Investment Summary

Aier is a leading ophthalmic medical chain in China and even in the world. It operates more than 330 ophthalmic medical institutions worldwide, with total revenue amounting to RMB5.9bn and net profit reaching RMB790mn in 2017. We highlight that the company 1) expands through both horizontal extension and vertical sinking of hospital network, 2) increases employee motivation with equity incentive programs and vigorously cultivates medical talents, and 3) actively explores the international and mobile medical fields. We expect FY18E/19E revenue to achieve yoy growth of 35%/30%, and initiate 12-mon TP of RMB35.2 with target PE 50x, BUY rating. (Closing price at 18 Sep 2018)

Business Overview

Aier, established in 2003 was listed on Shenzhen Exchange in 2009 (300015SZ). By 2018, Aier has built more than 250 professional ophthalmic hospitals in over 30 Chinese provinces and cities, covering more than 70% of the national medical insurance population and serving over 6.5 million outpatients annually. The company is committed to the parallel introduction and absorption of world-leading ophthalmic technology and management concepts, with professionalism, scale and science as its strategy. Aier has bridged all three areas of medicine, education and research, the establishment of these educational and research institutions is expected to boost research and clinical standards. Also, the company focuses on international development, given it operates more than 80 ophthalmic medical institutions in US, Europe and Hong Kong through investment holding.

Special hierarchical chain management model.

The company runs professional ophthalmic chain medical institutions, mainly engaged in the diagnosis and treatment of various ophthalmic diseases, surgical services and medical optometry glasses. Given the superior hospitals give technical support to lower-tier hospitals, and the difficult patients in lower-tier hospitals can be referred to superior ones, this mode is expected to realize the optimization of resource allocation and offer convenience to patients. Hospitals with different function and responsibility, facilitate to improve the efficiency of resource sharing and optimize management system. We believe that the advantages of the mode will be further demonstrated after accelerated expansion and penetration of hospital network.

Increasing outpatient visits and ophthalmic surgeries.

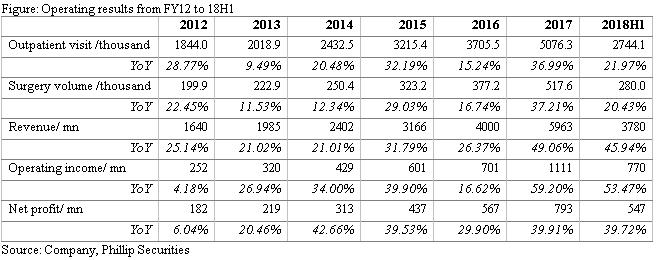

From 2012 to 2017, we see the numbers of outpatient visits and ophthalmic surgeries continuously increased, with 5y CAGR of 22.5%/21% respectively. In 2017, the number of outpatients exceeded 5mn, and ophthalmic surgery volume reached nearly 520,000 times. Accordingly, its topline/operating profit/net profit all achieved 5y CAGR of over 30%, given FY17 revenue/operating profit/net profit reached RMB5.96bn/1.11bn/790mn, respectively representing yoy growth of 49%/59%/40%. As the penetration of hospital coverage increases and the citizens` demand for ophthalmic treatment hikes, we expect that escalated outpatient visits and surgery volume will drive revenue further growing.

Rapid expansion leveraging on capital advantage.

The company has continuously invested in expanding hospital network with its own funds, cooperation with industrial funds or non-public fund-raising. Back to 2009 when it was listed, Aier only owned 18 ophthalmic hospitals in Mainland China. Now the company has developed 250 ophthalmic hospitals in China and more than 80 ophthalmic institutions abroad, rapidly horizontally expanding. Since 2014, the company has explored the cooperation with the M&A fund of medical industry, and three professional funds have been established (深圳前海東方愛爾醫療服務產業並購基金、華泰瑞聯並購基金以及愛爾中鈺眼科醫療產業並購基金). The cooperation has deepened the vertical network and improve hospital penetration, given it dramatically speeds up the development of city-level and county-level hospitals. The project fund also invests in and cultivates potential hospital targets, which guarantees for the sustainable development of the company. In 2017, through non-public offering, the company raised RMB1.72bn for hospital acquisition and construction. Meanwhile, Aier is engaged to construct a hierarchical diagnosis and treatment system in city, and develop eye care centers (clinics) and community eye health services, further sinking services to lower-tier channel.

