Investment Summary

- After revenue falling for the third consecutive fiscal year from 2014, FY2018 resumed growth. We believe that this reflected the growth of the overall market demand, as well as the company's own efforts in new products and reforming of sales and distribution channels. We expect the top line growth will accelerate further this financial year, taking into account of the increase in ASP, launching new products, as well as non-traditional channels`expansion. The company raised ASP by medium-to-high single digit since April to May. It expects that the impact of the fare increase on sales volume is short-term, and the actual sales performance in July-August is in line with expectations. It plans to invest the gain from price increase into channels and branding. The sales of regular-size rice cakes has not been affected by the price hike too much, while the larger size one has been affected. Tetrapak “Hot-Kid milk” has not been affected too much, while the aluminum-can one has been affected.

After June, the Chinese retail market sentiment seems to be negatively affected by factors such as the Sino-US trade war, the beverage market has slowed down and about to have a price war. Facing the potential market challenges, the management team stressed that it will not respond by price reductions, but will continue pushing innovations of products and channel promotion. It will also control the speed of shipment to ensure the inventory turnover staying health. Since April, new products such as Sawow cocktail, moisten-throat tea, latic acid water, “Dongchi”(room temperature ice-cream) and ect have been introduced. Mr. Bond Coffee was also launched in campus and offices in East China, mainly targeting young customers, and the market has responded well.

The management team expects that the contribution of new products this year will be higher than low single digit in previous years. Traditional channels will be raised penetration, and non-traditional channels (e-commerce, maternity channel, modern channel and overseas market) will be further expanded, including the launch of channel-specific products. Last year, non-traditional channels accounted for about 20% of total revenue, and we expect the share will further increase this year and beyond. In overseas market, the company has started to build a production plant in Vietnam and is expected to start production from the end of 2019 to the beginning of 2020. The outputs will mainly supply to local and neighboring ASEAN markets. It is also looking at market-expansion opportunities in Thailand, Indonesia and Europe and the United States.

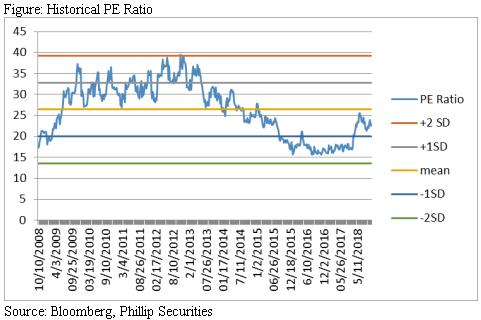

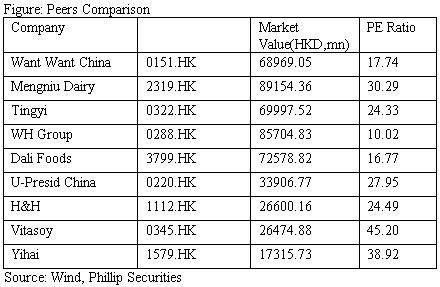

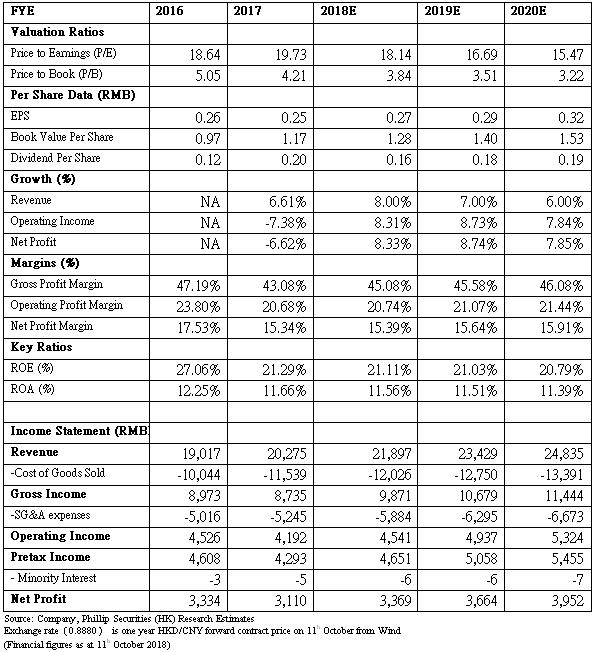

- The cost of raw materials for food industry has been stable since the beginning of 2018. For example, the price of sugar has begun to fall, and the price of iron has also stabilized. Only the price of packaging paper is still at a high level due to factors such as the imported waste paper policy. The management states that if the revenue was in line with expectation and the overall raw materials remained stable compared to last financial year, and the gross profit margin will be able to expand. We expect this year's profit to resume growth, ending the declining trend in profits for four consecutive years since 2014. We give Buy Rating, forecast P/E ratio 21.6 times, the corresponding target price HKD6.58. (current price as of October 11, 2018)

Business Overview

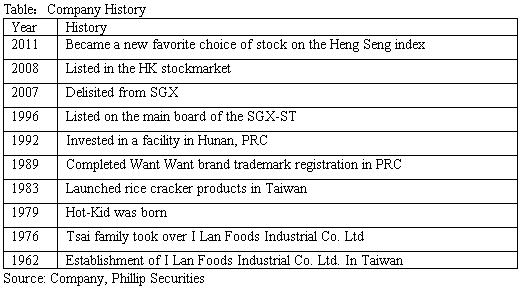

Wang Wang was established in Taiwan and officially invested in the Chinese market in 1992. It was the first Taiwanese company to have a registered trademark in mainland China. It was listed on the Hong Kong Main Board in 2008. It was added as one of the Heng Seng Index constituent stocks and became blue chip stock in 2011.

