Investment Summary

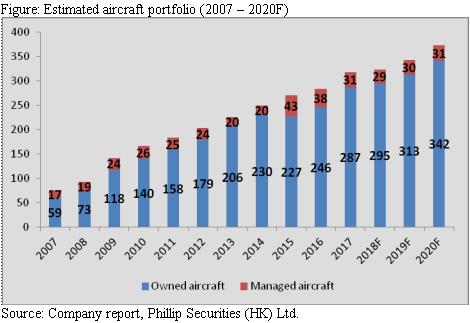

BOC aviation (BOCA) is a leading global aircraft operating leasing company in Asia, currently with a portfolio of 295 owned and 29 managed aircrafts. We initiate an “Accumulate” rating based on a Price-to-book ratio vs. Return on Equity method, deriving a target price of HK$70.5, 14.5% potential upside. (Closing price at 21 September 2018)

Advantage on low funding cost

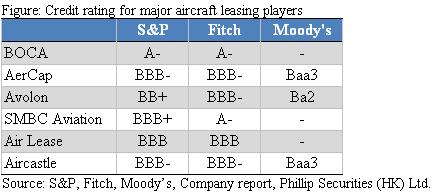

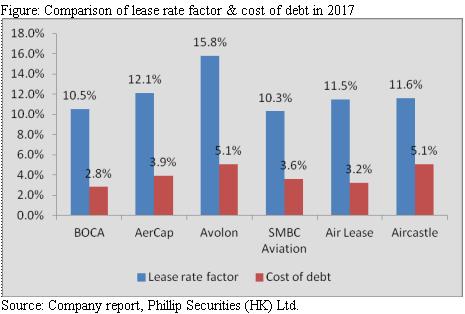

Supported by the parent company – Bank of China, and its financial strength, BOCA enjoyed a lower-than-peers funding cost, only 2.8% in 2017. Moreover, BOCA was rated as A- by Standard & Poor's and Fitch, above almost all its peers, which justify a cheaper funding cost than peers. A low funding cost allows lower lease rate to airline customers, thereby offering a more competitive package than other major competitors.

Rich order book on hand

BOCA has a total of 171 aircrafts on order, accounting for 34.5% of its air portfolio. It also means 44 aircrafts will be delivered for the next three years on average, providing a source of growth for the future. Besides, the aircraft models on order were believed to be cutting-edge, such as A320NEO, A330NEO, Boeing 737 MAX, and 787 family. A popular aircraft model ensures the possibility of leasing out the aircrafts in a short period.

Strong demand for aircrafts upcoming

The emerging middle class and low cost carriers (LCCs) enhance the propensity to travel. It is expected the revenue passenger kilometer (RPK) to double every ten years, and to be resilient after the crisis. From 2017 to 2037, it is predicted 42,730 new aircrafts to be delivered either for growth or replacement.

