Investment Summary

Kingsoft is a leading Internet company in China. In FY13-FY17, the company achieved revenue CAGR of 40%. Looking forward, it will focus on three major business segments: games, cloud computing and office software. We highlight that the company 1) has a respected-branded game studio with classic IPs continuing to contribute; 2) is a pioneer in game cloud and video cloud fields, to expand to more vertical fields, 3) owning office software business which leads the domestic market with potential value release after IPO on Shenzhen Exchange. We initiate with a target price of HK$18.8, BUY rating.

Business Overview

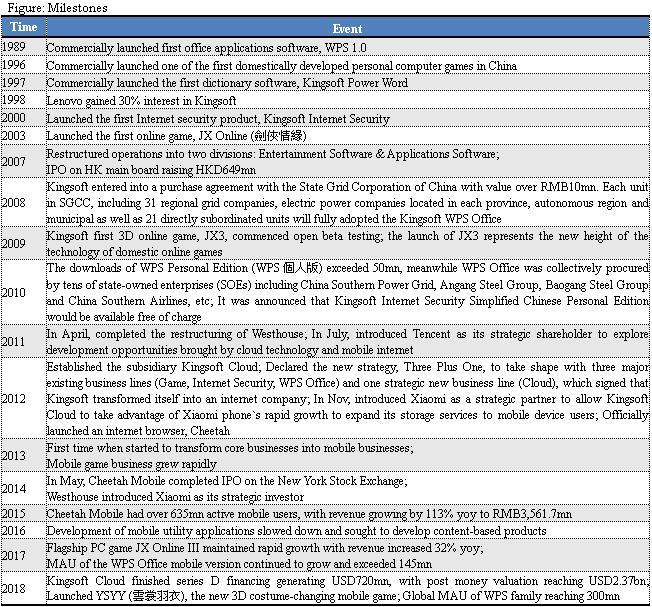

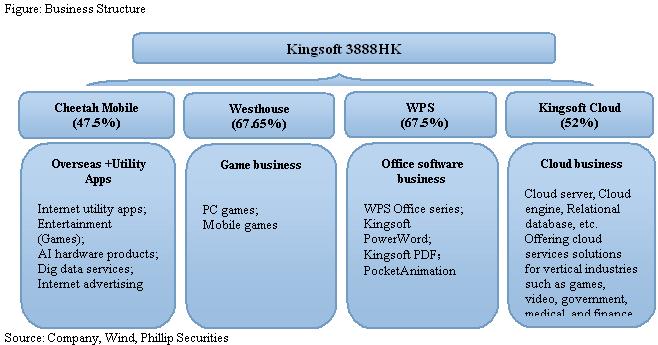

One leading Internet market player. Kingsoft has three major business sectors, namely game R&D, cloud storage & computing, and office software. In 1989 the company commercially launched its first office application software, WPS1.0, and gradually developed and launched popular utility applications, such as Kingsoft Duba and Kingsoft PowerWord, which helped to generate a large customer base overseas and nationally. The company has introduced Lenovo, Xiaomi and Tencent as strategic shareholders, and leveraging on its resource advantages proactively strives for development to cater to ever-changing market demand. As mobile Internet booms since 2013, the company has transformed to explore and develop mobile services. In Feb 2017, the company sold the voting rights of Cheetah Mobile and decides to establish the future focus on game business, cloud, and office software segment.

Respected-branded game company with classic IPs continuing to contribute. Seasun, the famous game studio was first established in Zhuhai in 1995, one of the earliest game market players in China. In 2009,Seasun launched its first 3D online game JX Online III (劍網三), which has been loved by players for many years. The game income grew at a CAGR of 30%, from RMB640.9mn in 2010 to RMB3.12bn in 2017. Seasun introduces strategic shareholders Xiaomi and Tencent to enhance its issue and operation strength and seeks potential synergy effect.

Pioneer in game cloud and video cloud fields, to expand to more vertical fields. The company is the third largest public cloud service provider in China. At present, the intensive capital and high technology threshold have formed barriers for new comers to enter public cloud IaaS market. The company is expected to maintain its leader advantages and continuously enlarge market share, with already set-up data centers in 30 regions worldwide. Kingsoft provides a complete range of cloud products, and integrated service solutions for industries such as game, video, government, medical, and finance, etc. In early 2018, Kingsoft Cloud finished D round financing with a valuation of US$2373mn.

