Investment Summary

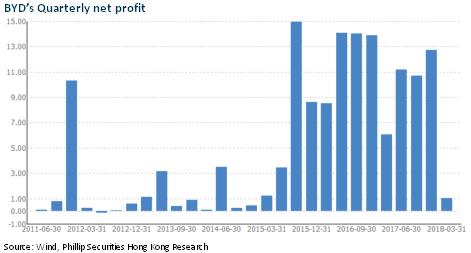

BYD has actively opened up the supply chain system to promote the outside supply of power batteries and spare parts, thereby inspiring the vitality of enterprises and enhancing their competitiveness. With the breakthrough and accelerated implementation of the transformation project, the company's future development momentum is expected to be strengthened. We hold the judgement that 2018 H1 will be a low point for BYD's automotive business and the new energy vehicles and conventional fuel vehicles will exert their power in H2, which will help the company's profit bottom out. We give BYD BUY rating (Closing price as at 8 August).

Joining hands with Changan Automobile, and making breakthroughs in power battery outside supply

On July 5, BYD signed a strategic cooperation agreement and a battery joint venture cooperation framework agreement with Changan Automobile. According to the agreement,

a. the two parties will integrate their respective resource superiorities in new energy, intelligence, overseas market and shared mobility to carry out all-round cooperation.

b. The two parties will jointly establish a new energy power battery joint venture company, jointly invest RMB5 billion to build 10Gwh battery capacity in Chongqing, and implement it in phases. It will reach 5-6GWh in the first phase and 4-5GWh in the second phase, supporting the power battery demand of Changan Automobile.

c. Changan Automobile will become a shareholder of BYD's battery business, and work together via in-depth technical cooperation in the subdivisions such as new energy vehicle industry chain, intelligent network, intelligent interaction, and unmanned driving in the future.

While in April of this year, Changan Automobile has already reached a cooperation with BYD to jointly develop a three-in-one product for the new energy vehicle electric drive. The product is expected to be launched with a new certain model of Changan Automobile next year.

Boxing out in advance and binding car companies to prepare for the knockout match

Due to the adjustment to the state subsidy policy and the changes in the financing environment, joint ventures and emerging car manufacturers have officially entered the competition arena. While the power battery market is developing rapidly, it is also entering the reshuffle phase of the survival of the fittest. The market share of the top five power battery companies with installed capacity increased by 10% to 71% compared with 2017 in the early five months of 2018. The CATL and BYD's share increased by 19% to 63% from the 44%, and the head effect is becoming more apparent. The CATL has established a joint venture factory with SAIC and Dongfeng, developed it with Honda, and entered the supply chain of Mercedes-Benz, Volkswagen, BMW and other car companies. The challenge is unprecedented in the future competition.

We believe that the joint venture with Changan Automobile and the deep integration mark a breakthrough in BYD's outside supply of power batteries, which is a key first step in the listing of BYD's disconnecting power battery. In addition, BYD's power battery has entered two electric trucks` supporting of Dongfeng Automobile. At present, BYD's battery capacity is 26GWh, and its total production capacity is expected to reach 60GWh in 2020, while the CATL's capacity in 2017 is 17GWh, and it is expected to reach 31GWh in 2018.

Joining hands with Faurecia stripped car seats, opening the supply chain and taking a solid step

On the same day, the auto parts company jointly established by BYD and Faurecia was unveiled the nameplate in Shenzhen. BYD holds 30% of the share and Faurecia holds 70%. BYD announced a strategic transformation a year ago to change its previous highly vertical integration strategy, reducing capital pressure and improving operational efficiency. We believe that the successful divestiture of the seat business is another milestone in the company's strategic transformation and the realization of the supply chain from closure to openness. It has great strategic significance for the company's long-term development, which will help the company to focus more on its main business and consolidate its leading position.

Investment Thesis

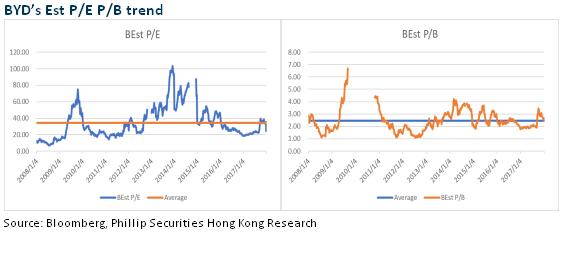

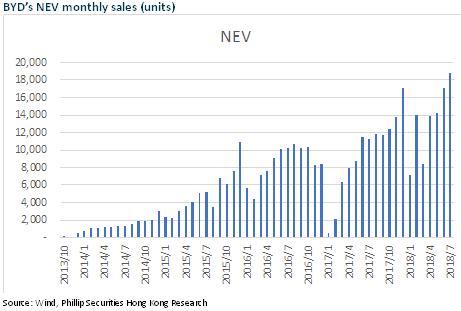

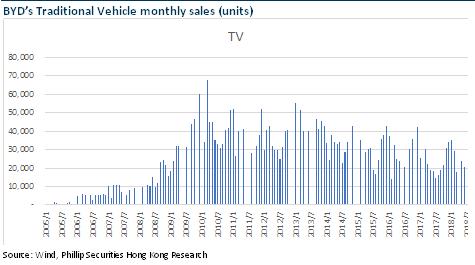

BYD's NEV sales hit a record high in July, reaching 18,793 units. It has risen month by month since 2018, with a total of nearly 94,000 units in the first 7 months, accounting for about 85% of the 2017's total sales. Among which, June and July saw more than 50% lift over the transition period. The sales of traditional fuel vehicles totaled 168,000 units in the first 7 months, up 11% yoy. What's more, driven by the new car Song MAX, the sales structure has improved significantly. The new model of Qin and Song MAX PHEV version, which will be launched in 2018H2, is expected to continue to contribute the momentum.As the latest estimates, we adjusted the expected EPS of 2018 to RMB1.44, and add our 2019 expected EPS to RMB 2.18. Thus, we revise the target price to HKD52, which corresponded to 31/21x P/E and 2/1.8x P/B ratio for 2018/2019. We give the rating of “BUY” (Closing price as at 8 August).

Risk

Sales of new energy vehicles is not as good as expected

Cloud Rail business risk

Slow-down of Hand-set components business

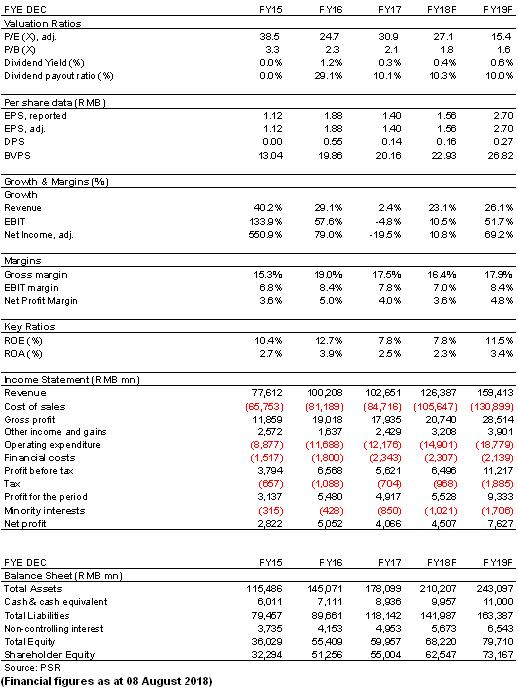

Financials

Click Here for PDF format...