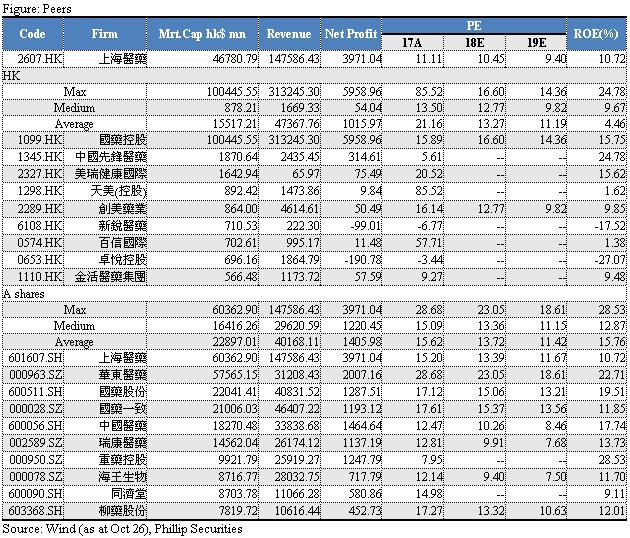

Investment Summary

In 18Q3, core business continued to grow rapidly, given manufacturing and retail income grew at a high speed, and distribution segment delivered stable growth. We maintain the target price of HK$24, BUY rating. (Closing price at 26 Oct 2018)

Business Overview

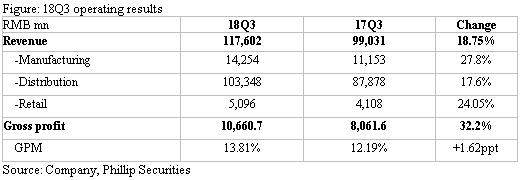

Strong growth of core businesses in 18Q3. As up to the end of third quarter, the company reported revenue of RMB117.602bn, up by 18.75% yoy. The net profit attributable to shareholders was RMB3.37bn, rising by 25.41% yoy. Invested firms contributed to profit RMB464mn, up by 27.24% yoy, mainly due to government's one-off subsidies and increasing sales volume of Roche key products after entering drug reimbursement list. Net profit, excluding non-recurring gains and losses, was RMB2.567bn, up by 4.49% yoy, mainly attributable to substantial increase in non-recurring loss from the acquisition of Guangdong Tianpu, and rising R&D costs. Its profitability steadily improved, with a overall gross profit margin of 13.81%, up by 1.62ppts yoy.

Manufacturing keeping high growth. This segment maintained a high growth rate with three quarters` sales of RMB14.25bn, up by 27.8% yoy with a gross margin of 57.64%. Sales income of 60 key drugs was RMB7.57bn, up by 28.91% yoy. The company completed the acquisition of 26.34% of Guangdong Tianpu shares, and has closed transaction yet. We highlight that Tianpu's products (i.e. Luoan, Kailikang) have enriched the product line of SHP, especially in the field of natural urinary protein products and critical illness. During first three quarters, its two key products Luoan and Kailikang both delivered income over RMB100mn, increasing by 14.4% and 34% respectively. In addition, Mgt indicated that its sales have not been affected by government's centralized purchase policy yet, given no products involved.

Retail segment benefits from high growth of DTP pharmacy business. The retail sector achieved sales revenue of RMB5.096bn, rising by 24.05% yoy, with a gross margin of 15.12% and operating profit margin of 0.80%. Cardinal has fully integrated with the operation management system of SHP and has renewed its agency contracts which are expired with all customers. From Feb to Sep, Cardinal generated net profit of RMB131mn, up by 7% yoy, with net profit margin rising to 0.8% (v.s. 0.5% in last year). SHP aims to raise Cardinal NPM to 1%-1.5% in next two to three years. Total sales of Cardinal this year (Feb to Dec) is expected to exceed RMB20.4bn, in line with company guidance. SHP now owns more than 75 DTP pharmacies. Since Sep, DTP pharmacy sales have increased significantly, with sales in Sep exceeding RMB200mn. We expect that DTP pharmacy sales will continue to grow at a high speed.