Office software business leads the domestic market and starts the listing process on Shenzhen Stock Exchange. Segment income grew at CAGR of 30% from FY13 to FY17. Its self-developed office software, WPS Office, provides office functions just like Word, Excel, PowerPoint, etc. Kingsoft initiated its R&D in 1988, launched a free PC version in 2005, launched mobile version for Android users in 2011 , and in 2013 covered iOS users. In May 2017, Kingsoft Office formally submitted application to the China SFC for an IPO on Shenzhen GEM.

SOTP valuation gives TP of HK$18.8. Downside risks include: slow-than-expected business growth; foreign exchange risks; overseas exploration fails expectations, etc.

Respected-branded game company with classic IPs continuing to contribute.

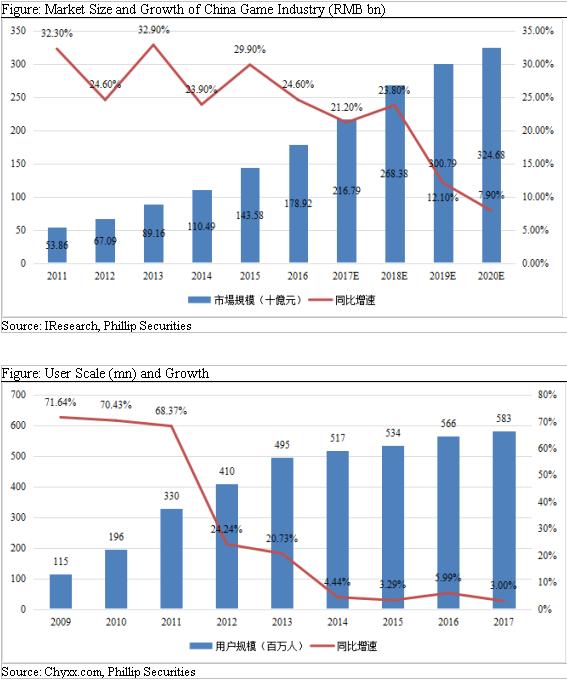

Industry Overview. In 2016, the market size of China's game market surpassed that of US, accounting for 27% of the global market and becoming the first worldwide. In 2017, the market size of China's game market reached RMB200bn. Looking back, we can roughly divide the development of Chinese online game industry into four stages: 1) The initiation: China's online games originated in 1990s, given the word online games suck as "Knight-errant" began to prevail, during which the operation mechanism has begun to take shape with the expansion of user scale and continuous development of game manufacturers. 2) High-speed development period: Since 2003, a high-speed development stage showed, with more capital and talents were appealed, as game businesses` high investment return, short paid-back period, and huge market demand. In 2006-2010, with the introduction and prevalence of Giant's client game "Journey", the charging model began to shift to props charges based. MMORPG has become the dominant force in the market. Meanwhile, domestic enterprises have set up their own R&D team, then the self-developed online games have become the mainstay of the domestic market. 3) Mobile games eruption period: From 2011, with the rise of mobile Internet technology and the popularity of smart terminals, the revenue of web games and mobile games has revealed an explosive growth. These games conform to the user's entertainment demand for fragmented time and mobile ways, so they become the biggest momentum of the industry. 4) Stable Development Period: By user amount, the growth of user scale dropped significantly after 2011, and began to maintain only single-digit growth from 2013. Player growth gradually saturated, and the cost of attracting new traffic was increasing. After 2015, the industry growth has shown a slightly downward trend. IResearch predicts that after 2018, the growth rate of the Chinese game industry will be less than 15%, and by 2020, the growth rate will decline to single digits. Meanwhile, the popularity of other emerging leisure entertainment methods (live broadcast, short video, online drama, etc.) obviously squeezes the market share of the game industry and occupies more entertainment time of users. In future, we expect the game industry maintain stable development. And efforts should be made to improve the user's willingness to pay and expenditure level, as well as to introduce and develop new forms of games to cater to ever-changing user preferences.

