|

|

|

*Advertisement* |

|

|

|

|

|

4 Oct, 2018 (Thursday) |

CALC(1848)

Analysis:

China Aircraft Leasing Group (1848) recently completed the disposal of 4 aircraft unded the Initial Aircraft Portfolio to CAG. (China Aircraft Global Limited). With the establishment of CAG, CALC has made great strides in its transition towards an asset-light business model. In June 2018, CALC joined hands with three leading state-owned enterprises engaged in overseas investment, the insurance business and the aviation sector as mezzanine financiers. CALC and the three leading state-owned enterprises held 20% and 80% of CAG respectively. By providing aircraft and lease management service to CAG, the Group further expands its asset management capabilities. (I do not hold the above stock)

Strategy:

Buy-in Price: $8.25, Target Price: $9.50, Cut Loss Price: $7.65

|

|

TSIT WING INTL(2119)

Analysis:

It is the largest B2B coffee and black tea solutions provider in HK with 24.5% of the market share in 2016, and the third and fourth largest provider in Macau and the PRC. It has developed a stable and diverse group of customers that include franchised business of McDonald`s om the PRC and HK, Yoshinoya,7-Eleven, Café de Coral, Fairwood, Tsui Wah, Tai Hing and Spaghetti House. It can reach approximately 60% of the food outlets in HK, with 70% to near 80% market coverage of fast food stores, Cha Chaan Tengs and cafes. In the first half of this year, the company`s revenue increased by 17% y.o.y. to HKD535 million, and the gross profit margin improved by 0.3 ppt to 31.1%. Excluding non-recurring items such as listing expenses, the profit attributable to owners of the company increased by 5.9% to HKD41 million. As the company`s cornerstone investor, Japan`s NH Foods and Singapore`s Fraser and Neave have a strategic cooperation agreement for the sale of frozen, fresh, pre-processed meat and seafood products. Its dividend policy is also attractive as the management has promised to distribute dividends in amounts not less than 35% of net profit of a financial year. It plan to further open up the PRC market. The first five years will focus on the development of South China, and then cover the Yangtze River Delta market, which will be the direction for the development of the entire decade.

Strategy:

Buy-in Price: $1.21, Target Price: $2.50, Cut Loss Price: $1.00

|

| |

|

SUNeVision (1686.HK) - Annual result in line with expectations, yet gross profit margin deteriorating

