|

|

|

*Advertisement* |

|

|

|

|

|

23 Oct, 2018 (Tuesday) |

|

|

Industrial Securities(601377)

Analysis:

A shares rebounded against the trend, thus we suggest attention to oversold stocks. Industrial Securities stock price has fallen by over 37% since the beginning of the year. Present P/E ratio is only 16x, lower than the average level of securities firms (22x), and P/B ratio is less than 1.82, less than industry average (1.2x). In 18H1, due to rising investment product remuneration and fixed management fee income, the asset management business (accounting for 39.53% of topline) reported revenue up by 65.91%, gross margin increasing by 3.73ppts. Brokerage business (making up 38.23% in topline), thanks to climbing trading volume and market share, reported 1.22% yoy growth with gross profit margin to rise by 2.86ppts. Investment banking, self-investment business and overseas segment performed poorly, with revenue falling by 52.65%/71.39%/5.83%, accounting for 8.31%/9.72%/7.87% of topline, respectively. For overseas business, although revenue fell, but gross margin improved by 36ppts. With growing customer size and improving income structure, the overseas business development is expected to perform more strongly.

Strategy:

Buy-in Price: RMB4.42, Target Price: RMB5.50, Cut Loss Price: RMB4.00

|

| |

|

Anta Sports (2020.HK) - Strong 18H1 Results with FILA Continuing Rapid Growth

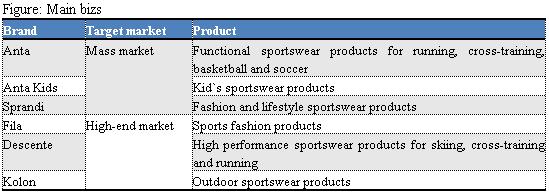

Investment SummaryAnta is a leading sportswear player in PRC. During previous three quarters, Anta delivered strong results and Q4 performance is expected to maintain strong, given more festival promotions and online shopping festival to boost sales. Previously, Anta announced potential acquisition of Amer Sports, a Finnish-based leading sportswear producer, together with a PE fund, which will enrich Anta's product portfolio further. We maintain TP HKD47.3. (Closing price at 19 Oct 2018) Company BusinessQ3 results beat expectation. In Q3, retail sales of Anta biz recorded mid-teens growth, while sales of other bizs (excluding brands newly joined to the Group) recorded 90%-95% yoy growth. According to Mgt, monthly sales per Anta store increased by 10% yoy to around RMB230k and that of Anta Kids rose from RMB110k to RMB120k. For Fila, due to effective adjustment especially in large stores, monthly sales per store was up by around 20% to RMB600k in Q3. On Descente, the product mix was improved given more thin dress was provided to cater for summer needs, boosting sales.

Proposed acquisition will affect dividend paid out but enrich brand mix. In Sep, Anta issued a takeover bid to a Finnish sporting goods giant, Amer Sports, for a cash stake of EUR40 a share, in conjunction with a private equity fund Fountain Vest. Amer is a Finland-based company engaged in manufacturing, marketing and marketing of sports equipment and footwear. Its products are sold through eight major brands, including Wilson, Salomon, Precor, Atomic, Mavic, Suunto, Arc`teryx and Louisville Slugger. The company conducts international business in more than 30 countries, with US, Europe and Japan as main market areas. In 2017, Amer's net profit fell sharply, mainly because of a one-off divestiture of intangible assets. In 2018, thanks to the recovery of the North American market and the strong growth in Asia Pacific region, operation results clearly recovered. Although the acquisition is still uncertain, but once it succeeds, Anta's brand line will be further extended, and it will be an important step to enter the international sports market. However, management indicated that the next two or three years dividend paid-out may be reduced to ensure acquisition funds required, but it will recover gradually in future. Q4 results are expected to be good. Second half is usually peak season for retail industry. Moreover, large e-commerce promotion activities and festival promotions are also expected to boost Q4 sales. We highlight that Fila launches a sub-brand Fila Youth and continuously improves its store performance, meanwhile, Descente is expected to deliver better results in winter sports season. We are optimistic about overall Q4 results.

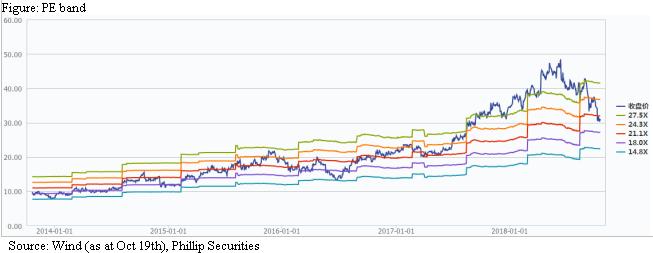

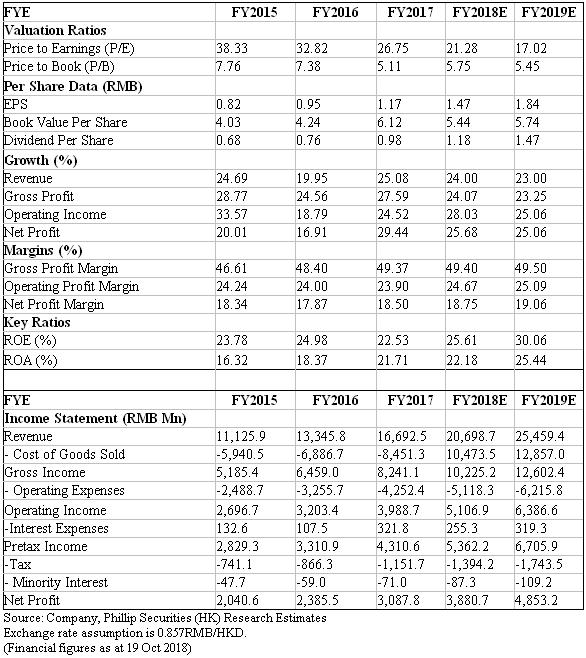

Valuation & RisksWe maintain target price HKD47.3: Projected EPS is RMB1.47/1.84 in 18E/ 19E and target price is maintained as HKD47.3. Risks include: Rising selling and R&D expenses; Sluggish retail market; Inefficiency resulting from so many brands under operation.

Financials

Click Here for PDF format...

| Recommendation on 23-10-2018 | | Recommendation | BUY | | Price on Recommendation Date | $ 31.300 | | Suggested purchase price | N/A | | Target Price | $ 47.300 |

| |

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2018 Phillip Securities (HK) Ltd. All Rights Reserved.

|