Investment Summary

Mainly affected by the weakness of car market and the increase of base, Geely's sales growth rate in September was narrower than previous, but the proportion of new vehicles with higher prices increased significantly. With the forecast that competition in the industry will intensify, we believe the sales growth of Geely will continue to slow down in the fourth quarter of 2018. But as the sales of new models ramp up and the proportion of old models continues to decrease, the marketing of the company will be restructured and move towards the higher end, partly offsetting the negative impact of the price pressure, and maintaining a steady growth in its gross margin and ASP. As the new products and capacity release progress steadily and the company's medium- and long-term growth is promising. So we maintain the rating of Buy.

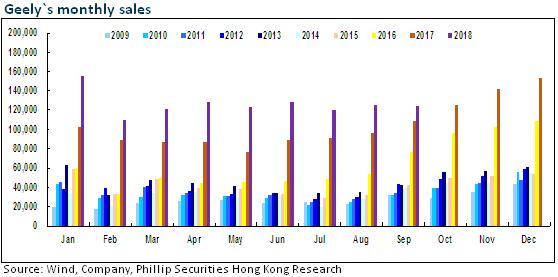

Slower sales growth amid the industry downturn in September

Geely sold 124,429 vehicles in September, increasing by 14% on a year-on-year basis and witnessing a 1% drop on a month-on-month basis. Although the year-on-year growth rate slowed down to a mid-teen number, it was still significantly higher than the industry average of 27 percentage points. According to the data of CPCA, the growth of Chinese generalized passenger cars decreased by 13% year-on-year in September. The company's domestic and export sales were 122,114 and 2,315, respectively, up 14% and 12% year-on-year. In the first nine months of 2018, the cumulative total sales volume was 1,136,858, an increase of 37% year-on-year, reaching 72% of the annual sales target (1.58 million).

More balanced distribution of vehicle sales. Increase in the proportion of new vehicles

According to the sales data of different vehicles, the total sales volume of sedans was 53,409, a slight increase of 1.9% year-on-year, but the distribution was more balanced, and the vehicle structure was obviously shifted upward. The medium-to-high end car Borui has been sold 5,289, an increase of 38% year-on-year. The latest sedan "Binrui" achieved sales of 5,029 in its first month. The sales of Emgrand and Vision were 20,077 and 10,273, respectively, down 15.5% and 8.2% year-on-year. A+ class sedan “Emgrand GL” has been sold 12,515, a slight increase of 3.5% year-on-year. Sales of the low-end sedan "King Kong" decreased by 85% year-on-year to 226.

SUV recorded a high growth rate of 25.8%, reaching 71,020. Mainly affected by the weakness of market and the increase of base, the growth rate in September was narrower than the previous 50%-100% growth rate, but the proportion of new vehicles with higher prices increased significantly. New vehicle LYNK&CO 01/02/ and Vision S1 contributed a total of about 19,000 increments. Boyue, Vision SUV and Emgrand GS sold 7,000 vehicles less compared with the same period last year, and Vision X1 and X3 sold about 3,000 vehicles more compared with last year.

It is also worth mentioning that there were 10,468 new energy and electrified vehicles sold, which exceeded 10,000 for two consecutive months, accounting for 8.4% of the total sales volume. Research and development in new energy vehicle technologies led by the company include 48V micro HEV, full HEV, pure electric vehicles and fuel cell. In the future, the share of Geely's new energy vehicle products is set to increase.

H1 net profit rose by more than 50%

Geely reported a 53.6% growth in its H1 net profit year on year, 50% above its result guidance. Automobile sales increased by 44% year on year, and revenue increased by 36 % year on year to RMB53.7 billion. The scale benefit brought by the expansion of the sales volume increased the gross margin to 20.2% from 19.2% in the same period of last year, and the net profit margin rose to 12.5% from 11.1% in the same period of last year, while the proportion of sales expenses in revenue decreased to 4.2% from 4.4 % in the same period of last year. In addition, despite the first six months of full operation and limited initial production capacity, LYNK&CO has recorded a net profit of RMB340 million with the selling price of its sing vehicles over RMB150,000, representing RMB170 million of return on investments. As at June 30, 2018, the market has seen 940 dealers for Geely brand and 130 dealers for LYNK brand, respectively; meanwhile, the subsidiary Genius AFC also recorded a net profit of more than RMB90 million, with a total loan up to RMB14.34 billion.

New products and capacity release progress steadily and the company's medium- and long-term growth is promising

According to the new product plan, the first SUV "Binyue" produced on the basis of the BMA platform is going on sale recently, following the launch of Binrui sedan also from the same platform. With the rolling out of new models such as Boyue sports version, LYNK&CO 03 and the first MPV in succession, and the actual implementation of its new energy strategy, the company will start a new round of product cycle. We believe that although the high growth rate of sales seems unlikely to repeat that in previous years which is over 50%, it is promising that the company achieves a further development in terms of profitability such as model structure, ASP and gross profit of single vehicles.

Regarding production capacity, in January 2019, the company will invest RMB5 billion in the newly-built engine plant in Guiyang with a capacity of 400,000. As it is to be set in motion soon, the current supply bottleneck pressure of the 2.0T engine is expected to be gradually eased.

Investment Thesis

With the forecast that competition in the industry will intensify, we believe the sales growth of Geely will continue to slow down in the fourth quarter of 2018. But as the sales of new models ramp up and the proportion of old models continues to decrease, the marketing of the company will be restructured and move towards the higher end, partly offsetting the negative impact of the price pressure, and maintaining a steady growth in its gross margin and ASP.

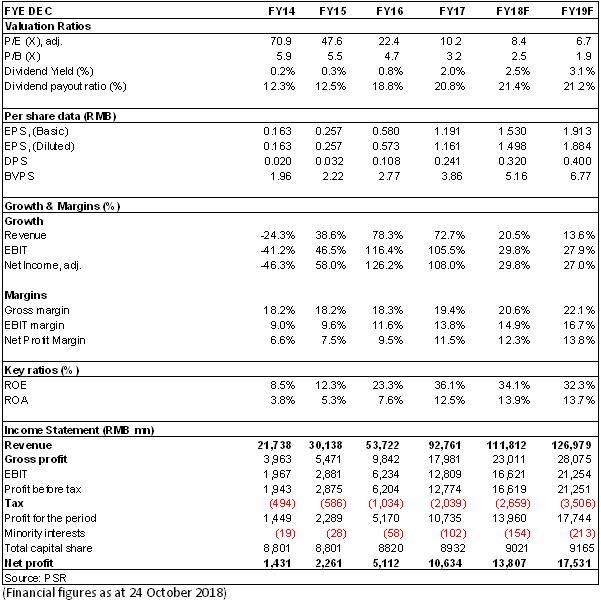

To reflect the lasted forecast and valuation, we revised our target price to HK$21, equivalent to 12/9.7 P/E ratio in 2018/2019, and we maintain the rating of Buy. (Closing price as at 24 Oct 2018)

Financials

Click Here for PDF format...