Investment Summary

GAC Group's 2018 interim results were in line with expectations, and sales in July/August 2018 recovered well. It is expected that the Company will maintain steady growth this year under the strong product cycle of the joint venture car companies. We revised the Company's 2018 earnings forecast and introduce the predicted value of 2019. We reaffirm the "Buy" rating with the target price to HKD 11. (Closing price as at 5 September)

Mid-term result basically in line with expectations

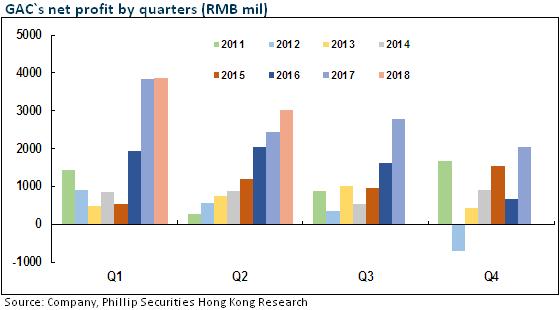

According to GAC's latest result report, the net profit attributable to the parent company in 2018 H1 increased by 10.3% yoy to RMB6.91 billion, which is basically in line with our expectations. Earnings per share were diluted to RMB0.68 due to the expanded share capital by 12.8%, and the interim dividend was RMB0.1.

The growth of the Group's car sales volume slowed down in H1

At the group level, GAC's total sales volume recorded 1,017,000 units in H1. The increase in the base number and the slowdown in the industry slackened the growth rate from over 30% in the last year to 5.5%. Among them, GAC Honda/GAC Toyota/GAC's self-developed brands/GAC Fait/GAC Mitsubishi increased by 5.5%/16.4%/6.9%/-35%/38%, respectively, contributing the incremental sales of 17,631/35,932/17,319/-38,119/20,951 units, respectively.

Gross profit margin increased by 3 ppts, and the cost rate slightly increased

Factors such as the scale effect and cost control brought by the increase in the sales volume of Trumpchi increased the gross margin by 3 ppts yoy to 19.6%. However, due to the RMB280 million expenses of the increased advertising investment, destocking promotion of the old GS4 in Q2 and equity incentives in H1, sales expenses and administration expenses increased by 2 and 1 ppts yoy, respectively. Financial expenses decreased by 41% yoy due to the decrease in interest rates and borrowings. The operating profit margin was 7.75%, showing a slight decrease of 0.1 ppts compared with 7.86% in the same period of last year, which we believe was caused by the increase in the marketing and management expense rate, and the not yet formed scale effect of new energy cars under the self-developed brands.

Joint venturecontributed a record high profit

In H1, the Company's sales revenue increased by 7% yoy to RMB37.2 billion, mainly due to the continuous product enrichment and sales growth of its self-developed Trumpchi models, and the rapid development of auto parts and after-sales services in the upstream and downstream of the industrial chain. The total revenue of the Group, together with the joint ventures and affiliated businesses, increased by 6.22% yoy to RMB172.6 billion. In addition to the continuously growing sale volume of self-developed brands, the steady growth of Japanese joint venture products and the corresponding expansion of supporting businesses were also one of the driving factors. Benefiting from the best-selling models of the 8th generation Camry/Levin/Avancier/Outlander, the profit share of joint ventures and affiliated businesses increased by 7.4% yoy to RMB4.94 billion, setting a new record after the listing, accounting for 65% of profit before tax.

Prospects of Japanese cars are optimistic, while self-developed brands will undergo trials

With the improvement of China-Japan relations and the new product cycle, we are optimistic about the future prospects of GAC Honda/GAC Toyota/GAC Mitsubishi, and GAC Fait is still under adjustment. New cars under the self-developed brands to be launched in H2 include the mid-term modification of GS4, the upgrading of GS5, and the GM6 of medium-sized MPV. At present, GS3/GS4/GS5/GS8 constitute the core lineup of the Company's self-developed brand SUV models. In order to make up for the insufficiencies of the self-developed brands in the sedan models, the new generation models of GA6/GA8/GA4 will also be launched according to the planning in the coming years. Due to the increasingly fierce competition in the domestic SUV market, we believe that GAC's self-developed brands will encounter market trials in the short term.

Investment Thesis

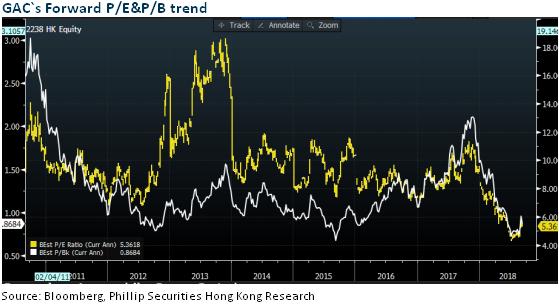

GAC Group's 2018 interim results were in line with expectations, and sales in July/August 2018 recovered well. It is expected that the Company will maintain steady growth this year under the strong product cycle of the joint venture car companies. We revised the Company's 2018 earnings forecast and introduce the predicted value of 2019. We reaffirm the "Buy" rating with the target price to HKD 11, equivalent to 7.6/6.9x P/E ratio in2018/2019.

Financials

Click Here for PDF format...