Investment Summary

Anta announced interim results and we highlight that 1) Fila performance exceeds expectation; 2) new brands continue improving store network; 3) E-commerce will account for 20%-30% of revenue in future. We expect that the company will leverage on strong distribution channels and store network as well as the launch of new popular products to consolidate its leading position. (Closing price at 17 Aug 2018)

Event

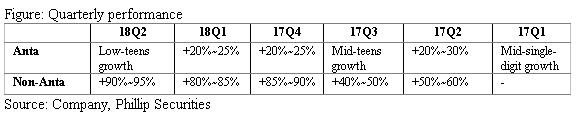

Solid 18H1 results. The company revenue increased by 44% YoY, and gross profit was up by 54% YoY due to effective cost control, while net profit attributable to shareholders climbed by just 34% YoY. By products, sales of footwear/apparel/accessories was up by 21.3%/64.6%/51.3% respectively, with GPM rising by1.9/4.3/4.5ppts.

Comment

Rising expenses dragging down profit margin currently. OPM decreased by 0.4ppts, due to rising expenditures regards to A&P amortization and retail level marketing and promotional activities as well as R&D. We see NPM was down by 1.4ppts, which is because exchange loss and hiking tax rate.

Improving operation efficiency. Although inventory days raised by 15 days to 83 days, which is mainly resulting from higher percentage of Fila sales in topline (after all Fila has higher inventory days around 120 days while Anta around 50~60 days). Mgt emphasized that inventory days of Fila is decreasing while that of Anta is rising for e-commerce hike, which overall indicates a healthy inventory level. Meanwhile, AR days dropped to 35 days while AP days remain unchanged around 49 days.

Net operating cash flow decreased to RMB1.475bn (vs. 2.058bn in 17H1), attributable to inventory hike of Fila and new brands, and mounting account receivables due to advanced purchase of raw materials (mainly eider down) for winner production. Mgt indicated that cash flow condition would be normal throughout the year.

Fila growth higher than expected. Fila biz recorded over 85% YoY growth in 18H1 with extending same store sales (from RMB400k to RMB600k now) and climbing stocks. The company also launches Fila Fusion, a trendy sportswear series which targets youth market, as a new momentum. Therefore, Fila now has complete product lines to cater for different customer demand involving adults, youth and kids.

Development of new brand. Anta operates four relatively new brands for various markets. 1) Descente, focusing on high-end sportswear products for customers aged 25~35, now owns 85 store and expands smoothly in Northeastern China. 2) Sprandi provides fashion and lifestyle footwear products, to focus on mid-end clients with 81 stores in China. 3) Kolon offers outdoor sportswear, located in tier 2-3 cities with 189 stores. 4) Kingkow, positioned into mid- to high-end kidswear market, was acquired in 2017 and operating 63 store in greater China area. The company is adjusting and developing store network of these new brands.

Valuation

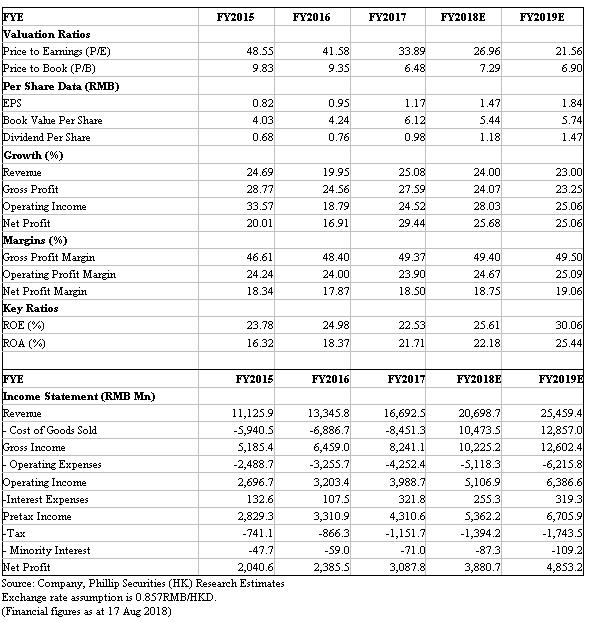

We maintain target price to HKD47.3: Forecasted EPS is RMB1.47/1.84 in 18E/19E and target price is maintained as HKD47.3. (Closing price at 17 Aug 2018)

Risks include: Rising selling and R&D expenses; Fierce competition in retail market; Inefficiency resulting from multi-brand operation.

Financials

Click Here for PDF format...