Investment Summary

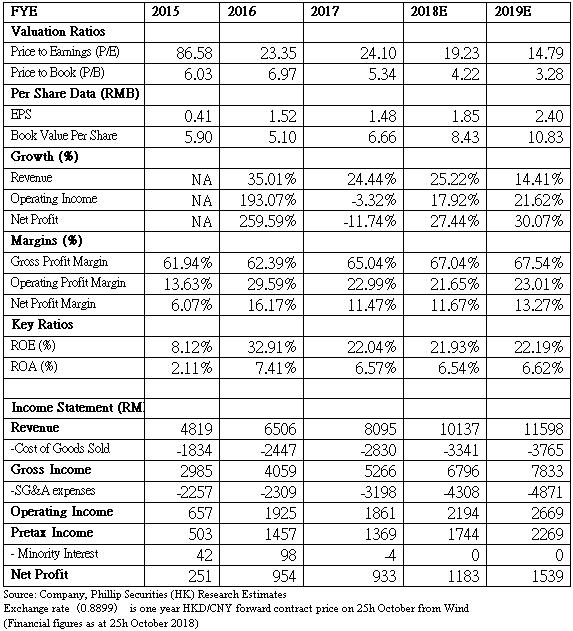

- Interim income as of the end of June this year increased by 28.8% y.o.y to RMB 4.573 billion, and the adjusted EBITDA increased by 16.2% to RMB 1.249 billion. As the top-line growth in 1H exceeded expectations, the management team has raised the ANC(adult nutrition and care) and BNC(baby nutrition and care) business revenue growth guidelines. ANC's revenue growth guideline has been increased from 20% to over 30%, and EBITDA has remained at around 30%, milk powder in the BNC business has been increased from 15 to 20% to slightly above 20%, and the probiotics has been increased from 20 to 30% to about 30%, which is lower than the actual growth of 64% in 1H, mainly due to the one-off capture of the shortage of goods at the end of last year, as well as the base factor. BNC's EBITDA is expected to remain around 20%.

- The management team said that recent operational data was in line with expectations, and has not yet seen the impact of the trade war between China and USA on China's retailing market. We believe that the one-off factors of restocking by distributors during the launch of new registered infant formula, and the backorders placed in the fourth quarter of 2017, will not occur in 2H. We also take into account of the large base effect, and expect that the revenue growth of BNC business will slow down from 1H. However, the growth trend of ANC business is expected to continue, as considering the company will launch a number of new SKUs. The management revealed that around 8 to 9 new SKUs will be launched in 2H of the year, including oral-intake hyaluronic acid and collagen jelly which will be launched during the upcoming Nov. 11.

-The cross-border e-commerce(CBEC) positive list may be launched by the end of this year in China, that will imply that Swisse non-vitamin SKUs of ANC business cannot be sold through this channel. However, we question about whether it can be launched on time, as the details of the policy remain to be clarified. In fact, the market is currently brewing noises about launching a negative list. At the same time, E-commerce Law will be implemented from next year. It requires anyone who engages in purchasing abroad, must obtain licenses and fulfill its tax obligation, purchasing in person or micro shops will be under regulated. We believe that the market of purchasing from abroad is too big to be fully regulated. For H&H, it already has large e-commerce partners including Tmall, JD.com, VIP.come and NetEase Kaola.com. It also has physical stores. We believe the negative impacts of the new law on the company is limited in medium to long term.

The company intends to further expand its offline business. It plans to increase the number of stores from the current 7,000 to more than 9,000 by the end of the year. 50% of the newly added stores will be maternal stores, and there will be synergies with the BNC business. Due to the uncertainty of the policy in the online business, and the increase in the penetration rate of 3rd to 4th-tier cities, the management team expects the share of the offline business to increase in the future.

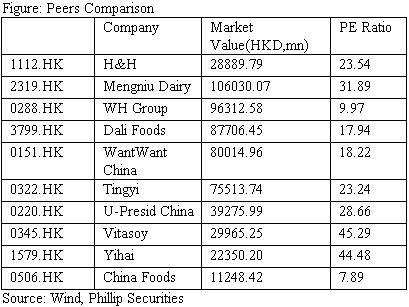

-We expect that the price increase of ANC business in 1H will help GPM to expand y.o.y., while OPM will decline, as this year was positioned as investment year. We expect it will continue to increase spending on marketing activities, including online and offline platforms for its new infant formula. It will also improve the high debt situation caused by the acquisition of Swiss, we expect financial expenses to fall year by year, which will help to improve the net profit margin. We give Buy Rating, forecast P/E ratio 23.9 times, the corresponding target price HKD49.55. (current price as of October 25, 2018)

Business Overview

H&H Group has two core business including baby nutrition and care, and premium quality vitamins and supplements. It owns several brands including Biostime, Swisse, Health Times, Dodie and ect.

