|

|

|

*Advertisement* |

|

|

|

|

|

31 Aug, 2018 (Friday) |

SINOFERT(297)

Analysis:

Despite the fact that the Chinese fertilizer industry is still facing excess capacity and the growth of global fertilizer demand is slowing down, Sinofert Holdings (297) still managed to achieve satisfactory results in the first half of 2018, mainly because the Group actively carried out strategic sourcing and the distribution channel expansion strategy known as DTS, further strengthened synergy effect of various operations, focused on increasing sales of differentiated products and worked hard to rein in cost and expenses. For the six months ended 30 June 2018, the sales volume of the Group was 6.72 million tons and revenue was RMB13.037 billion, up by 10.34% and 25% respectively over the corresponding period in 2017. Net profit attributable to shareholders was RMB315 million, a remarkable increase compared to RMB13 million of the corresponding period in 2017. Gross profit margin was 8.33%, which was relatively stable compared to the corresponding period in 2017. Annualized ROE was 9%, up 8.7 percentage points year on year. (I do not hold the above stock)

Strategy:

Buy-in Price: $0.88, Target Price: $0.96, Cut Loss Price: $0.84

|

|

CHINACOMSERVICE(552)

Analysis:

In 1H18, CCS focuses on expanding domestic non-telecom operator market and proactively controll the development of the products distribution business. It realized total revenues of RMB50.8bn (+13.2% yoy), in which core businesses revenue increased by 17.1% yoy. Cost of revenues amounted to RMB44.6bn (+13.9% yoy). Gross profit increased by 8.2% yoy to RMB6,176mn. Due to the decreased service prices and increased costs in relation to labor, GPM was 12.2% (-0.5pp). With continued effort on controlling the SG&A expenses, such expenses amounted to RMB4,661mn and its percentage over topline further decreased by 0.5 percentage point yoy to 9.2%. Profit attributable to equity shareholders of the company grew by 8.6% yoy to RMB1,595mn, and the growth rate increased by 2.7 percentage points yoy. NPM was 3.1%, decreased by 0.2 percentage point year-on-year. Basic EPS amounted to RMB0.23 (+8.6% yoy). Due to the significant increase in free cash flow last year, free cash flow dropped to RMB877mn, but still accounted for over 50% of the profit attributable to equity shareholders.

Strategy:

