Investment Summary

Mengniu's interim revenue increased 17% y.o.y. to RMB34.474 billion. Gross profit margin(GPM) increased 3.6ppt y.o.y to 39.2%. Operating profit margin fell 0.5ppt y.o.y. to 5.6%, mainly due to the sponsorship of World Cup. Net profit increased 38.5% y.o.y. to RMB1.56 billion.

Facing the economic slowdown in China, the management team still raised its full-year growth target from the previous low double digit to the medium double digit and revealed that the business performance from July to August was in line with expectations. Facing the risk of competitors launching promotions or increasing discounts, it emphasizes that it will respond to price wars through increasing innovation capabilities and brand investment.

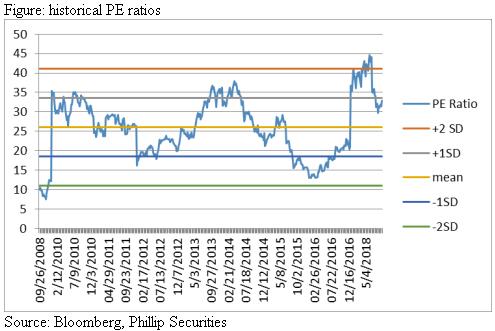

We believe that the dairy industry in China is with rigid demand and the impact from economic slowdown is limited. The double-digit growth target for the whole year is still able to meet. We believe that the recovery of raw milk prices in 2H will help its material associate China Modern Dairy (1117) to further reduce its loss. Sales and distribution expenses are expected to be lower than 1H. We maintain a forecast PE of 31 times and target price of HKD28.5. (current price as of 27th September, 2018)

Business/Industry Overview

-Its interim revenue increased 17% y.o.y. to RMB34.474 billion, of which 7% came from sales volume growth, and more (10%) came from the increase in ASP, driven by the improvement in product portfolio, and decrease in discount rate. Gross profit margin(GPM) increased 3.6ppt y.o.y to 39.2%.

- In terms of GPM, the stable raw milk procurement cost coupled with the higher growth rate of the high-margin Deluxe, room-temperature yogurt and milk powder, led to the increase in overall GPM. The management stated that the high GPM in 1H of the year was sustainable and that it could be maintained throughout the year and next year. The raw milk price in 2H is expected to be higher than 1H due to seasonal reasons, but it is believed that it will be at reasonable and controllable level. The annual raw milk price is expected to be flat y.o.y.

We believe that the recovery of raw milk prices in 2H will help its material associate China Modern Dairy to further reduce its loss. From the past performance, Mengniu's GPM is usually lower in 2H than 1H, we expect the same thing will happen for this year. But as considering the improvement of the overall product mix, and higher number of high-margin new products (40 SKUs), GPM for the whole year is expected to be higher than last year.

- Operating profit margin in 1H fell 0.5ppt y.o.y. to 5.6%, mainly due to the sponsorship of World Cup during the period which involved RMB800 million. Selling and distribution ratio including advertising and promotion expenses recorded an increase of 4.7ppt y.o.y to 28.9%. However, benefiting from the reduction of loss of China Modern Dairy, the increase in interest income and the decline in effective tax rate, the net profit increased 38.5% y.o.y. to RMB1.56 billion. The net profit margin improved 0.7ppt. to 4.5%.

The management team expects that the operating profit margin for the whole year will be flat or slightly lower y.o.y, with the latter being more likely. It states that the investment in branding is long-term. The overall sales and distribution expenses will be higher in the future than in previous years.

The management team aims Yashili International (1230) turnaround this year and same as ice cream business, the latter with a double-digit growth in revenue.

-Mengniu's new businesses include fresh milk, cheese, vegetable milk and overseas markets. The management said that the new business has growth potential, and some categories may have surprises in the next one to two years. Among the new businesses, the fresh milk business which in cooperation with China Modern Dairy is a long-term strategy, it is mainly focused on high-end fresh milk products. During 1H, it launched two new fresh milk products, namely Shiny Meadow and Greenhouse. The management team expects this business will grow faster than Mengniu Group. Currently, the business has been laid out in key cities in East China, South China, Central China and North China.

In terms of overseas markets, there will be further layout this year, especially in Southeast Asia. The new Indonesian plant is expected to be commissioned in the fourth quarter this year, mainly to fulfill local and surrounding market demand. Apart from selling in overseas markets such as Hong Kong, Macau, Myanmar and Cambodia, it also explored the Australian market during the period with ice cream products as its chariot. Mengniu expects to enter new markets – Malaysia and the Philippines within this year.

In 1H of the year, new product sales accounted for 26% of the low temperature business, while the normal temperature business accounted for 9 to 10%. Among the 40 SKUs this year, room-temperature yogurt accounts for 6 to 7 SKUs. In 1H, room-temperature yogurt recorded over 30% increase in revenue. We are optimistic on the sales growth of room-temperature yogurt in the next couple of years.

In terms of channel expansion, the proportion of traditional channels such as small and medium-sized supermarkets is declining, and the proportion of e-commerce and convenience stores is rising. Emerging channels include micro-business, campus, food and beverage outlets, hotels, parks, cinemas, etc. Management also expects that there will be strong growth in the future for unmanned retail outlets.

And its B2B e-commerce platform, including retail (Ali) and Huishang (Tencent), will help increase penetration in lower-tier cities (townships). The e-commerce business currently accounts for 3% of the total, mainly focusing on the sale of imported dairy products. The management plans to promote the integration strategy of e-commerce and emerging channels from research and development to marketing.

Valuation and risk

We are optimistic about the industry and the company's prospects, thus maintain forecast PE ratio of 31 times and target price of HKD28.5.

We believe that the target of mid-double-digit growth target for the whole year is still able to meet. We believe that the recovery of raw milk prices in 2H will help its material associate China Modern Dairy (1117) to further reduce its loss. Sales and distribution expenses are expected to be lower than 1H.

Potential risks include failure to meet revenue growth, lower profit margins than expected, and huge fluctuations in raw milk prices. (current price as of 27th September 2018)

Financials

Click Here for PDF format...