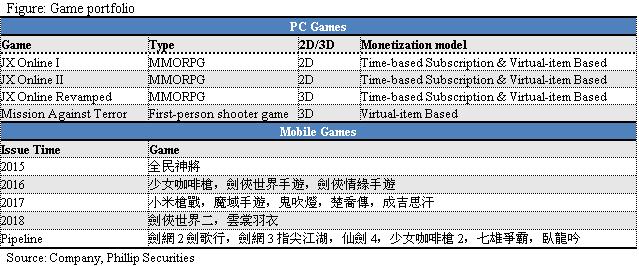

Game platform: Seasun. Established in Zhuhai in 1995, it is the earliest game development studio in China. In Jan 1996, Seasun released its first commercial game (《中關村啟示錄》) in mainland China, marking its first step into game field. Beginning from 2003, online game products (such as 劍俠情緣,仙侶奇緣,封神榜) were launched and entered overseas markets including Vietnam, Taiwan, Singapore, Thailand. In 2009, its first 3D online game JX Online III (劍網三) launched a public beta, and has always enjoyed popularity. The game income grew at a CAGR of 30%, from RMB640.9mn in 2010 to RMB3.12bn in 2017. The company makes breakthroughs in game proxy, given in Oct 2017, Seasun and NetDragon co-issued a mobile game Eudemons, which achieved a turnover of RMB100mn within 19 days. In June 2018, Seasun introduced a new dress-changing mobile game (《雲裳羽衣》), which ranking NO.1 in free game list of Apple Store on its release day.

Cooperation with Xiaomi and Tencent to enhance distribution strength. In 2014, Xiaomi invested US$20mn in Seasun, which thus has enriched Seasun's distribution channel resources. One mobile game (《劍俠世界》手遊) was operated by Xiaomi and has performed good though facing fierce competition. Besides, Tencent acquired a 9.9% stake in Seasun for US$142.6mn in April 2017 (Tencent already invested in Kingsoft in 2011). Tencent's strong distribution network and operation power will help to expand core users and increase market share as well as maximize the value of Seasun's classic IPs.

Valuing both PC & mobile games and strengthening R&D and distribution. Future momentum mainly comes from: 1) Upcoming mobile games (including JX II, XJ IV and so on; 2) Maximizing the money value of classic IP JX, given one related PC game (JX Online III) has maintain notable growth during 8 years and the player amount of its Revamped version grew by 43% within 24 hours after launch; 3) Create a new IP, the company launched its first animation in June this year, "Dream Tower Snow Labyrinth". In three months, the network broadcast more than 40 million, with the potential for IP; 4) Increasing ARPU (Average Revenue Per User). With the help of big data analysis technology, the company continues to optimize user profiles, and improve users` willingness to pay and expenditure level.

Pioneer in game cloud and video cloud fields, to expand to more vertical fields.

Industry overview. It is common to categorize cloud service as IaaS (Infrastructure as a Service), PaaS (Platform as a Service) and SaaS (Software as a Service); or by user characteristic as public clouds ( for the public or a large industry group), private clouds (for a single organization), community clouds (shared by several organizations to support a particular community), and hybrid clouds.

