.880 | | Suggested purchase price | N/A | | Target Price | $ 16.470 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|