Investment Summary

China's dairy product consumption is still in a period of steady growth. With the increase in disposable income of households and individuals, relaxing of two-child policy, we are optimistic about the prospects of the dairy industry. The State Council has released a circular in last June to guide the industry's development. It says the whole industry should be revitalized by 2025. It encourages the integration of dairy enterprises, promotes milk-drinking program to students and cultivates national habits of dairy-product consumption.

Mengniu as one of the market leaders, is expected to benefit from both national policies and the growing trend of the industry, which help it to further increase its market share. With the new management team lead by CEO, Minfang Lu, actively investing resources to carry out product innovation and upgrading, its business recovery momentum is obvious, and the business in the third and fourth tier cities maintains rapid growth.

In addition to the domestic market, Mengniu is also actively engaged in the overseas market layout. It also proposes to achieve a target of RMB100 billion in sales by 2020. It is expected to achieve the target through promoting high-margin innovation products, and external mergers and acquisitions.

According to the management team, the sales growth target of FY2018 is double digit aiming to increase the market share. In fact, the actual sales growth of FY2017 reached 11.9%, higher than the internal guidance of high single digit. As we consider its faster pace of launching new products this year, as well as increasing brand investment, including sponsoring the World Cup and increasing advertising costs, its sales target can be met.

We also consider the high-base effect for 2H, and the downward pressure on China's economic growth, the revenue growth of 2H in FY2018 is expected to slow down from the 1H, but it is still able to achieve double digits throughout the whole financial year.

At the same time, we have also considered that its milk-powder business platform,i.e. Yashili (1230) is expected to return to profit making in FY2018, whereas its material associate China Modern Dairy (1117) is expected to reduce losses sharply, and the ice products business is expected to resume from loss-making.

Facing the potential increase of raw milk price, the management team has no plan to tackle it through end-product price hikes. But as we consider its new products launching within the year are with higher gross profit margin, we expect this can fully offset the pressure from raw milk and help to bring the overall GPM to expand y.o.y.

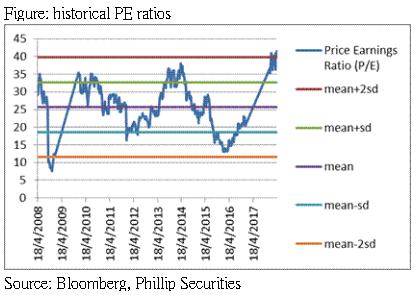

As the management team plan to increase its investment in branding, especially in advertisements, to boost its sales for greater market share, we expect its SG&A expenses to revenue ratio will increase y.o.y. We give Mengniu Buy rating, a forecast PE of 31 times and target price of HKD28.5. (Closing price as at 10 August 2018)

Business/Industry Overview

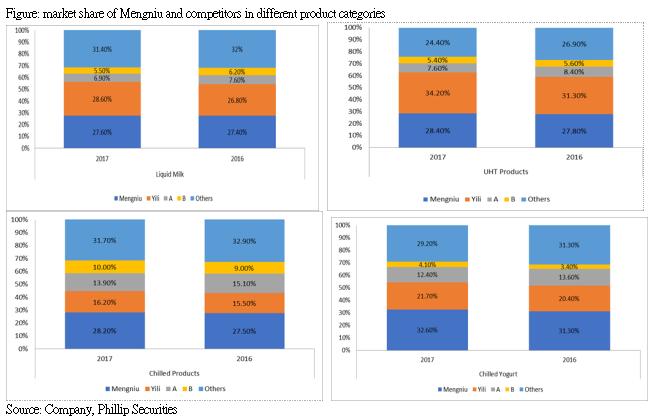

The two leading companies in China's dairy industry are Yili and Mengniu. The market shares of liquid milk, UHT products, chilled products and chilled yogurt have all increased y.o.y in 2017. Mengniu is the market leader in chilled yogurt and chilled products. Its market share has increased by 1.3ppt and 0.7ppt respectively, to 28.2% and 32.6%. Compared to Yili, the later's market share still has a big gap of 12ppt and 10.9ppt respectively.