Distribution business grew steadily, with sales revenue of RMB103.06bn, rising 16.94% yoy, gross profit margin of 6.67%, and operating profit margin of 2.80%. Distribution network continued to optimize, given the proportion of inventory allocation business decreased, and direct-sales coverage strengthened contributing to 70% of segment income. To improve the national network, it proactively expands northeast and southwest markets, completed acquisition of distribution businesses in Liaoning, Guizhou and Zunyi. At present, the company has acquired 24 provincial platform companies, further consolidating and expanding grass-roots business.

New products attained CDE approval. It is reported that from Jan to Sep, there are 16 new imported drugs approved by CDE and distributed through the national distribution company, 12 of which are introduced by SHP. The company signed a strategic cooperation agreement with Mercedes, and became the national general agent of two new PD-1 drugs in China market. Odivo and Coreda have great potential given their sales revenue reached RMB190mn and RMB150mn respectively within just 2-3 months.

Cooperated with Russian biological medicine company. The company has signed a cooperation memorandum with Russian BIOCAD Company. BIOCAD is engaged in biomedical R&D, production and marketing businesses. Its products focus on the treatment of anti-tumor and autoimmune diseases, covering 14 countries all over the world. Many of its products are in clinical stage. The first phase of partnership will involve four heavy-duty bio-analogues and two bio-innovative drugs. It will carry out in-depth cooperation in the fields of macro-molecule drug R&D, localized production, import registration and marketing, which is expected to enhance its strength in the field of anti-tumor bio-medicine.

R&D progress. The company spent RM756mn on R&D, up by 50.31% yoy, mainly due to increased investment in generics and conformity assessment. Fluoxetine Hydrochloride Capsules and Captopril Tablets passed the conformity evaluation, 12 products (including metformin hydrochloride sustained-release tablets, Cefalexin Capsules and enalapril maleate tablets) have completed BE test and reported to CFDA, and 48 products are in the clinical research stage.

Valuation and Risks

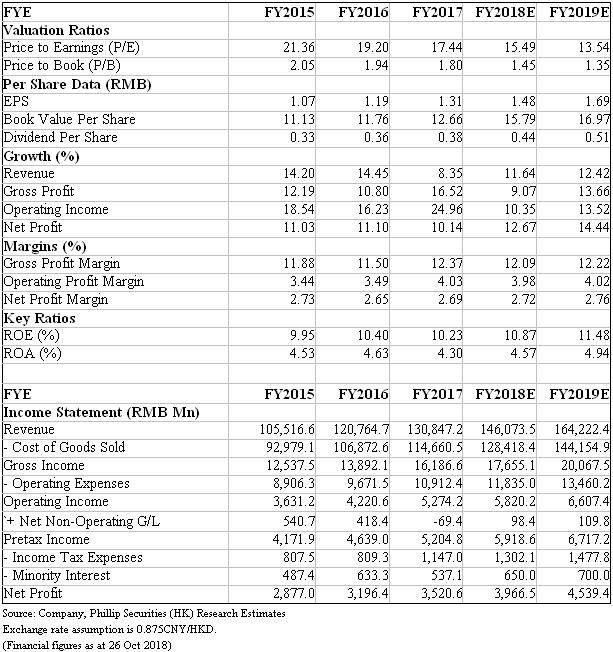

Our valuation model shows TP of HK$24.0, based on target PE 14.25x (with assumption of Ex rate to be 0.875 RMB/HK$). Downside risks include: 1) Price reduction after inclusion in NDRL/PDRL; 2) Unfavorable progress in consistency evaluation ; 3) Policy risk. (Closing price at 26 Oct 2018)

Financials

Click Here for PDF format...