|

|

|

*Advertisement* |

|

|

|

|

|

3 Oct, 2018 (Wednesday) |

SHENZHEN INT`L(152)

Analysis:

Shenzhen International Holdings (152) announced that China Vanke will become the strategic investor of its subsidiary, United Land Company, by way of capital injection which will further enhance the Group`s confidence in developing large-scale comprehensive property projects, quality of project management and overall return of the project. United Land Company holds the land use rights of the land parcels of the Meilin Checkpoint Urban Renewal Project of the Group and is engaged in developing the project. The project is adjacent to the Futian District in downtown Shenzhen and has been redesigned as a comprehensive development project with a total gross floor area of approximately 486,000 square metres, comprising properties for residential, commercial, office, business apartment and public ancillary uses. The fair value of the properties to be constructed under the project is expected to be over RMB10 billion. (I do not hold the above stock)

Strategy:

Buy-in Price: $15.80, Target Price: $17.40, Cut Loss Price: $15.00

|

|

LIFESTYLE INT`L(1212)

Analysis:

The company completed disposal of its entire 59.56% stake in Lifestyle Properties on 13th April 2017. It becomes a retail operator that specializes in the operation of mid to upper-end department stores in Hong Kong. Its two SOGO stores in Hong Kong including the flagship store in Causeway Bay (SOGO CWB), one of the largest and leading department stores in Hong Kong, as well as the Tsim Sha Tsui store (SOGO TST). There is Kai Tak project which is under construction currently. The company aims to complete the foundation construction work in 2019. The company`s department store operations saw its turnover increased by 26.2% over the same period last year. The strong growth in turnover was mainly attributable to the increase in direct sales and commission income derived from APO sales and concessionaire sales. As the former is with lower gross profit margin, the overall gross profit margin dropped 1.2ppt. to 73.7%. EBITDA for the period increased 25.2% to HK$1285.2 million. Regarding the outlook for the retail market in the second half of the year, the management said that although there are many uncertainties, including the Sino-US trade dispute, but according to the company`s performance during July to August, they remain optimistic. The impact of RMB depreciation on the consumer market has not seen much. Tsim Sha Tsui store, which is mainly based on mainland customers, can still maintain double-digit growth from July to August. In addition, the opening of the high-speed rail and the Hong Kong-Zhuhai-Macao Bridge is expected to bring more tourists.

Strategy:

Buy-in Price: $15.20, Target Price: $17.20, Cut Loss Price: $14.50

|

| |

|

Report Review of September 2018

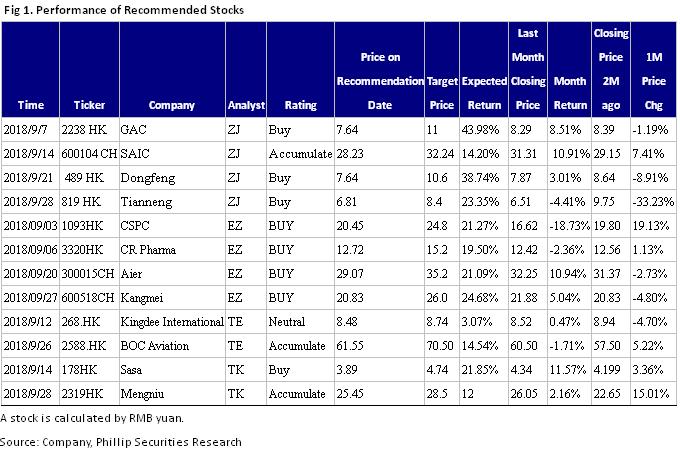

Sectors: Air, Automobiles (ZhangJing) Healthcare, TMT (Eurus Zhou) TMT, Education (Terry Li) Retail, Property (Tracy Ku) Automobile & Air (ZhangJing)This month I released 4 updated reports of GAC (2238 HK), SAIC (600104 CH), Dongfeng Group (489 HK) and Tianneng Power (819 HK), which got success by their unique Competitive edge.In 2018H1, Dongfeng reported a basically unchanged revenue, with better-than-expected EPS of RMB0.9364, representing a yoy increase of 14.9%. Sales expenses and financial costs decreased due to the lower advertising fee and exchange profit respectively. We expect Dongfeng Honda is recovering gradually in H2 and DFNissan's capacity expansion planning is also about to be put on the agenda. Overall, we expect the Company's result will maintain steady. In accordance with the latest data, we adjust the company's EPS forecast, and target price to HKD10.6. The "Buy" rating is given.GAC's 2018H1 results were in line with expectations, and sales in July/August 2018 recovered well. It is expected that the Company will maintain steady growth this year under the strong product cycle of the joint venture car companies. We revised the Company's 2018 earnings forecast and introduce the predicted value of 2019. We reaffirm the "Buy" rating with the target price to HKD 11.. Healthcare & TMT (Eurus Zhou)This month I released 4 equity reports, including CSPC (1093HK), CR Pharma (3320HK), Aier Eye Hospital (300015CH) and Kangmei (600518CH). We tend to highly recommend CR Pharma (3320HK). We tend to highly recommend CR Pharma (3320HK). 18H1 revenue recorded HKD93.7bn up by 13.3%. Gross profit reached HKD16.88bn up by 34.7% with GPM rising by 1ppt, which is mainly due to increasing shares of direct sales to medical institutions. We expect that after the effects of two invoice system fade in 18H2, the distribution business will further rebound. The company implements a number of M&A projects in the field of traditional Chinese medicine and chemical medicine treatment to enrich product mix and expand business layout. We expect Matthew effect in future competition, and the strong will always be strong. The company will continue to maintain its leading position in industry. TMT & Education (Terry Li)I released two reports including China Maple Leaf Education (1317.HK) and Wisdom Education (6068.HK). We highly recommend Wisdom Education. Wisdom is operating 7 schools in Dongguan, Huizhou, Jieyang, Weifang, and Panjin and providing private premium education for PRC curriculum programmes, including elementary, middle, high schools. The Group will focus on developing in the Guangdong province, so that it can be benefited from the Guangdong-Hong Kong-Macao Greater Bay Area. Besides, the rise of middle class in China is believed to bring demand for private premium education. Wisdom is able to cope with the upcoming demand, as there are still rooms to expand its schools. And, Wisdom has financed 500 million RMB from Ping An, making it capable of executing M&A in the future. Retail, Property (Tracy Ku)This month I released the first coverage report of Sasa(178.hk), and updated report of Mengniu(2319.hk). The former belongs to HK retail industry and the later is one of the market leaders of China's dairy industry. Among the two, I recommend Mengniu. Mengniu's interim revenue increased 17% y.o.y. to RMB34.474 billion. Gross profit margin(GPM) increased 3.6ppt y.o.y to 39.2%. Operating profit margin fell 0.5ppt y.o.y. to 5.6%, mainly due to the sponsorship of World Cup. Net profit increased 38.5% y.o.y. to RMB1.56 billion. Facing the economic slowdown in China, the management team still raised its full-year growth target from the previous low double digit to the medium double digit and revealed that the business performance from July to August was in line with expectations. Facing the risk of competitors launching promotions or increasing discounts, it emphasizes that it will respond to price wars through increasing innovation capabilities and brand investment. I believe that the dairy industry in China is with rigid demand and the impact from economic slowdown is limited. The double-digit growth target for the whole year is still able to meet. We believe that the recovery of raw milk prices in 2H will help its material associate China Modern Dairy (1117) to further reduce its loss. Sales and distribution expenses are expected to be lower than 1H.

Click Here for PDF format...

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|