Sectors:

Air, Automobiles (ZhangJing)

Healthcare, TMT (Eurus Zhou)

Education, TMT, Finance (Terry Li)

Retail, Property (Tracy Ku)

Automobile & Air (ZhangJing)

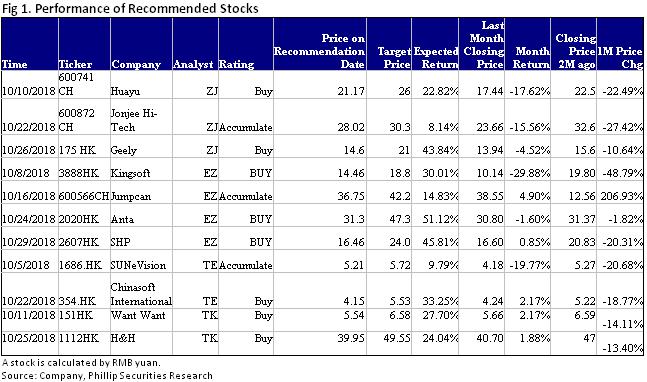

This month I released 3 updated reports of Huayu Auto ( CH), Jonjee Hi-Tech (600872 CH), Dongfeng Group (489 HK) and Geely (175 HK), which got success by their unique Competitive edge. Geely reported a 53.6% growth in its H1 net profit year on year, 50% above its result guidance. Automobile sales increased by 44% year on year, and revenue increased by 36 % year on year to RMB53.7 billion. The scale benefit brought by the expansion of the sales volume increased the gross margin to 20.2% from 19.2% in the same period of last year, and the net profit margin rose to 12.5% from 11.1% in the same period of last year, while the proportion of sales expenses in revenue decreased to 4.2% from 4.4 % in the same period of last year. Geely's sales growth rate in September was narrower than previous, but the proportion of new vehicles with higher prices increased significantly. With the forecast that competition in the industry will intensify, we believe the sales growth of Geely will continue to slow down in the fourth quarter of 2018. But as the sales of new models ramp up and the proportion of old models continues to decrease, the marketing of the company will be restructured and move towards the higher end, partly offsetting the negative impact of the price pressure, and maintaining a steady growth in its gross margin and ASP. As the new products and capacity release progress steadily and the company's medium- and long-term growth is promising. So we maintain the rating of Buy.

Healthcare & TMT (Eurus Zhou)

I published four equity reports this month including Kingsoft (3888HK), Jumpcan Pharma (600566CH), Anta Sports (2020HK), and Shanghai Pharma (2607HK). I tend to highly recommend Kingsoft and Shanghai Pharma (SHP). Kingsoft is a leading Internet company in China. In FY13-FY17, the company achieved revenue CAGR of 40%. Looking forward, it will focus on three major business segments: games, cloud computing and office software. We highlight that the company has a respected-branded game studio with classic IPs continuing to contribute. It is a pioneer in game cloud and video cloud fields, to expand to more vertical fields. Its office software business which leads the domestic market may release potential value after IPO on Shenzhen Exchange. For SHP, as up to the end of third quarter, the company reported revenue of RMB117.602bn, up by 18.75% yoy. The net profit attributable to shareholders was RMB3.37bn, rising by 25.41% yoy. Its core business continued to grow rapidly, given manufacturing and retail income grew at a high speed, and distribution segment delivered stable growth. Thus we maintain BUY rating.

Education, TMT, Finance (Terry Li)

I released two reports on SUNeVision (1686.HK) and Chinasoft International (354.HK). We highly recommend Chinasoft International. The interim result of Chinasoft was satisfactory, where the revenue reached RMB$4.81 billion, up 16.1% YoY, and the net profit was RMB$356 million, up 48% YoY. We believe the software market will remain strong, thanks to the SaaS market and industry digitalization. In addition, the government has launched the "Internet Plus" policies, encouraging the technology integrating into traditional industry, in order to enhance its efficiency. Under these circumstances, as one of the leading software companies in China, Chinasoft will definitely benefit from it. Besides, Chinasoft has been focusing on its industry solution business, where we believe it is able to build up competitive edges in this business, because it is located at the higher position in the value chain; it also requires companies with rich project experience, leading to large entry barrier. Chinasoft had rich experience in Finance, Telecommunication, Internet and Public affairs, and its clients are large enterprises, such as Huawei, HSBC, China Mobile and so on. Chinasoft has launched the crowdsourcing platform “Jointforce” to outsource the small and medium-sized projects of the company. This not only helps Chinasoft to release resources and concentrate on large customers, but also does not have to give up small and medium-sized customers, and earn stable income from it. Therefore, the launch of Jointforce has helped Chinasoft optimize its business model.

Retail, Property (Tracy Ku)

This month I released the first coverage report of Want Want China(178) and H&H(1112). The former belongs to food industry and the later belongs to healthcare and dairy industry. Among the two, I recommend H&H its interim income as of the end of June this year increased by 28.8% y.o.y to RMB 4.573 billion, and the adjusted EBITDA increased by 16.2% to RMB 1.249 billion. As the top-line growth in 1H exceeded expectations, the management team has raised the ANC(adult nutrition and care) and BNC(baby nutrition and care) business revenue growth guidelines. ANC's revenue growth guideline has been increased from 20% to over 30%, and EBITDA has remained at around 30%, milk powder in the BNC business has been increased from 15 to 20% to slightly above 20%, and the probiotics has been increased from 20 to 30% to about 30%, which is lower than the actual growth of 64% in 1H, mainly due to the one-off capture of the shortage of goods at the end of last year, as well as the base factor. BNC's EBITDA is expected to remain around 20%.

The management team said that recent operational data was in line with expectations, and has not yet seen the impact of the trade war between China and USA on China's retailing market. We believe that the one-off factors of restocking by distributors during the launch of new registered infant formula, and the backorders placed in the fourth quarter of 2017, will not occur in 2H. We also take into account of the large base effect, and expect that the revenue growth of BNC business will slow down from 1H. However, the growth trend of ANC business is expected to continue, as considering the company will launch a number of new SKUs. The management revealed that around 8 to 9 new SKUs will be launched in 2H of the year, including oral-intake hyaluronic acid and collagen jelly which will be launched during the upcoming Nov. 11.

The price increase of ANC business in 1H is expected to help GPM to expand y.o.y., while OPM will decline, as this year was positioned as investment year. The company will continue to increase spending on marketing activities, including online and offline platforms for its new infant formula. It will also improve the high debt situation caused by the acquisition of Swiss, financial expenses are expected to fall year by year, which will help to improve the net profit margin.

Click Here for PDF format...