Developing mobile medical system.

In 2016, the company released a scheme about Ophthalmology Mobile Medical Development and Implementation Progress, which specifies that leveraging on its national hierarchical hospital chain, the company aims to build an eye health guarantee system, which involving online and offline channels, disease prevention and treatment, hospitals and out-of-hospital institutions. One of its invested firms has laid out a number of community centers offering eye health services in Changsha, Tianjin, and Chengdu, which involve online platform and off-line service providers.

Facilitating international development.

Currently, the company owns overseas ophthalmic institutions such as Hong Kong Asia Medical Service, MINGWANG Ophthalmology Center in US, and Clnica Baviera.S.A. in Europe, which will help to effectively integrate the advanced international medical service concepts and cutting-edge technical systems, as well as high-end service models and management experience for Aier. On the one hand, the company takes advantage of the international network to strengthen the international interactions, and promotes the growth of high-end medical services. On the other hand, through the Global Science and Technology Innovation Incubation Fund, the company invests in innovative projects in ophthalmology and related cutting-edge fields, to enrich its potential investment project reserve.

Science and education research platform for training talents.

The talent training system is maturing and talent introduction system has become a healthy circle. The company has set up an integrated platform involving teaching, research and training, cooperated with several quality Chinese universities to set up ophthalmology academies and research institutes, and established 9 academic groups for different diseases including cataract, optometry, refraction and fundus, which promotes the transformation from research results to real products, and improves the company's innovation ability and drive business development. Meanwhile, the company provides attractive compensation to appeal intelligent talents and experts from outside to enhance the technical strength.

Increasing demand and upgrading consumption in China.

The modern lifestyle with lots of pressure from learning, work, and entertainment, leads to a rising prevalence of various eye diseases. At the same time, eye diseases, such as cataracts and diabetic retinopathy, emerges more often as the aging of the population, which puts higher demands on eye medical services. In the case of cataracts, which is more common in people over 50 years old, the incidence increases with age. According to a government research (中國人口老齡化發展趨勢預測研究報告), China's population over 60 years old will exceed 400mn in 2050E. So we predict that the number of age-related eye diseases such as cataracts will show a long-term growing trend. With the gradual popularization of eye health knowledge and enhanced eye protection concepts, the demand for eye care services is expected to continue increasing. Also, as the residents` income level goes up, people are more willing to pay for eye healthcare and mid- to high-end services will become more affordable for them. We expect that the market will continue to expand under the combined effect of improving demand and consumption upgrades.

Investment Thesis, Valuation & Risk

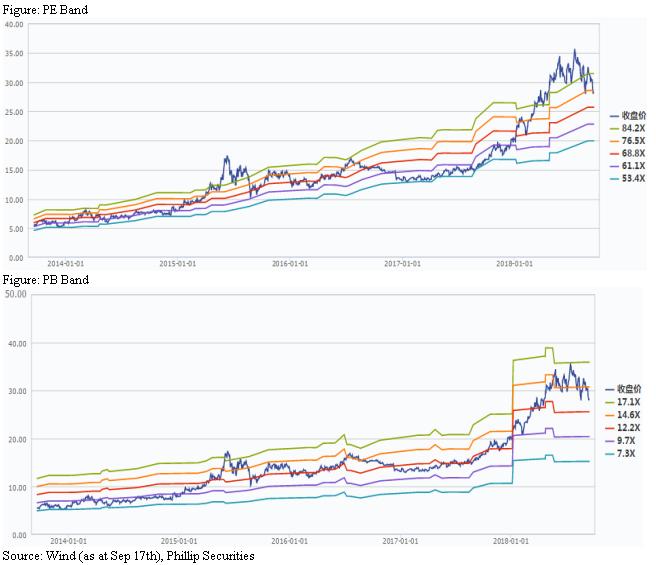

Our model initiate TP of RMB35.2. Benefiting from the expanding hospital network and the endogenous growth of existing hospitals, we predict that revenue growth will reach 35%/30% in FY18E/19E. Assuming that profit margins remain relatively stable, we expect EPS to be RMB0.53/0.70 in FY18E/19E. With target PE 50x, we give 12-months target price of RMB35.2. Risks include: Rising sales costs; Rapid expansion of hospital networks leads to reduced management efficiency; Sluggish market demand.

Financials

Click Here for PDF format...