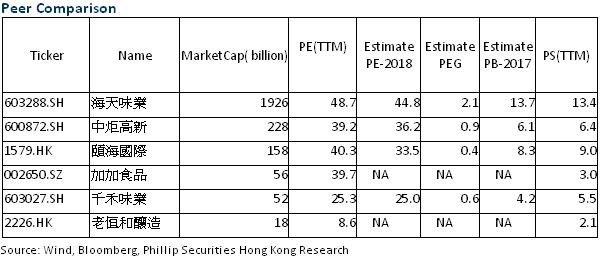

Investment Summary

Jonjee Hi-Tech recorded a high growth ratio in 2018H1 with improved gross margin and expanded network. As a Leading Company in the Condiment Industry of China, it will continue to benefit from the rise of the sales structure caused by the sales upgrading, with strong brand advantage, continuous expansion of production scale and channels, and its operating efficiency will still be on a steady growing trend. According to the latest forecast, we give the "Cautiously Accumulate" rating.

A high growth in the H1 result, and an increase of over 60% of the net profits

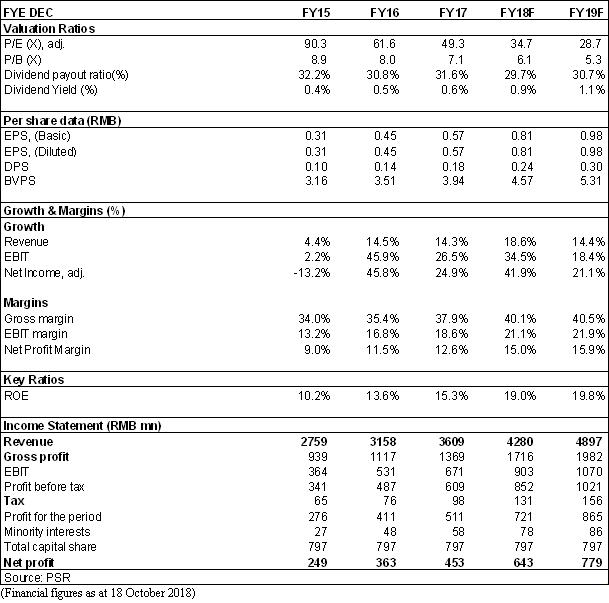

In the H1 of 2018, the company recorded the revenue of RMB2.174 billion, increased by RMB0.370 billion yoy, up 20.5%; the net profit attributable to the parent company was RMB0.339 billion, increased by RMB0.128 billion yoy, up 61%. The EPS was RMB0.43, increased by RMB0.16 yoy, up 61%; the yield of ROE was 10.31%, up by 3.06 ppts yoy.

Steady progress in condiment business, and positive returns contributed by other businesses

In the H1, the condiment business remained stable growth, with revenue of approximately RMB1.962 billion, with a slowdown increase ratio of 12.3%. Among them, the soy sauce progressed steadily, with an increase in revenue exceeding 10%; the increase in edible oil and other categories was 20%, which continued the rapid growth. Thanks to the benefit of scale effect, structural optimization and price lifting in March of last year, the gross margin of condiments increased by 0.47 ppts yoy to 39.99%.For the non-condiment business, the official filing and delivery of some of the sold properties have been completed in the H1 by way of transferring the sold properties to the self-owned properties for the second-hand sales. The real estate company reported the revenue of approximately RMB39.21 million in the H1, up approximately 13.6 times yoy. The net profits attributable to the parent company were estimated to be about RMB9 million, up nearly 6 times yoy.

Improvement in profitability and steady progress in regional sale network expansion

In the H1, the company's comprehensive gross margin increased by 0.82 ppts yoy to 39.95%. At the same time, the expense ratio decreased by 3.34 ppts yoy due to the company's control of sales and reduction of selling expenses. The final net profit margin exceeded 17%, up 4 ppts yoy, and the profitability reached a new high.During the period, the company accelerated the optimization of channel segmentation, added 90 new distributors and continued to steadily promote the nationwide expansion of the sales networks. In terms of the development of the regional market, the north markets have seen the fastest growth, the growth rate of the eastern and central and western markets has been slightly faster than that of the average, and the market shares of the external market have been gradually increased.

Leave imagination due to the change of shareholders

In early to mid–September, the company's former largest shareholder, Foresea Life Insurance, transferred the entire 24.92% of the company's shares to Zhongshan Runtian, a wholly-owned subsidiary of Baoneng Group, which is supposed be more flexible and quicker in investment decisions and corporate governance. As a private enterprise, Baoneng implements a more aggressive management style, inclined to market-oriented. In terms of goal setting, equity incentives, cost control and efficiency enhancement, it has left an imagination space for further optimization of the company's future development.

Investment Thesis

Jonjee Hi-Tech is a Leading Company in the Condiment Industry of China. Condiment industry is encouraged by the Chinese government, and enjoys huge market demand and broad development prospects. In the future, it will continue to benefit from the rise of the sales structure caused by the sales upgrading. With strong brand advantage, continuous expansion of production scale and channels, the company will keep consolidating its position in the industry, and its operating efficiency will still be on a steady growing trend. We expected diluted EPS of the Company to RMB 0.81 and 0.98 of 2018/2019. And we accordingly gave the target price to 30.3, respectively 31x P/E for 2019. "Cautiously Accumulate" rating. (Closing price as at 18 Oct 2018)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...