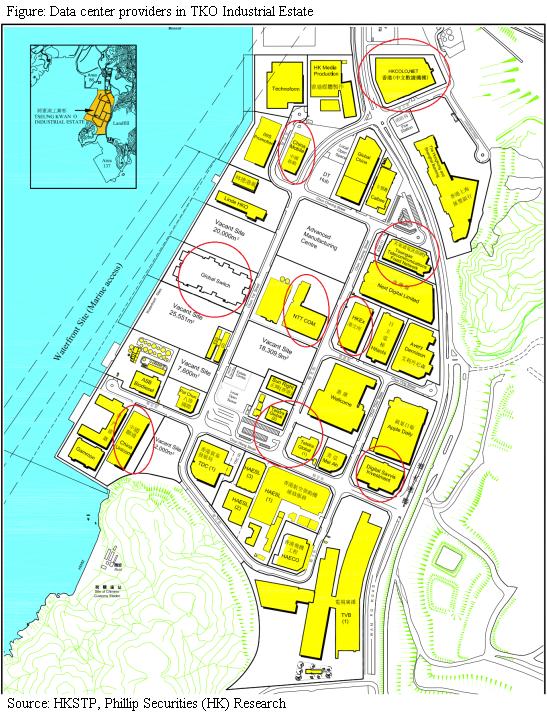

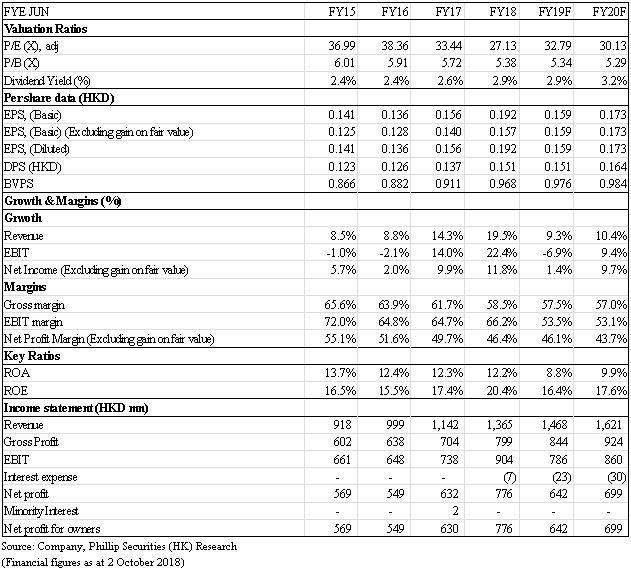

Investment SummarySUNeVision is one of the leading carrier-neutral data center operators in Hong Kong, owned 74.04% by Sun Hung Kai Properties (16.HK). The 2018 annual result was satisfactory, and generally in line with our expectations except GPM. Besides, the group was applying for a judicial review on subletting restriction in industrial estates. Once successful, it could enhance the importance of Mega Plus in Hong Kong. Factoring in the severer deterioration in GPM, rising interest expense, and stronger estimated revenue growth, we derive our target price to be HK$ 5.72, downgrading to “Accumulate”, with 9.79% potential upside. (Closing price at 2 Oct 2018) Corporate Update2018 performance in line with expectations, except gross profit margin The annual result for the group was generally in line with our forecasts, except the gross profit margin. The revenue reached HK$1.36 billion, up 19.5% YoY, slightly over our previous estimate, 16.2%. However, the deterioration in GPM was larger than we expected, dropping by 3.2ppt to 58.5%, 1.5ppt lower than our estimate. The plunge in GPM was mainly due to higher operating costs and depreciation charges due to the opening of MEGA Plus. For selling expenses and administrative expenses, the actual amount generally matched with our expectations. The actual EBIT excluding gain on fair value reached HK$738 million, generally in line of our estimate, HK$742 million. Judicial review on subletting restrictions in industrial estates On 10 Sep 2018, the group applied for a judicial review, accusing Hong Kong Science & Technology Parks Corporation (HKSTP) of allowing its tenants subletting to a third party in the industrial estates, and asking for the enforcement of the lease terms. According to the lease terms in industrial estates, the tenants are prohibited to sublet its space to any third party, because the lease is subsidized by government, leading to a much lower rental than market price. Since data center business usually involves subletting, data center operators located in industrial estates may be considered in breach of the terms during the operations. However, it is allegedly some operators in industrial estates are taking advantage of the grey area in the lease terms to provide subletting, resulting in a judicial review from the group. Currently, there are 9 data center service providers in TKO Industrial estates, such as China Mobile, NTT Communications, HKCOLO, Digital Realty Trust, and etc. If the loophole is closed due to the success in judicial review, the operators in TKO Industrial Estate may be either slapped with penalties or forced to cease the lease agreement. In addition, Tseung Kwan O has been one of the favorite districts for data center, because four submarine cables are connected right there. If the data centers in TKO stop operation due to the subletting restrictions, Mega Plus will be the only data center located in TKO, and permitted to subletting, which enhance its importance in Hong Kong. ValuationWe adjust the GPM downward from 59/58% to 57.5%/57% in 2019/20F, in reflection of the severer deterioration in GPM then our previous estimate. Besides, we also lift the estimated revenue growth from 7.9%/9.2% to 9.3%/10.4% in 2019/20F, in light of the strong growth from Mega Plus as well as the optimization and expansion in Mega Two and Mega-i. Assuming 2019F P/E 36x, we give a target price of HK$5.72, down 4.2% then previous TP, due to the increasing interest expenses and dropping GPM. With 9.79% potential upside, we downgrade to the rating to “Accumulate”.

Risk1. Slower than expected demand on data center 2. Significant increase in land supply for data centers within a short period 3. The entry of cloud service giant players to data center industry in Hong Kong Financials

Click Here for PDF format...

| Recommendation on 4-10-2018 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 5.210 | | Suggested purchase price | N/A | | Target Price | $ 5.720 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|