Mengniu was the second largest in markets of liquid milk and UHT products. Its market share has increased by 0.2ppt and 0.6ppt, to 27.6% and 28.4% respectively. However, compared to chilled products and chilled yogurt, the gap with the largest market player is less as 1ppt and 5.8ppt respectively.

New management team aims to enhance product innovation

Under the leadership of the new management team, Mengniu has completed the organizational restructuring and the business has been categorized into room temperature product business, chilled product business, milk formula business and ice cream business. According to the management, the internal target for milk formula and ice cream businesses is to reach breakthrough growth.

Mengniu also plans to its product innovation capability. It aims to recruit 60 R&D personnel in this year. It is expected to help it launch more high-margin new products in the future.

The company plans to launch 40 new SKUs this year, which is a significant increase compared with last year. Among different product category, there will be 6 to 7 SKUs adding to the fast-growing room temperature yogurt business. We expect that as Mengniu further strengthens product innovation and continues to improve its advertising and sales channels, the gap of market share between Yili in room temperature product market, can be further narrowed in the next couple of years.

Yashili is expected to return profit-making

The sales grew 11.9% in FY2017 and 9ppt was contributed by sales volume growth. We expect the sales growth for FY2018 will also be mainly driven by volume. According to the management team, for the sales target of each business, Yashili is set more than 20%, ice cream business is over 10%, and liquid milk business is at least high single digit.

Yashili has recorded a loss in FY2017. But both top line and bottom line showed improving trend since 2H and the trend has continued in Q1 of FY2018 according to the management team. The team plans to promote high-end products and improve product mix. It will also continue to improve mother-and-baby channel, and maintain multi-brand and multi-category business strategies. It will improve operation efficiency including same-store growth.

From 1 January 2018, the Infant Formula registration requirements in the new Food Safety Law came fully into force. Infant formula products, either domestically manufactured or imported through general trade, must obtain formula registration before they can be sold in China. We believe that this can help to raise the entry barrier of the industry, accelerate the pace of integration, thus optimization the production capacity structure. Mengniu, as one of the leading companies in the market, is believed to benefit from the trend.

The pressure on raw milk prices is increasing in the second half of the year

Taking into account the seasonal factors in 2H of FY2018, as well as the intensified trade disputes between USA and China, which can all help to drive up the cost of cow's food such as soybean and corn, we expect the raw milk price to be higher than 1H. The recovery of raw milk prices will help to improve the financial performance of China Modern Dairy. In addition, there will be no one-off provision of RMB500 million as last year. We expected the loss will be shrank substantially and recorded a break even.

Overseas market development and M&A opportunities bringing potential for medium and long-term

Mengniu's room temperature and chilled product businesses is growing fast in 3rd and 4th tier cities, this market are expected to become the future growth diver for Mengniu. For the time being, the market size in this market still needs to be improved, and the 1st and 2nd tier cities are still the main source of overall sales revenue. The products sold in both markets are similar currently.

Apart from China market, Mengniu plans to further develop its overseas market this year, especially in Southeast Asia. The Indonesian plant is currently under construction and it is expected to be put into operation in 2H, which will mainly supply local and surrounding market demand.

Mengniu's sales target for the year 2020 is RMB100 billion. To achieve this goal, we expect annual sales to maintain double-digit growth and with the help of potential opportunities of M&A. According to the management team, it will seek M&A opportunities in both China and overseas, as long as they are in line with the core strategy of Mengniu. Mengniu has basically completed the layout of the upstream raw milk, so it plans to mainly invest resources in downstream branding and channels.

Valuation and risk

We are optimistic about the industry and the company's prospects, giving a rating of Buy, with forecast PE ratio of 31 times and target price of HKD28.5.

We expect the company is able to meet double-digit sales growth target this year, with an expansion of GPM. Its SG&A expenses to revenue ratio will increase. Its material associate China Modern Dairy is expected to record a break even.

Potential risks include failure to meet revenue growth, lower profit margins than expected, and huge fluctuations in raw milk prices. (Closing price as at 10 August 2018)

Financials

Click Here for PDF format...