Remarkable interim results

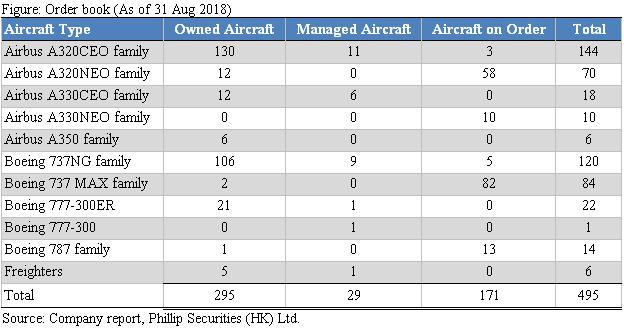

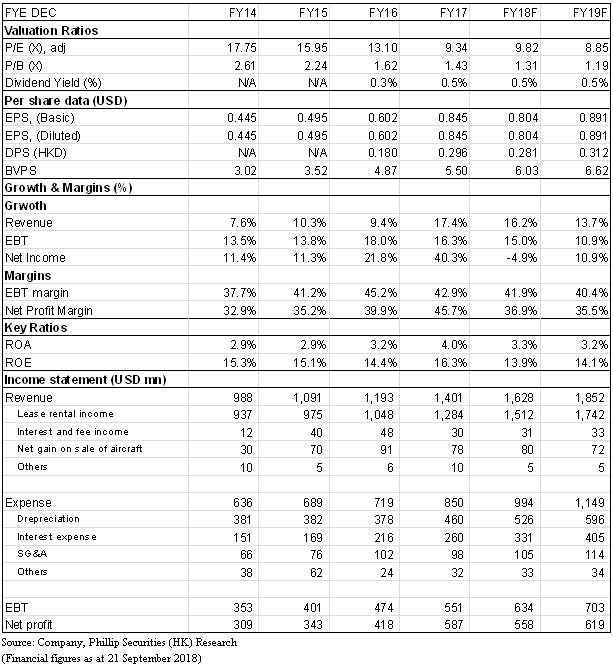

The revenue and net profit reached US$824 and $297 million, up 23% and 24% respectively. The interim dividend was US$0.1284 per share, implying a 30% payout ratio. The aircraft portfolio reached 495 as of 31 Aug 2018. The lease rate factor and cost of debts was 10.5% and 3.1%, deriving an 8.5% net lease yield.

Company profile

Founded in 1993 as Singapore Aircraft Leasing Enterprise (SALE), BOC Aviation (BOCA) is a leading global aircraft operating leasing company headquartered in Singapore. In 2006, BOCA was acquired by Bank of China (3988.HK) for US$965m, and renamed “BOC Aviation” in 2007. In 2016, BOCA was listed on the Main Board of the Stock Exchange of Hong Kong, raising HK$4,246m in primary proceeds. With a portfolio of 295 owned and 29 managed aircrafts, BOCA ranked 7th in terms of both fleet value and fleet size in 2017, according to Flight Ascend. It serves 88 airlines in 35 countries and regions, and is one of the global aircraft leasing companies with the youngest age of aircrafts (3.0 years) and longest remaining lease term (8.3).

Business model

BOCA's model is relatively simple, where it first acquires aircraft either from order book aircraft purchases or purchase and leaseback from airlines. Then, it leases the aircraft to airlines on long-term contracts, typically 10 to 12 years. Around half way through the lease, BOCA sell the aircrafts with leases attached to other investors, such as other aircrafts leasing company, airlines and financial investors, and reinvest the proceeds in new aircrafts. All the leases of BOCA are operating lease, accounting for around 90% of the total revenue, and dry leases, meaning no crews are provided in the lease from BOCA. During the leases, airline customers are responsible for the maintenance, with some lessees required to pay maintenance reserves to BOCA.

Industry analysis

Emerging middle class and low cost carriers enhances the propensity to travel, in turn boosting the demand for aircrafts

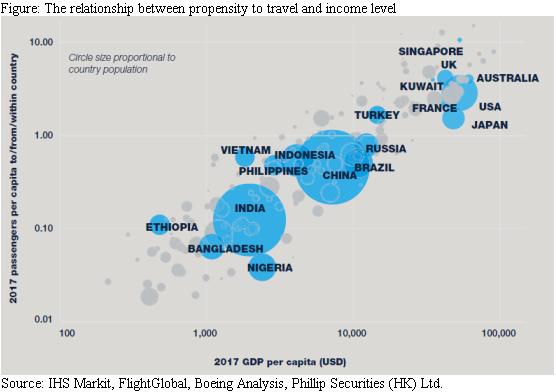

The propensity to travel determines the demand for airline services, which in turn makes up the demand for new aircraft from airlines. According to Boeing analysis, the propensity to travel indeed positively correlated with income levels. Thus, the burgeoning growth in middle class could edges up the propensity to travel, eventually driving up the revenue passenger kilometer (RPK). It is expected the number of middle class will rise by 69.2% in 2037, accounting for 56% of the total population. Africa will enjoy the most significant growth in 2037, about 144% increase, while Asia-Pacific will have the largest number of middle class in 2037, reaching 2.811 billion.

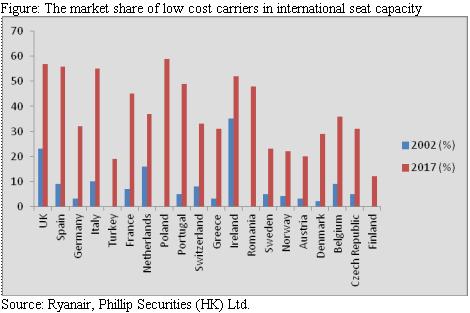

Asides the presence on middle class, the emerging in low cost carriers (LCCs) also creates higher propensity to travel, thanks to the affordable airline fare. According to Ryanair airline, the market share in international seat capacity of LCCs in Europe rises from 10% in 2002 to 42% in 2017. The market share of LCCs in UK, Spain, Italy, Poland, and Ireland even exceeds 50%. An affordable airline fare lowers the threshold of travelling, leading to traffic growth. Eventually, the demand for aircrafts is fueled by the stronger traffic growth.

