Investment Summary

The revenue growth of traditional ERP was faster-than-expected, due mainly to the strong demand in Kingdee EAS; while the growth in Cloud business was below market expectation, up 25.6% YoY only. However, the group has launched their new product – Kingdee Cloud Cosmic, the first ever PaaS platform for the group. We believe it will bring positive impact for its cloud business in long term. But, because of the depreciation in RMB, we give a target of $8.74, 2.2% lower than previous, initiating “Neutral” recommendation. (Closing price at 7 Sep 2018)

Performance update

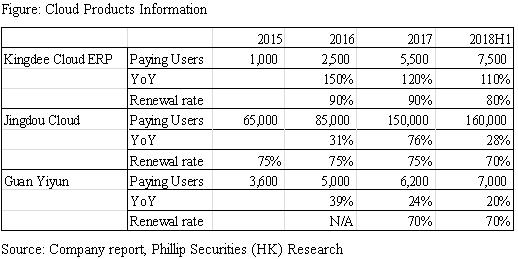

Slower-than-expected growth in Cloud business with slightly decreasing renewal rate

The growth in cloud business was below the market expectation, where the reported revenue in cloud for half year was RMB 355 million, up 25.6 YoY%. However, if taking the deferred revenue into account, the real growth in cloud for half year was 45%, but still lower than expected. The revenue of Kingdee Cloud rose 43% YoY, and its renewal rate slightly dropped to 80%, yet its user growth maintained above 100%, accounting for over 7500 clients. The revenue of Jingdou Cloud increased 30% YoY, and kept its renewal rate in 70%, but the user growth reduced from 75% to 28%, with over 16 million users. The revenue of Guan Yiyun fell 17% YoY, while the renewal rate and user growth rate remained unchanged at 70% and 20% respectively. The paying users also exceeded 7000. Besides, the operating loss margin was slightly up from 18.6% to 19%.

Faster-than-expected growth in traditional ERP

Unlike cloud business, the growth in traditional ERP was above the marker expectation, where the reported revenue for half year was RMB 923 million, up 19.4 YoY%, due mainly to the strong demand from Kingdee EAS. The revenue growth of EAS, K/3 and KIS were 29%, 14% and 14% respectively. Boosted up by strong growth in Kingdee EAS, the revenue from implementation and maintenance rose by 25% and 18% YoY. In addition, the operating profit margin was up from 18.9% to 21.7%, demonstrating an improving profitability in traditional ERP business.

Business update

First ever PaaS product - Kingdee Cloud Cosmic

On Aug 8, Kingdee has launched the second generation of cloud ERP products - Kingdee Cloud Cosmic, mainly for large and mega enterprises with revenues higher than 10 billion. And it targets conglomerate, construction, and new retail. Currently, four enterprises have signed with Kingdee, including Huawei Infrastructure, WENS, Ecolovoz and Xiamen C&D. The price for software leasing is ranging from $300,000 to $500,000. Other than SaaS, Cosmic also provides PaaS services. In the past, Customers will be affected whenever Kingdee tries to provide customization to a single customer under a traditional SaaS product. Now, through the DDM dynamic cloud model, the micro-service is built, and Cosmic adjusted functions through the API to ensure that multi-tenancy structure will not be affected. In addition, users can develop customized modules through modeled component. 70% of the codes can be saved. It only needs to drag the interface, and the document template can be completed in less than three minutes. The ultimate goal of the development platform will need no code at all, which reduces the development cost of enterprises. As a result, we believe that more customers will shift from Kingdee EAS to Cosmic in the future.

Promotion of enterprises cloud migration from government

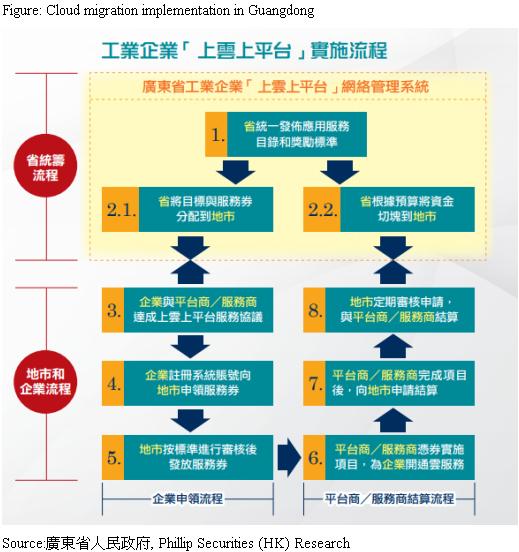

On Aug 10, the Ministry of Industry and Information Technology launched the “The Action Plan for Enterprise Cloud Migration in 2018-20”, which accelerates the promotion of enterprises in key industries in order to strengthen the service and operational capabilities of cloud computing platforms. The plan requires the provinces to carry out propaganda and training for cloud platform service providers and industry enterprises to match up their supply and demand. Taking Guangdong Province as an example, the provincial government will use vouchers to subsidize enterprises to adopt cloud services, in order to increase the incentives for enterprises. Kingdee has been included in the list of enterprise cloud service providers in 8 provinces, including: Guangdong, Guangxi, Hubei, Shandong, Jiangsu, Zhejiang, Sichuan and Hunan. Among them, the top 50% of enterprises in Hunan Province are Kingdee Cloud.

Valuation

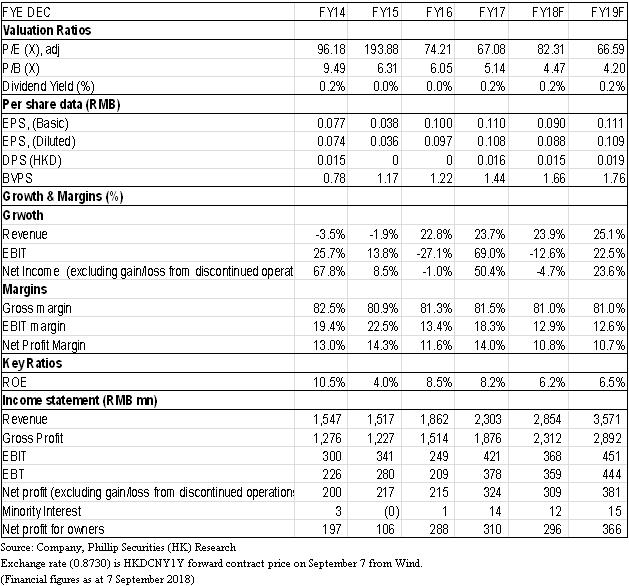

We adopted sum of the parts valuation by dividing the business into three parts: 1) Traditional ERP business (P/E), 2) Cloud business (P/S), and 3) Investment real estate business (book valuation). We forecast the earnings per share of the traditional ERP business in 2018 to be RMB 0.107, 11.5% higher than the previous estimate, still with target PE ratio 28x; the revenue of cloud services per share in 2018 would be RMB 0.250, 6.7% lower than the previous estimate. We raise the target PS ratio from 13x to 15x, reflecting our positive view on Kingdee Cloud Cosmic in long term; for the investment real estate business, the book valuation is used, and the valuation per share is RMB 0.52. Finally, a net cash is RMB 0.31 per share at the first half of 2018. A target price of HK$8.74 was obtained, 2.2% lower than previous target price due to the RMB depreciation, and we remain “Neutral” recommendation. (HKD/RMB: 0.873)

Risk

1. Slower-than-expected growth in cloud products

2. The economy of China slows down

3. Cloud ERP may take away the existing customers of traditional ERP, particularly SME

Financials

Click Here for PDF format...