Buy-in Price: $6.04, Target Price: $8.00, Cut Loss Price: $5.00

|

| |

|

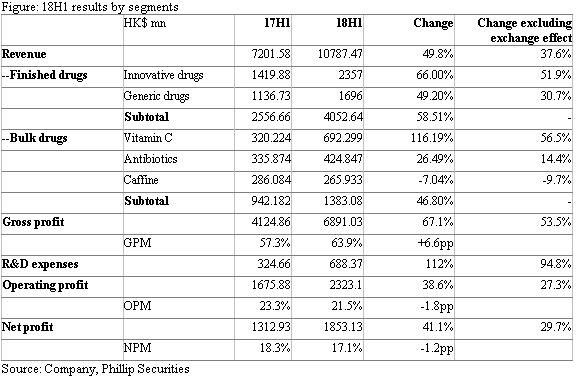

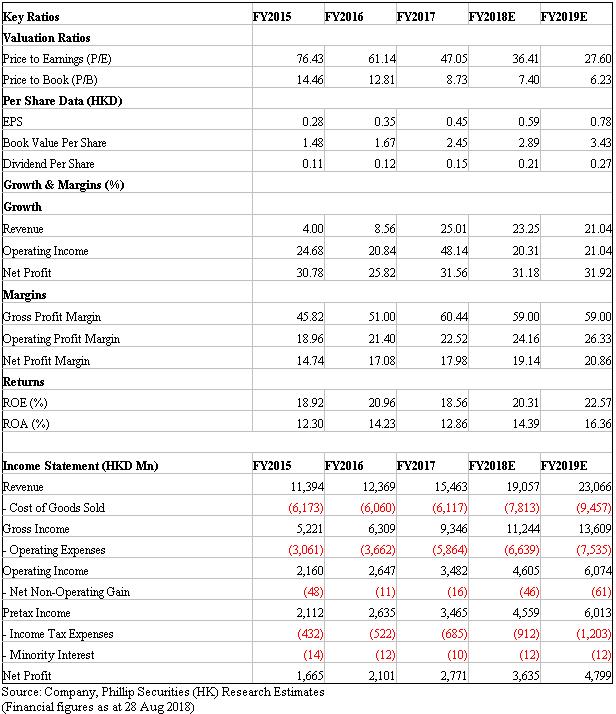

CSPC Pharmaceutical (1093.HK) - Comments on 18H1 Results

Investment SummaryCSPC announced 18H1 results last week with strong revenue and profit growth. We maintain EPS forecast of HK$0.59/0.78 for 18E/19E, and target price of HK$24.8 on the basis of a target P/E ratio 42x. (Closing price at 28 Aug 2018) Business OverviewFinancial review. Total sales increased by 49.8% yoy to HK$10.79bn in the first half, mainly due to the sustained strong growth of innovative drugs (now 45.2% of the total revenue), and recovery of Vitamin C business which also drive the profitability of this business up. The profit attributable to shareholders increased by 41.1% yoy to HK$1.85bn. Cash flows from operating activities climbed to HK$2.18bn (HK$1.27bn in 2017). Operation efficiency improves. Average turnover period of accounts receivable increased slightly from 40 days to 37 day, and inventory days dropped from 173 days to 150 days. Escalated expenses. OPM dropped by 1.8pp due to rising selling and R&D expenses. R&D expenditure rose 112% yoy to HK$688mn, more than 60% of which was spent on innovative drug R&D, and some on conformity assessment and generics. In the next few years, CSPC will continue to invest heavily in innovative drugs thus we expect that R&D cost is expected to remain relatively high. Selling expenditure ratio rose to 33.35% in 18H1 from 25.8% in 17H1, mainly resulting from continued expansion of sales team and increased cost of academic promotion. According to company guidelines, the number of salesmen for NBP will increase to about 1500 by FY17 end, and that for Xuanning and Olaining will reach more than 600 respectively. Also CSPC proactively promotes the consistency evaluation of generic drugs. At present, products that have passed consistency evaluation include azithromycin tablets, tramadol hydrochloride tablets and captopril tablets, etc. Innovative medicines. Innovative drugs achieved HK$48.7 in 18H1, up by 65% yoy. By products, NBP achieved sales revenue growth of 42.6% to HK$2.36bn, with 28% growth for capsules and 57.5% for injections. Albumin paclitaxel has come into market since Mar, which grows quickly realizing sales of HK$86mn yet. Albumin paclitaxel has now entered five provinces’ drug reimbursement list and covers 290 hospitals. Sales target according to Mgt was HK$300mn/1bn for 18E/19E. Revenue of Oulaining increased by 78% to HK$1bn, and that of Xuanning injections increased by 105% to HK$580mn. Generic medicines. Sales of generic drugs reached HK$3.31bn, a notable increase of 42.3%, mainly because the company continues to intensify promotion of non-antibiotic drugs and expand oral products for chronic diseases. High-end antibiotic products (Meropenem for injection) and health products (vitamin C buccal tablets) also maintained rapid growth. The company indicated that it would consider divestiture or sale of VC business. Currently, VC business provides stable cash flow for the group, and has higher than industry average profit margin. While its gross margin will further increase, if the divestiture of Vitamin C business happens. Valuation Thesis & RisksWe maintain target price at HK$24.8. Solid 18H1 results further prove its growth momentum that coming from expanding salesman team and newly-launched drugs. We remain TP of HK$24.8 to factor into concerns about improving expenditures (for sales and R&D). Risks include: R&D failure; Slow than expected sales growth; Rising expenses.

Financials

Click Here for PDF format...

| Recommendation on 31-8-2018 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 20.450 | | Suggested purchase price | N/A | | Target Price | $ 24.800 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|