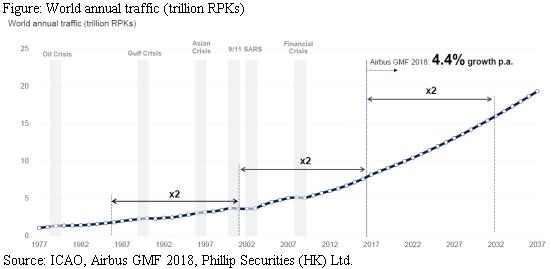

According to estimate from Airbus, the RPKs, a metric that is usually used to measure the traffic, is expected to double in 2032, with 4.4% growth p.a. Apart from the traffic growth, the RPKs have shown its resilience to external shocks, including 9/11, SARS, and 2008 financial crisis. Thanks to the gradual rise in traffic, the airlines are required to expand its fleet size to keep up with the upcoming demand, edging up the number of fleet. Boeing estimates the total number of fleet will reach 48,540 in 2037 from 24,400 in 2017. Added up the replacement, the total new fleet will be 42,730, around 2,100 new aircraft every year on average. The demand for new aircraft will underpin the aircraft leasing.

Competitive advantage

Low cost of funds facilitates attractive lease rate

Thanks to the support from parent company – Bank of China, and its strong financial condition, BOCA was graded as A- from both Standard & Poor's and Fitch, which was well-above its peers. Leaning on its superb credit rating and its mix of fixed and floating rate financing, BOCA enjoyed a lower cost of funds than its peers, which have a funding cost ranging from 3.2% to 5.1%. The cheaper fund allows BOCA to maintain a stable net lease yield, and operating margin. We believe the lease rate is the most crucial factor for airline customers when there are more than one aircraft leasing operators in the market that could offer them the aircraft they want, as the aircraft with same model will not provide too many differentiations. As a result, the relatively low lease rate, supported by low cost of funds, could make BOCA more competitive in terms of price in the rivalry. The lease rate factor of BOCA is lower than its major competitors, such as Aercap, Avolon, Air Lease, and etc., around 10.5% in 2017. We expect the relatively low lease rate will remain the key competitive edge in the future when competing with major players.

Rich order book with popular aircraft backlog provides certainty in the future

The source of aircraft is mainly from two, 1) order book and 2) purchase and leaseback. The growth on lease revenue mainly relies on the number of new leases, which will require lessors to have enough aircrafts to enter a lease with airlines. As of 31 Aug, BOCA owned a portfolio of 495 owned, managed and committed aircraft, in which 295 of them are owned. And, 34.5% of aircrafts have been ordered and will be delivered in next few years. On average, 44 aircrafts will be delivered in next three years. Thus, a rich order book provides better certainty on growth by ensuring the source of aircrafts in next few years.

Apart from the rich order book, a popular aircraft model is also needed in order to attract airline customers. BOCA strived to acquire the most popular aircraft model in the market, such as Airbus A320NEO, A330NEO, Boeing 737 MAX, and 787 family. Most of them are equipped with new technology, for example, Airbus A320neo family is believed to be 15% more fuel efficient and Airbus A330neo family promises 14% better fuel economy per seat. Aside the new technology, the aircraft type also determine the demand. As the surge of low cost carriers which prefer narrow-body aircraft, we forecast the demand for narrow-body aircraft will outstrip that for wide-body aircrafts. 87% of aircrafts in delivery are narrow-body, so we are positive that the aircraft backlog will be able to lease out once they are about to be delivered.

Young fleet and lengthy remaining lease term

BOCA is one of the companies which have the youngest fleet age and the longest remaining lease term. The long remaining lease term ensure the lease revenue for next few years, as there is no early termination for lease contract, meaning the lease revenue should be very stable in the future, unless its airline customers go bankrupt. Besides, the lease expiries are well-dispersed during next few years, which the percentage of aircraft NBV with leases expiring from 2019 to 2023 is between 2.2% and 6.4%, and 79.8% of lease will expire in 2024 and beyond. Thus, we should see no significant impact on lease revenue in a single year due to the lease expiry.