Last finacial year's performance review

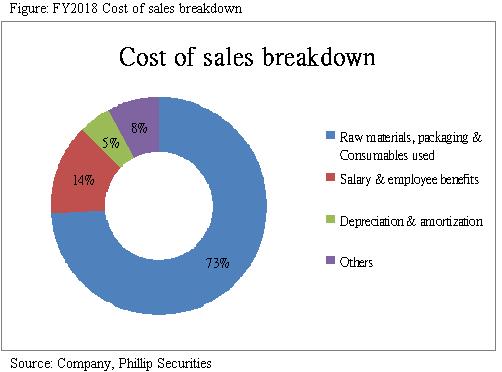

Revenue grew by 6.6% to RMB 20.27billion as compared to the previous year. In particular, each of the core products including Hot-Kid milk, core-brand rice crackers, popsicles and ball cakes, achieved a double-digit growth rate or slightly below such growth rate. Gross profit margin dropped significantly by 4.1 percentage points to 43.1% due to the rising costs of certain raw materials and packaging materials. Accordingly, net profit attributable to equity holders of the Company decreased by 6.6% to RMB3115.8 million as compared with that of the same period in the previous year.

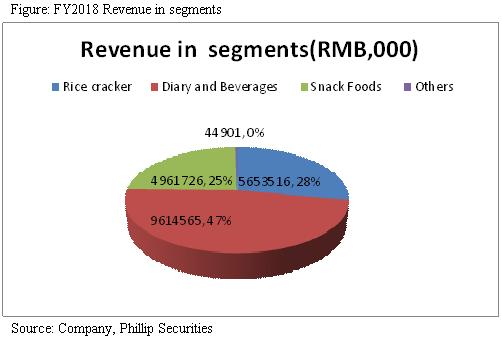

In terms of the Company's revenue attributable to the three key product segments, the revenue from the rice crackers, dairy products and beverages, and snack foods accounted for 27.88%, 47.42% and 24.47% of the total revenue last financial year. Among the three segments, rice crackers grew the fastest i.e. 8.37%, the other two segments were 7.11% and 4.01% respectively.

Operating expense ratio decreased by 0.4 percentage points y.o.y. to 25.9%. Distribution costs to revenue ratio was 14.8%, representing a decrease of 0.4 percentage points y.o.y. partly due to the increase investment in advertising and promotion resources in modern channels and emerging channels which include e-commerce. The ratio of administrative expenses to revenue was dropped by 1.2 percentage points due to the improved sales and effective cost control. By the end of March 2018, the inventory turnover days recorded 81 days improving from 94 days on the end to December 2016. Trade receivable turnover days remained around 20 days.

Non-traditional channels continue to expand: launching exclusive products for online channels

Want Want has put effort in channel restructuring last year. Sales through traditional channels (wholesale business) had resumed on a positive growth track. Sales through modern channels have maintained a double-digit growth momentum since 2016. Sales through e-commerce channel were doubled each year in recent two years and have become an important revenue growth driver. In particular, one-third of the revenue growth of the dairy products and beverages segment has come from e-commerce channel. Sales from maternity channel also maintained strong growth momentum. Under the trend of having a second-child and consumption upgrade in China, there will be more market opportunities.

Want Want's sales strategy on the e-commerce platform is to reduce direct competition through channel-specific products such as brands, packaging and tastes that are different from offline channels. Currently dry goods and Hot-Kid milk are quite popular on e-commerce platform, whereas maternity channel mainly focus on rice crackers under the brand name of “Baby Mum-Mum”.

Sales through traditional channels account for 80% of the total revenue currently, modern channels account for 10%, export accounts for 5 to 6%, and emerging channels (ecommerce and maternal and child platforms) are nearly 4%.

Increasing investment in overseas market

For overseas market, revenue achieved a double-digit growth last year , becoming one of the main drivers of the rice cracker's sales growth. The management team plan to grape the opportunity of One Belt One Road policy by setting up factories in Southeast Asia to further open up the local market. It plans to invest 250 to 300 million yuan annually within the next 3 to 5 years, to set up 3 to 5 factories. Although the land cost in Southeast Asia is more expansive than China, wage and tax rates are cheaper.

According to the management, the development of OEM business will not be ruled out and net profit will have relevant indicator requirements. At present, the revenue share of the business over the total revenue is only low single digit.

New products being launched this year,production cost under control

New products have or will be launched among the three main segments. For the rice cracker segments, non-fry products will be launched. We expect this kind of products can match consumers` increasing demand for healthy foods. For dairy products and beverages segment, there will be unique distinctive new products such as lactic acid water, Sawow cocktail, moisten-throat tea , Mr Bond Coffee and etc. which will be marketed and sold to specific consumer groups.

For snack segments, the company will launch a new product with Tetra Pak package “Dongchi”(room temperature ice-cream), which will extend the company's product range to include ice-cream products.

Investment Thesis & Valuation

We expect this year's profit to resume growth, ending the declining trend in profits for four consecutive years since 2014. We give Buy Rating, forecast P/E ratio 21.6 times, the corresponding target price HKD6.58. Potential investment risks include revenue growth or channel expansion missing expectation, raw material cost with huge volatility. (current price as of October 11, 2018)

Financials

Click Here for PDF format...