|

|

|

*Advertisement* |

|

|

|

|

|

13 Sep, 2018 (Thursday) |

WEIGAO GROUP(1066)

Analysis:

At the beginning of the year, Shandong Weigao Group Medical Polymer (1066) optimized its product strategies, reclassified from former single-use consumables, hemodialysis business and orthopedic business into eight business segments, comprising clinical nursing care, wound management, blood management, pharma packaging, medical testing, anesthesia and surgical related products, orthopedics and interventional products. These segments cover an enormous size of market. For the six months ended 30 June 2018, the revenue of the Group was RMB4.15 billion, representing an increase of 39.4% over the same period last year. Turnover of high value-added products (with a gross profit margin of over 60%) accounted for 61.7% (same period last year: 57.9%) of the total turnover. Excluding extraordinary items, net profit attributable to shareholders was RMB762 million, representing an increase of 17.2% when compared with the same period last year. (I do not hold the above stock)

Strategy:

Buy-in Price: $7.30, Target Price: $8.00, Cut Loss Price: $6.90

|

|

HC GROUP(2280)

Analysis:

The businesses of the group can be divided into three parts, Information, Transaction and Data, in the hope of creating an industrial internet ecosystem that founded by data, formed by transaction and supported by information. Information service segment is formed by ZOL.COM.CN and HC360.COM; transaction service segment consists of UnionCotton, IBUYCHEM, and China Formwork; data service segment is made up by PanPass and Trading Wisdom. The business model of UnionCotton and IBUYCHEM is to create a platform, gathering the orders from downstream, in attempt to lower the average cost for small merchants in downstream. Transactions, settlements, transportation, and financing are provided in the platform. Besides, that of China formwork is to build up a materials bank in the construction formwork industry, creating a platform for construction companies for design, installation, maintenance and refurbishment, supply chain financing, and sub-leasing and leasing business. The group had remarkable interim results, and announced a positive profit warning, up 182.3% and 37.9% YoY in revenue and net profit respectively.

Strategy:

Buy-in Price: $5.00, Target Price: $6.50, Cut Loss Price: $4.30

|

| |

|

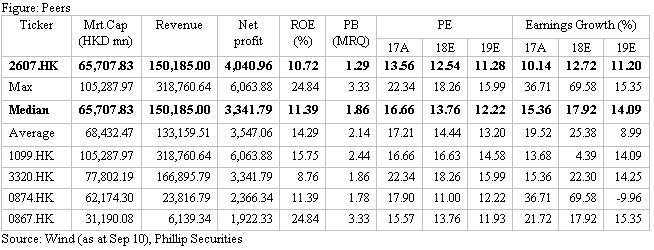

Shanghai Pharma (2607.HK) - Comment on 18H1 Results: Strong Momentum of Manufacturing and Coming Rebound of Distribution