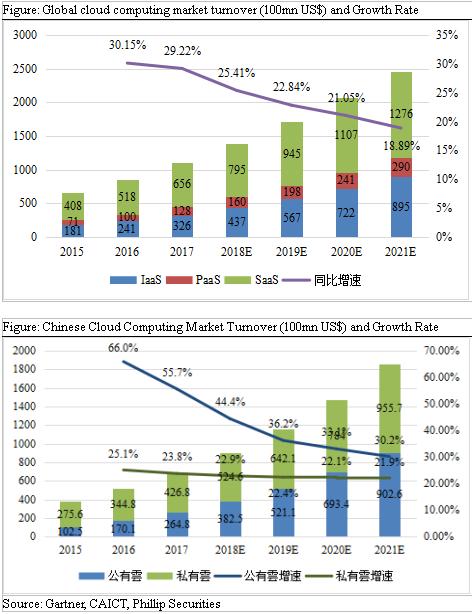

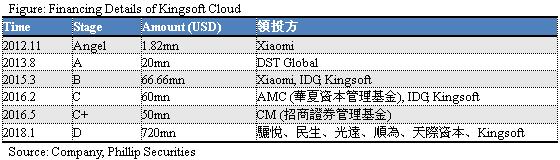

Global Cloud Computing Market. According to CAICT research, the global public cloud market created turnover of US$11.1bn in 2017, up by 29.22% yoy. CAGR in the next few years is expected to be around 22%, and the market size will reach US$246.bn by 2021. China cloud computing market: In 2017, the market value of domestic cloud computing reached RMB69.16bn, up by 34.32% yoy. On one hand, the 2017 turnover of public cloud market reached RMB26.48bn, up by 55% yoy, which will continue to grow rapidly from 2018 to 2021 with a CAGR of 35% and achieve RMB90.6bn turnover in 2021. On the other hand, the size of the private cloud market recorded RMB42.68bn in 2017, up by 23.8% yoy, and is expected to maintain a steady growth with 4-y CAGR of 22% .

Entry barriers to public cloud market already high. The development of public cloud needs not only intensive investment of capital, technology, management and service, but also high technical strength, which have formed substantial barriers for new players. Giant cloud service providers have obvious advantages and we expect that large gets larger. For global market, Gartner's survey indicates that in 2007, five giants (Amazon, Microsoft, Ali, Google and IBM) occupy substantial shares of global public cloud IaaS market share, with yoy growth more than 25%, while other vendors only created 8% more. In domestic market, according to the cloud assessment data from CAICT, main cloud service providers (such as Ali, Tencent, China Telecom, Kingsoft, UCloud, China Unicom, China Mobile, etc.) occupy most market share, and the leading edge is still intensifying.

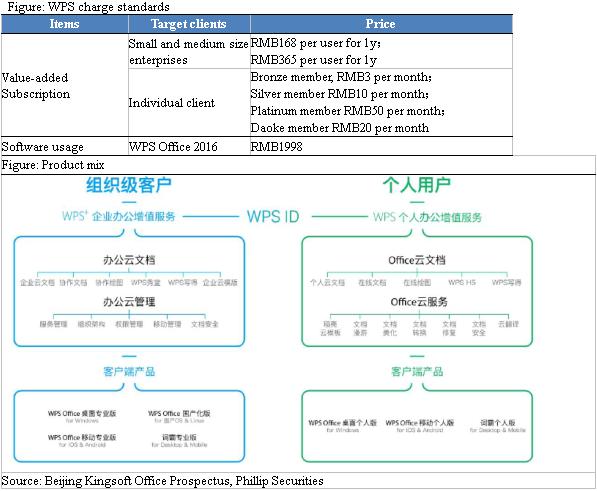

Kingsoft Cloud, founded in 2012, is one of TOP3 Cloud Computing players in China. It currently owns data centers and operations in 30 regions around the world, including Beijing, Shanghai, Chengdu, Guangzhou, Hong Kong and North America, etc. According to IDG, Kingsoft Cloud is the third largest provider of IaaS services, accounting for 6.5% of the public cloud market. Kingsoft has launched abundant cloud products and cloud service solutions for industries such as games, video, government, medical, and finance. In early 2018, Kingsoft Cloud completed D round of financing with a valuation of US$2.372bn.. In future, Kingsoft Cloud will further consolidate the advanced stake in Internet field, expand more vertical areas, and actively exploit overseas markets.

