|

|

|

*Advertisement* |

|

|

|

|

|

28 Sep, 2018 (Friday) |

NANFANG COMM(1617)

Analysis:

Nanfang Communication Holdings (1617) is principally engaged in the manufacture and sales of optical fibre cables. In 2017, the Group established a joint venture company for the manufacturing of optical fibre preforms with its partner and reached the principal of the optical fibre cable production chain. After the joint venture company is put into production, the Group`s raw material supply is expected to be secured. This alignment of the complete industry chain will enhance the gross profit margin and competitiveness of the Group. Additionally, the Group will strive to identify qualified optical fibre suppliers to stabilize the supply of optical fibre and explore for upstream development or acquisition of the optical fibre and cable production value chain. This will improve the utilization of the production capacity of the Group. (I do not hold the above stock)

Strategy:

Buy-in Price: $5.00, Target Price: $5.50, Cut Loss Price: $4.65

|

|

CHINA GAS HOLD(384)

Analysis:

The company is China`s largest gas operators, mainly engaged in investment, construction, operation of urban and township gas pipeline infrastructure, supply of natural gas and liquefied petroleum gas to residents and industrial users, as well as the construction and operation of compressed natural gas/ liquefied natural gas filling stations. It serves for over 6mn users covering 19 provinces in China. Over last fiscal year, gas sales volume grew 52.6% yoy to 18,659.3mn cubic meters, and the number of new residential users reached 3.9mn, up by 53.1% yoy. Topline grew by 65.1% yoy to HK$52,831.96mn, gross profit was up by 39.3% yoy to HK$11,671.02mn, and profit attributable to shareholders was up by 47.0% yoy to HK$6,095.15mn. In August, the company signed a strategic cooperation agreement with Shandong Luxin to invest RMB800mn in 41% of Shandong Petroleum and Natural Gas. This will facilitates the company to control the main incremental gas sources and core storage and transportation capacity of Shandong natural gas market in future, expand source supply and terminal coverage in Shandong, and help promote the gas project there.

Strategy:

Buy-in Price: $22.75, Target Price: $30.00, Cut Loss Price: $18.00

|

| |

|

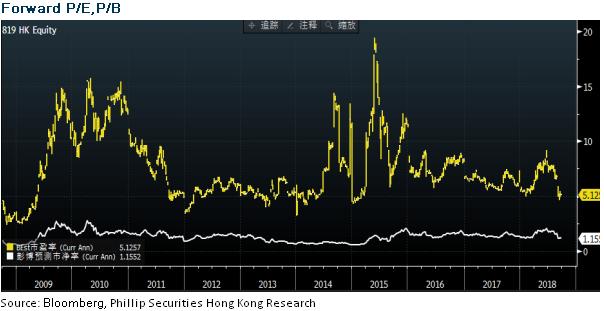

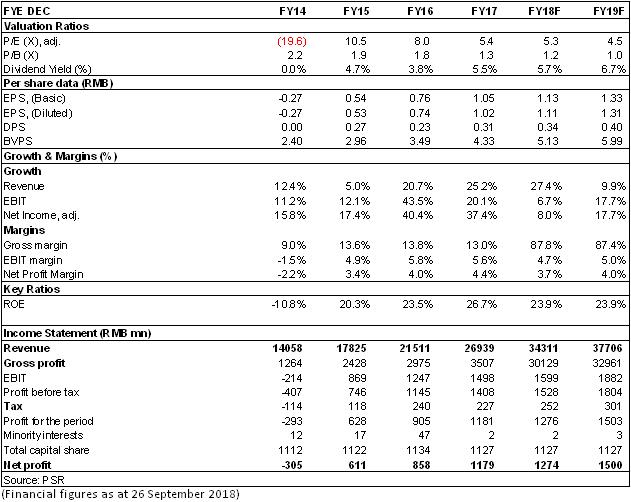

Tianneng (819.HK) - 2018H results slightly lower than expected, cut target price but maintain Buy rating

Investment SummaryTianneng Power's 2018H1 revenue and net profit increased by 28% and 16%, respectively, but the gross profit margin declined slightly. The lead battery business was better than expected, but the correction of the lithium battery business dragged down the company's net profit growth slightly lower than expected. We adjust our EPS forecast for 2018/2019 to 1.13/1.33 yuan. We believe that the current market is too pessimistic about the company, after its stock price retraced more than half from the high point. The current valuation does not reflect the company's leading position in domestic lead-acid battery market. For valuation we cut our target price to HK$8.4 to reflect the possible challenge of the company, but maintain a Buy rating. (Closing price as at 26 Sept 2018) 16% More Revenue in the Middle of the PeriodTianneng Power recorded a revenue of RMB14,507 million in the first half of 2018 with a net profit of RMB534 million, an increase of 27.7% and 15.8%, respectively, compared with those of 2017. The operational cash flow was around RMB1,159 million. The EPS was RMB0.44. The gross profit was RMB1,709 million with a gross margin of 11.8% during the period. Compared with that of the same period of 2017, there was an increase of 18.8% and a fall of around 0.9 percentage point, respectively. The main reason why the gross margin dropped was the rise of the price of lead, a main raw material. A Prominent Growth in Lead-acid BatteryAs the traditional main business, the lead-acid battery sector has been providing stable cash flow for the company. The integration-based bonus in the industry was further released and the revenue from the lead-acid battery was as high as RMB13,313 million, a yoy increase of 31.7%, accounting for 91.8% of the total sales. Among others, the sales of lead-acid battery used in electrical bicycles/tricycles increased by 31.8% to RMB12,178 million yoy. The revenue from the special-purpose battery went up by 30.2% to RMB1.14 billion yoy. The company further enhanced its leading position in this field with a steady expansion of market shares. Adjustment is Made in the Lithium BatteryThe revenue from the lithium battery was RMB278 million, a fall of 39.0% yoy, accounting for 1.9% of the total sales. Affected by the reduction of the national subsidy policy, the lithium battery industry is going through an adjusting period. From the perspective of prudent operation, the company decided to select its customers and shrink its production lines for the moment. The total effective productivity is around 2.5GWh with a capacity utilization rate of about 50%. We believe that the company's lithium battery segment will go through a period of adjustment for technology & clients reserve. The Rapid Growth of Recycled LeadThe sales revenue from the recycled lead was RMB745 million, an increase of 36.0% yoy, accounting for about 5.1% of the total sales revenue. During the reporting period, with an annual processing capacity of 400,000 tonnes of used batteries, the company processed 120,000 tonnes, in which 66,000 tonnes were undergoing a recollection period and would enter the internal recycling afterwards. By recycling, RMB125 million can be saved in terms of material costs. The company plans to actively expand the layout recycling productivity, including building new bases or expanding the existing ones. In the case of building new bases, the company will follow the rules of local provincial governments for granting licenses. Investment ThesisTianneng Power is a leading enterprise in China's lead-acid power battery industry. We believe that the Company's lead-acid battery business will continue to maintain its stable growth characteristics and become the Company's ※cash cow§ business. Its recycle business is expected to become a new profit growth point. While its lithium battery business will go through an adjusting period. We expect the company's EPS for 2018/2019 to reach 1.13/1.33 yuan and the target price of HK$8.4, corresponding to 2018/2019 6.5/5.6x P/E. We maintain a Buy rating.

Financials

Click Here for PDF format...

| Recommendation on 28-9-2018 | | Recommendation | BUY | | Price on Recommendation Date | $ 6.810 | | Suggested purchase price | N/A | | Target Price | $ 8.400 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|