One of the company's main priorities during the first half of the year was the progressive transfer of Swisse distribution rights from PGT to the company's full ownership in Hong Kong, Singapore, Italy, Netherlands and the United Kingdom. The transfer of of HK market was completed in February 2018, while the transfer in other territories was completed by the end of June 2018.

In mid-June 2018, the company optimized its capital structure with a new 3-year term loan facility that refinanced an existing senior secured term loan facility with significantly improved terms and conditions. The company enhanced its net leverage ratio and further develop the financial resources with strong cash flow generated during the first half of this year.

Last finacial year's performance review

In 1H, the revenue of BNC increased 33.2% y.o.y., which accounts for 60.7% of total income. The revenue increase includes one-off factors of restocking by distributors during the launch of new registered infant formula, and the backorders of probiotic supplements placed in the fourth quarter of 2017. The revenue of other pediatric products increased by 51.3%. The growth was mainly led by the incremental sales from Dodie branded diapers.

The GPM of BNC segment decreased by 0.6ppt y.o.y to 68.4%. The lowered GPM was mainly caused by the increased cost of packaging materials and the increased cost of IMF ingredients resulting from the upgraded formula in IMF products.

The revenue for the ANC segment increased by 29.3%y.o.y on a currency-adjusted basis. The company has increased price points on its top-selling SKUs, the average price increase was 10 to 15%. The management team has no plan to adjust the price in 2H. According to it, the market has responded the price hike positively. Although there were some push backs in Australia, sales in the Chinese market has continued to rise.

The GPM for the ANC sector increased by 5.6ppt to 65.5%, which help to driven the overall GMP to rebound by 2ppt to 67.2%. The increase in GPM for ANC was mainly a result of the company's initiatives taken including sales price increase for top selling SKUs, reduction of discounts and bonus stocks to customers, as well as enhancement of inventory management efficiencies.

The adjusted EBITDA margin decreased by 3ppt to 27.3%, mainly due to the selling and distribution costs as a percentage to revenue increased by 3.6ppt to 33.8% resulting from the ramped-up investments in advertising and marketing activities. According to the management, it considered the expenses crtical especially the current year is the first year the Chinese new IMF registration rules became effective, and at the same time with the distribution rights of marketing and selling of Swisse products in a number of key markets have been transferred from PGT to the company.

medium- to-long-term development plan of this year for ANC and BNC

-ANC:

The Chinese market accounts for 35% of ANC's business, with CBEC accounting for 92% and offline for only 8%. The company will launch a pregnancy and infant range and adult probiotics range under the Swisse brand in 2H. These products will rolled-out in-store and online in Australia and New Zealand, as well as across Chinese CBEC channels. Furthermore, Swisse's high-selling Calcium+Vitamin D product- the first Australian-made VHMS product approved by the CFDA through new filing process, will also be launch soon.

The State Council has recently announced 22 cities as pilot zones for comprehensive CBEC, in addition to the original 15 cities. We believe that this implies that Chinese government intention to further develop CBEC as an important channel meeting domestic consumption demand.

- BNC:

BNC business mainly focuses on high-end market. According to the management team, it intends to develop new business including goat milk powder. For channels, it will continue to further expand the existing channels. Currently, 2nd, 3rd and 4th-tier cities account for 90% of total infant powder revenue.

In 1H of the year, ASP of infant powder was around RMB300, higher than the industry average. Due to the small base and rapid growth, the overall market is expected to maintain a steady growth of 14 to 16% this year and next, but will slow down from 2019 to 2020.

As competition between major companies in the infant formula market is expected to remain fierce in 2H, the management team plans to invest in branding and channels, while continues to drive creative marketing campaigns. Recently, Dodie brand has got a new brand ambassador to boost its brand exposure in online and offline markets.

Market share

The IMF market remained competitive during 1H as major players stepped up their investments in branding and channel initiatives following the commencement of the China Food and Drug Administration'snew registration rules on 1 January 2018. The Group's super premium and premium IMF series grew 27.9% compared to the same period of last year, due to ongoing consumption trade-up, as well as continuous and effective investments in marketing and channel initiatives.

According to Nielsen, an independent market research company, the marketshare of the company's premium and super premium series under Biostime and Healthy Times increased to 5.7% for the twelve months ended 30 June 2018, while the share of the Group's mid-tier Adimil branded IMF products weakened compared to the same period of last year. Consequently, the company's overall market share increased to 5.9% in the first half of 2018, from 5.5% for the twelve months ended 30 June 2017.

According to research statistics by IRI, an independent market research company, Swisse further strengthened its leading position in the Australian VHMS market, with a market share of 18.6%* for the twelve months ended 30 June 2018. It also has a leading position in the Chinese online VHMS market.

Investment Thesis & Valuation

We give Buy Rating, forecast P/E ratio 23.9 times, the corresponding target price HKD49.55. Potential investment risks include revenue growth and channel expansion not meeting expectation, CBEC policy changes and the competition of infant milk powder market deteriorating (current price as of October 25, 2018)

Financials

Click Here for PDF format...