Rapid expansion of Kingsoft Cloud. The segment contributed to topline only RMB11.5mn in 2013 but generated RMB1,332.5mn in 2017, with CAGR over 227%. When founded first, Kingsoft Cloud started with just store business, but further expanded the fields of games, videos, governments, medical care, finance and so on quickly. 1) Game Cloud: Game Cloud has made breakthroughs in CDN, hybrid cloud and network security. Customer usage continues to climb, and business revenue has increased steadily. 2) Video Cloud: Kingsoft builds a platform `Jinjing`(金睛) , based on artificial intelligence in-depth learning algorithm and models, to provide image recognition services, recognizing contents about sex, terrorism, policy, inadequate advertising. Besides, it provides an application `金山云AI画质+`to provide real-time security supervision services for live and short videos, and introduces video super-resolution technology and restoration technology to optimize picture quality and improve viewing experience. Ingsoft Cloud has access to many large Internet enterprises. 3) Government cloud business progress well with extending layout in China. During 18H1, Kingsoft Cloud, as the first contractor involving in Chinese largest government cloud project, Beijing government cloud project, has served 42 bureaus of Beijing Municipal, and has reached a strategic cooperation agreement with Rizhao Shandong to build a smart city. 4) In the medical field, Kingsoft focuses on the medical informatization construction and improvement of medical staffs profession in primary medical institutions, to promote the implementation of graded diagnosis and treatment system. At the same time, using intelligent auxiliary diagnosis technology, Kingsoft can help doctors complete phonetic record entry, conduct safe medication guidance and basic auxiliary diagnosis, which improves doctors` efficiency. CloudHIS, the nation's first cloud-based health information system, has been deployed in more than a dozen provinces and cities.

WPS, the leading office software in domestic market with three monetization channels to underpin growth.

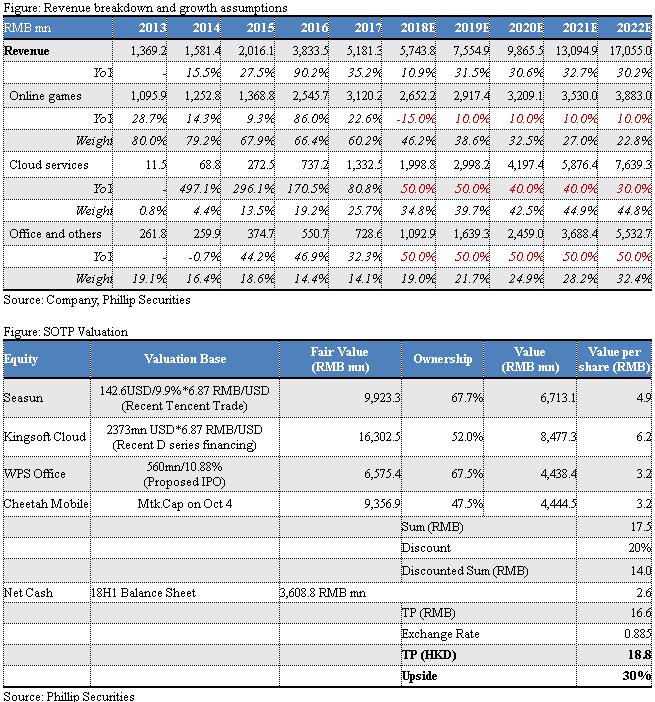

Powerful and compact office software. WPS Office, self-developed by Kinsoft, is an office software suite, which include apps like Word, Excel, PowerPoint, etc. WPS Office products was first developed in 1988, and the company launched a free PC version in 2005, a mobile version for Android users in 2011 and that for iOS platform users in 2013. WPS features low memory occupation, fast running speed, compact size, powerful plug-in platform support, free online storage space and document templates, which supports reading and outputting PDF files. It is fully compatible with Microsoft Office 97-2010 formats, and available in Windows, Linux, Android, iOS and many other systems. In May 2017, Beijing Kingsoft Office Software Co. formally submitted IPO application to China SFC on GEM of Shenzhen Stock Exchange.

Large user base. WPS Office has become an essential software for 32.7% of PC end users and 21.3% of mobile end users in China, according to a survey released by IResearch in this May. The prospectus shows that WPS Office is for both desktops and mobile offices. Through the Google Play platform, the mobile apps now cover more than 190 countries and regions. In domestic market, the products and services have been widely used in government, finance, energy, aviation and other important industries, covering over 30 provinces and cities. Among 102 state-owned enterprises, 82 of them are WPS clients, accounting for 80.39%. In financial industry, Kingsoft WPS serves for all five state-owned commercial banks. In Dec 2017, the number of monthly active users of mobile apps exceeded 145 million, and global MAU surpassed 300mn in 18H1.