Diversified customer bases together with credit analysis team

BOCA serves 88 airlines in 35 countries and regions, in attempt to make its customer portfolio diversified. Based on the NBV of the fleet, in 2018, 52% of the fleet was leased to airlines in Asia Pacific, 25% in Europe, 13% in Middle East as well as Africa, and 11% in America. With a more diversified customer bases, it effectively reduces the credit risk on BOCA's lease portfolio. In addition to a diversified customer mix, BOCA generally requires its customers to have at least 20 aircrafts, securing the quality of its clients` financial condition. Moreover, BOCA also has its own research team in an effort to monitor the financial health of its clients by evaluating their credit score. We believe BOCA has effectively mitigated its exposure to credit risk by those means.

Matching lease and debt sensitivity to mitigate interest rate risk

As the interest rate is hiking since 2015, airlines tended to enter a lease contract by fixed rate. In order to match the lease and debt sensitivity, BOCA lifted the proportion of its fixed rate debts from 14% in 2013 to 56% in 1H18. Therefore, although the cost of debt for BOCA has also been rising since 2015, BOCA is able to maintain its net lease yield above 8%. Furthermore, BOCA hedged 70% of its mismatched interest rate exposure, and expected the net profit to be reduced US$1.8 million if a 25 basis points increase based on the balance as at 30 June 2018. We believe interest rate risk has been closely monitored by BOCA, resulting in no significant influence in the Interest rate hike cycle.

Earnings forecast

We expect to see a net increase of 18/29/21 in 2018F/19F/20F for its owned aircrafts, with a slight rise in managed aircraft, reaching a total of 324/343/373 aircrafts in 2018F/19F/20F respectively. Besides, we believe the lease rate factor and cost of debt will be driven up in next few years due to an interest rate hike cycle. Mitigating the rising cost of debt by lifting its lease rate factor, BOCA is able to immune itself from eroding its net lease yield, maintaining around 8.3% - 8.5%.

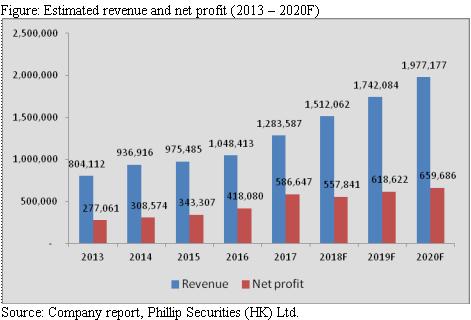

We forecast the growth of revenue to be 17.8%/15.2%/13.5% in 2018F/19F/20F thanks to both rising fleet size and lease rate factor. Meanwhile, the growth of net profit is expected to be 12.5% (excluding the tax adjustment benefit in 2017) /10.9%/6.6% in 2018F/19F/20F.

We also predict the proportion of interest expense to reach 33%/35%/36% because of an increase in financial leverage, making that of depreciation, SG&A and other expenses driven down. However, the depreciation cost remains the major cost among the operating cost.

Valuation

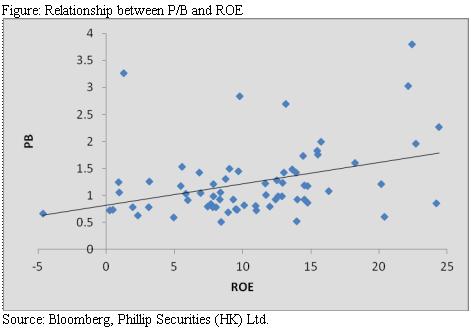

We adopted the Price-to-book ratio vs. Return on Equity framework (P/B-ROE) for our valuation. We investigate the relationship between P/B and ROE for Aercap (AER.US), Air Lease (AL.US), Aircastle (AYR.US), China Aircraft Leasing Group (1848.HK), CDB Leasing (1606.HK), and etc. According to the results and our estimate on ROE, we derive our target price to be HK$70.5 based on the NAV in 2019F, implying P/B 1.50x/1.36x/1.25x in 2018/19/20F respectively and giving an “accumulate” rating. We believe the competitive advantages, such as low cost of funds, rich order book, and diversified customer base could justify a relatively high valuation. (HKD/USD: 7.8)

Risk

1. Higher-than-expected increase in interest rate

2. The demand for traveling and aircrafts slow down

3. Delayed aircrafts deliveries

4. Depreciating value for aircrafts in secondary markets

Financials

Click Here for PDF format...