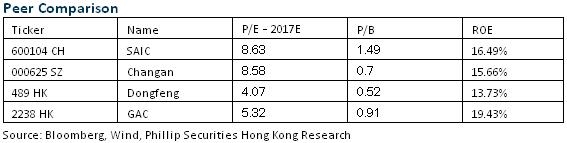

Investment Summary

SAIC's 2018H results still posted satisfactory growth at a high base and gained a steady rise in the gross margin, with a further enhancement market share. in H2, both self-owned brands and joint-venture brands will launch many new cars, thereby expecting to exceed the annual target driven by self-owned and joint-venture brands. Given the impetus of promising growth of self-owned brands, strong product cycle of joint-venture brands and the leading layout in emerging fields, the Company's overall result is expected to grow steadily, and meanwhile, the Company's high cash dividend rate is worth the wait. We maintain Accumulate rating. (Closing price as at 12 Sep 2018)

2018H result review

Earn nearly 20% in over half a year in 2018, and exhibit a steady rise in gross margin

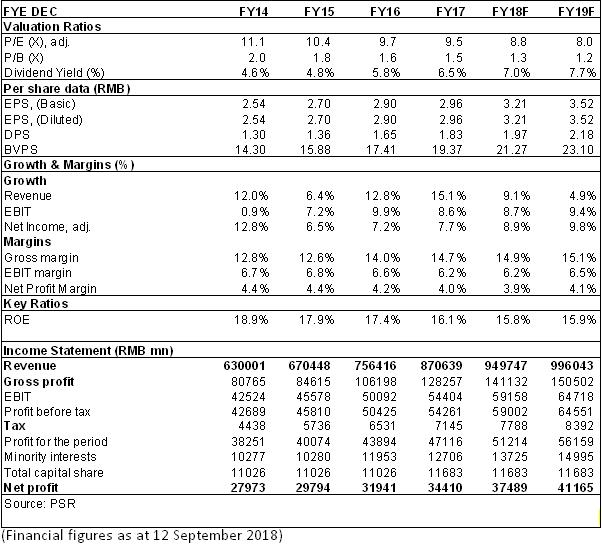

The 2018 semi-annual report of SAIC MOTOR showed that the revenue within the period reached RMB464,852 million, up 17.3% yoy; the net profit attributable to the parent company recorded RMB18,981 million, up 18.95% yoy; ROE registered 8.13%, up 0.54 percentage point; basic EPS was RMB1.625.If the non-recurrent profit and loss items are deducted, such as RMB918 million equity premium reported by the subsidiary HUAYU Automotive Systems arising from the consolidation of Skoito, the net profit attributable to parent company after deducting non-recurring gains and losses was RMB17,262 million, up 10.12%, suggesting that the Company's medium-term results still posted satisfactory growth at a high base.

In H1, the Company gained a steady rise in the gross margin, lifting by 0.29 percentage point yoy to 13.13%. In the second quarter, the R&D expenses climbed significantly, but asset impairment loss decreased. Thus, the net profit margin reached 5.85%, presenting a yoy increase of 0.23 percentage point. Besides, the sales expense rate and the administration expense rate stayed flat basically, and financial expense rate increased by 0.2 percentage point yoy along with a substantial rise of 535.3% in financial expenses caused by the growth of new loan interest paid.

Expansion of the leading edge, and further enhancement of the market share

In H1, the Company sold 3.52 million finished vehicles, with a yoy rise of 10.9% that surpassed the growth of the industry by 5.3 percentage points. Besides, the Company's market share bucked the trend of recession in vehicle market and witnessed a rise. The domestic market share arrived at 24.2% with a yoy rise of 1.2 percentage points, indicating the further expansion of the leading edge. Additionally, the Company registered the export and overseas sales of 130,000 finished vehicles with a yoy rise of 104%, continuing to rank first in finished vehicle export.

Specifically, sales volume of SAIC-Volkswagen/SAIC-GM/self-brand/SGM-Wuling increased by 5.2%/10.4%/53.7%/3.8% yoy to 1,020,000/960,000/360,000/1,050,000 vehicles, respectively. The Group's cumulative sales volume in H1 has already reached 49% of the annual target, suggesting strong probability to outperform the whole-year target; in H2, both self-owned brands and joint-venture brands will launch many new cars, thereby expecting to exceed the annual target driven by self-owned and joint-venture brands.

Brilliant performance of self-owned brands

In H1, the passenger vehicles of self-owned brands presented brilliant performance, with sales growth rate (+53.7%) leading the domestic mainstream passenger car enterprises, of which the internet vehicle types accounted for more than 40% of sales volume, and monthly sales of new energy passenger cars have surpassed 10,000 since May. The sales volume of new energy cars in the market outside Shanghai accounted for 60%, indicating more balanced market distribution. Financially, the self-owned brands achieved full-calibre (including R&D expenses) profit for the first time in the second quarter.

Increase in both prices and volume of joint-venture brands

Among joint-venture vehicle enterprises, both SAIC-Volkswagen and SAIC-GM recorded steady growth propelled by the strong product cycle, of which the effect of increase in both prices and volume arising from the upward shift of product mix of SVWSC was more notable. In H1, the revenue of SAIC-Volkswagen increased by 14.9% to RMB139.5 billion, and the net profit jumped by 17.5% to RMB15.47 billion. Benefiting from the increase in the proportion of high-end SUV vehicle sales, the prices and profits of single vehicles rose significantly. Besides, the revenue of SAIC-GM went up 8.5% to RMB111.9 billion, and the net profit grew by 9.5% yoy to RMB10.25 billion. Besides, the single vehicle price of SGM-Wuling lifted to some extent, and its revenue reached RMB51.5 billion with a rise of 4.7%, but the contribution to profit stayed flat at RMB2.06 billion.

What is worth mentioning is the field of new energy vehicles. In H1, the Company's self-owned and joint-venture new energy products were promoted, and 57,000 new energy passenger vehicles and new energy commercial vehicles were sold, up 275% yoy. The market share shot up strongly, and the medium- and high-end brand image was further consolidated and strengthened.

Accelerated implementation of the "new four modernization" strategy

The Company is fully pushing forward a new round of core technology innovation in new energy battery, motor, and electric control, and the business layout in core component systems, such as IGBT, ADAS, three electricity system, high precision electronic map for vehicle, V2X vehicular communication and intelligent driving decision control, has been activated. The MARVEL X vehicle type that will be launched in H2 will be equipped with autonomous parking and zebra smart 3.0 system by the end of the year. And in the field of shared travel, SAIC's new energy time-sharing leasing service has entered 62 cities across the country, with a membership of 2.75 million and more than 1,700 car-sharing stores.

Investment Thesis

Given the impetus of promising growth of self-owned brands, strong product cycle of joint-venture brands and the leading layout in emerging fields, the Company's overall result is expected to grow steadily, and meanwhile, the Company's high cash dividend rate is worth the wait. We adjust the profit forecast, giving the target price of RMB32.24, equivalent to 10/9.2x estimated P/E ratios in 2018/2019. The "Accumulate" rating is given.

Financials

Click Here for PDF format...