Booming with prevalent mobile office trend. According to CNNIC's survey (《中國互聯網路發展狀況統計報告》) , the total number of national informants has reached 770 million, and mobile Internet users has reached 750 million by the end of 2017. IResearch's study pointed out that for the office software industry, the traditional PC-side office is still irreplaceable for office workers, but the demand for mobile office applications is increasing. With the development of PC-based office software, mobile ones become an effective complement to serve for diversified office scenarios. Besides, with the implementation of artificial intelligence technology, office software products tend to be more intelligent, service-oriented, integrated and convenient. The company will continue to upgrade technology and products, integrating artificial intelligence and cloud computing tech, to create better office solutions.

High quality users and healthy user structure pave way for long-term development. IResearch interviewed 2,065 WPS Office users and found that 65.1% of the total sample was 26-35 years old, followed by 36-40 years old taking up 17.0%. Users of 26-40 are the core working population in city, bearing large work pressure with lower disposable income, but having greater demand for rigid consumption. Schools are also one use scenarios of WPS products, given about 10% of the respondents were young students aged 25 and under, meaning. Generally speaking, its user structure is healthy covering core studying and working population, which lays the foundation for sustainable development.

Three major ways to monetization, while currently advertising and value-added services promoting rapid revenue growth. In 2016, the income was made up by three parts, namely software usage fee, advertising charge and subscription services fees, accounting for 43.48%/ 45.08%/ 11.44%, respectively. In 2017, segment revenue of office software and other services amounted to RMB728.6mn, up by 32% yoy. Revenue from advertising promotion and value-added services for individual users all grew rapidly. According to IResearch survey in 2018, 34% of WPS users have purchased membership services. They are willing to pay in order to use membership-specific functions, like PDF toolkits, long pictures output, etc. We see that a considerable number of users have established paying habits. The company continues to optimize and develop new capabilities to provide users with customized office experience. By offering customized and high-quality content, the number of membership at the end of Dec 2017 is about four times that of early 2017. In July 2018, the company launched WPS Office 2019, WPS Office for Mac and other new products. These involving cloud and AI technology will provide users with more intelligent, scene-based office services.

Investment Thesis & Valuation

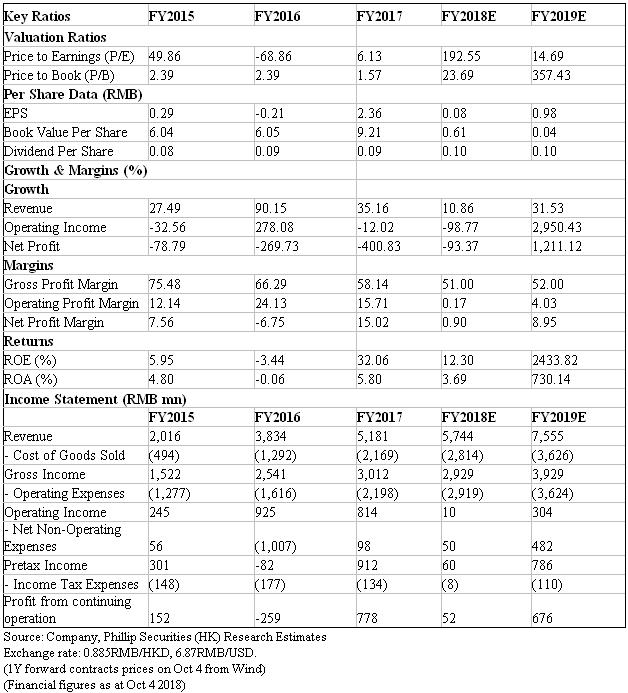

SOTP model derives TP of HK $18.8. We predict that topline will grow at 10.9%/31.5%/30.6%/32.7%/30.2% from 2018 to 2022. Based on the latest market trading of each business, considering a 20% discount, the share price should be HK$18.8. Foreign exchange rates are trading price of the one year foreign exchange forward contracts on Oct 4th. Downside risks include: business growth is slower than expected; exchange rate risk; overseas business development fail expectations.

Financials

Click Here for PDF format...