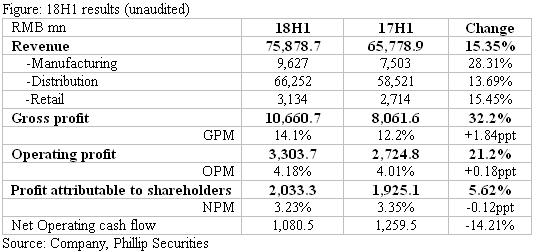

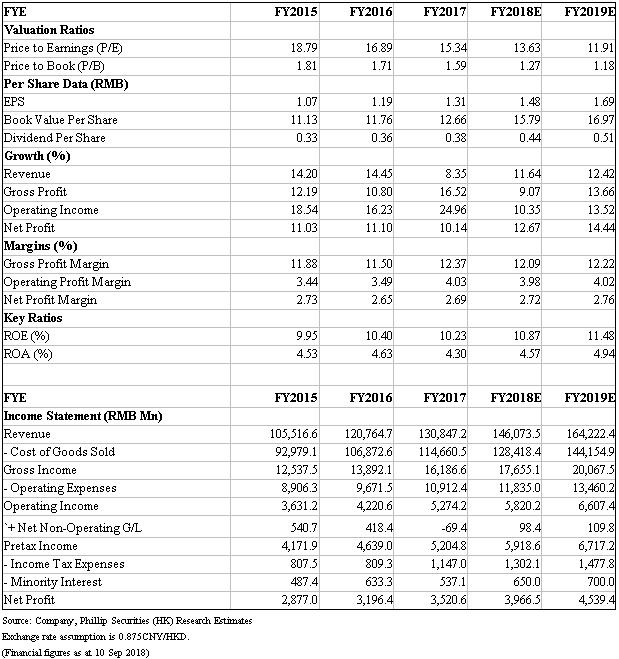

Investment SummaryThe company publishes interim results that the manufacturing business and retail part have maintained rapid growth, and the distribution segment has maintained double-digit growth under the influence of the two-invoice system (TIS). Profitability continued to improve with rising margins. It is expected that distribution business will recover in 18H2. We maintain EPS forecasts and adjust the target price to HK$24.0 to factor into further devaluation of RMB. (Closing price at 10 Sep 2018) Business OverviewSolid 18H1 results. The company achieved topline of RMB75.87bn (+15.35% yoy) and net profit attributable to shareholders of RMB2.03bn (+5.62% yoy). Shareholding enterprises contributed RMB353mn, down by 9.74% yoy, mainly resulting from channel adjustment under TIS and some drugs experiencing price reduction after entering drug reimbursement lists. Net profit after deducting non-recurring G/L and share profit contributed by invested companies increased by 11.58% yoy. Profit margins steadily increased. Gross margin recorded 14.10%, up by 1.84 percentage points (ppt) , with the manufacturing up by 5.35ppt and the distribution up by 0.62ppt. Excluding management, sales and R & D expenses, OPM rose by 0.17ppt to 4.18%. Operating cash flow fell 14.21% yoy, which was mainly due to the high base of 17H1 according to Mgt, and dose not affect the company's current good operating conditions. Manufacturing segment. It achieved revenue of RMB9.627bn (+28.31% yoy), GPM of 57.66% (+5.35ppt), R&D expenditure of RMB479mn (+28.29% yoy), accounting for 4.98% of manufacturing revenue. The continued high growth was mainly due to the company's focus on key products and the implementation of "one product, one policy". In 18H1, sales of 60 key products reached RMB5.158bn (+30.19% yoy) and GPM of these was 74.92% (+4.75ppt). With the accomplishment of consistency evaluation of more products, manufacturing segment is expected to continuing growing at a high speed. Distribution business. Its revenue reached RMB66.25bn (+13.69% yoy) and GPM was 6.68% (+0.62ppt). The company continued to improve the layout of the national network, given it finishes acquisitions of distribution business in Jiangsu, Shanghai, Liaoning, Guizhou, Sichuan, Anhui, Hainan and other provinces, and promotes the sinking of sale channels to city level from province. It progress the integration of SPH and Cardinal, with a professional team of 63 people established. We see the realization of unified management system, and the preliminary combination in terms of DTP (direct high-value drug delivery) pharmacy business and contract sales. We highlight that distribution business still maintained double-digit growth under the influence of TIS is impressive. In 18H2, the growth of distribution business will accelerate given industry recovery.

Retail segment. Sales reached RMB3.13bn (+15.45% yoy) and GPM of 15.61%, down 0.39ppt yoy. It currently operates 1,981 retail drugstores (including 1,324 self-owned ones), 50 hospital pharmacies and 77 DTP pharmacies. SPH has actively participated in the Shanghai Community Comprehensive Reform Prescription Extension Program, thus it has covered 230 community hospitals and healthcare centers in Shanghai, with a market share of nearly 70%. In 18H1, the company has obtained more than 410,000 prescriptions, with prescription volume increasing by 115.4% yoy. SPH has facilitated the B-round fund of its healthcare e-commerce platform to further expand platform scale, which has processed more than 1.3mn electronic prescriptions and connected with more than 220 hospitals already.

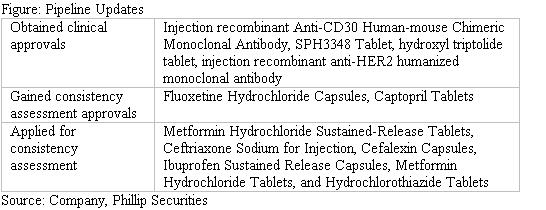

R&D updates. The company increased R&D investment, with an expenditure of RMB479mn (+28.29% yoy), accounting for 4.98% of manufacturing revenue. In 18H1, the company received six clinical approvals of innovative drugs, and promoted the consistency evaluation. It is expected to complete consistency evaluation of around 30 drugs by the end of 2018. At the same time, it focus on strengthening the R&D capability of bio-pharmaceuticals, with formally launching the San Diego R&D Center in US, and carrying out foreign cooperation and equity investment in bio-drugs, so as to enhance the overall innovation capability of bio-medicine.

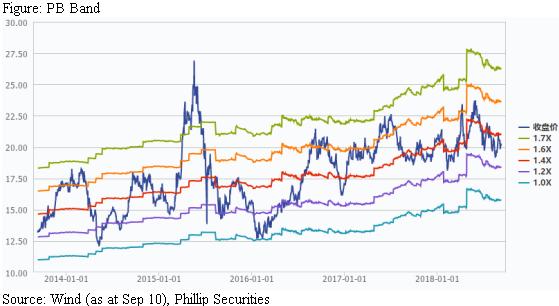

Valuation and RisksOur valuation model shows TP of HK$24.0. Based on target PE 14.25x and unchanged EPS forecast of RMB1.48, we get TP HK$24.0 (with assumption of Ex rate 0.875 RMB/HK$). Downside risks include: 1) Price reduction after inclusion in NDRL/PDRL; 2) Unfavorable progress in consistency evaluation ; 3) Policy risk.

Financials

Click Here for PDF format...

| Recommendation on 13-9-2018 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 20.100 | | Suggested purchase price | N/A | | Target Price | $ 24.000 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|